RBI Governor Shaktikanta Das has cautioned the Indian banks against hiding stress and skirting governance issues. Despite the stability of the country’s banks in the face of global spillovers, there are significant challenges plaguing the sector. The banking regulator and the government have taken several measures to strengthen the Indian banking system and eliminate volatility after the collapse of three US banks — Silicon Valley Bank, Signature Bank and First Republic Bank – since March. The crisis has highlighted the need to address domestic issues and restore public trust in the banking system.

The RBI has implemented closer monitoring of the business models of banks and financial institutions. In March this year, finance minister Nirmala Sitharaman urged public sector banks to identify stress points and scrutinise their business models, including concentration risks and adverse exposures.

READ | India’s angel tax rules may hit investor confidence

Without explicitly naming any banks, Shaktikanta Das warned against over-aggressive growth strategies and the use of innovative methods for evergreening loans, which involves reviving a loan on the verge of default by extending further loans to the same borrower. The RBI’s caution on evergreening loans is timely, as the government aims to resolve the twin balance sheet problem of overleveraged companies and high bank NPAs to drive higher GDP growth.

When accounts become non-performing assets, banks are required to make higher provisions, affecting their profitability. To avoid such scenarios, banks sometimes resort to evergreening loans as a temporary fix. This can involve two lenders mutually evergreening each other’s loans through sale and buyback agreements or persuading sound borrowers to enter structured deals with stressed borrowers to conceal the stress, ultimately weakening the banking system.

Need for close monitoring of banks

The banking system is the backbone of any economy, providing financial stability. While central banks control money supply at the national level, banks facilitate the flow of money in the markets they operate within. Therefore, it is crucial for the government to closely monitor and address issues within the banking system, and the situation is no different for Indian banks. Encouragingly, recent stress tests conducted on the banking system following the global banking crisis revealed that Indian banks met the minimum regulatory requirements, highlighting their stability.

In recent years, Indian public sector banks have experienced a significant decrease in losses. While these banks reported a net loss of Rs 85,390 crore in FY18, their profits in FY23 reached Rs 1,04,649 crore. Analysts note a 57% increase in total profits for these 12 public sector banks compared to Rs 66,539.98 crore earned in 2021-22.

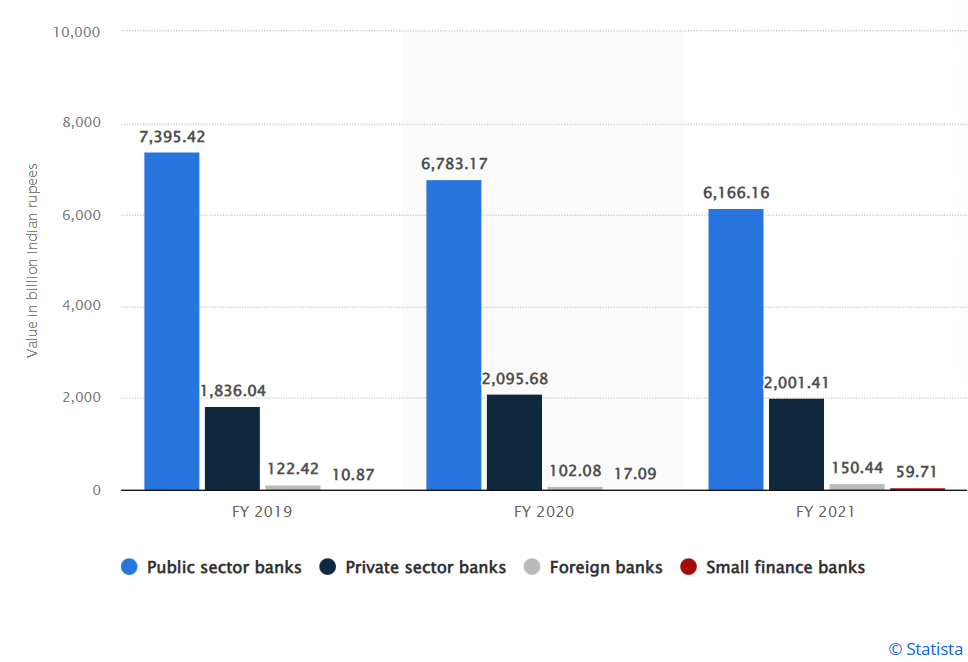

Gross non-performing assets of India’s commercial banks

Despite the progress made, Indian banks still face challenges, particularly with regards to non-performing assets (NPAs) or bad loans. NPAs are loans where borrowers have defaulted on repayment or have been unable to make interest payments for a specified period. The accumulation of NPAs significantly strains the financial health of banks, impacting profitability and lending capacity.

To prevent bank failures, the government has undertaken a privatisation initiative, merging well-performing banks with those facing difficulties. Union Finance Minister Nirmala Sitharaman recently confirmed the government’s commitment to privatising public sector banks. The gross non-performing assets ratio of banks in India fell to 4.41% (unaudited) by the end of 2022, the lowest since March 2015, according to RBI Governor Shaktikanta Das.

Presently, India has 12 public sector banks: Bank of Baroda, Bank of India, Bank of Maharashtra, Canara Bank, Central Bank of India, Indian Bank, Indian Overseas Bank, Punjab & Sind Bank, Punjab National Bank, State Bank of India, UCO Bank, and Union Bank of India.

India’s banking system has experienced a recent revival after grappling with severe bad loan issues for nearly a decade. Policymakers and banks have made concerted efforts to stabilise the system, at least for the time being. However, Indian banks remain vulnerable to monetary policies and external contingencies, including geopolitical risks. Therefore, the government and policymakers cannot afford to become complacent.