By Naliniprava Tripathy, Sushant Sant & Ayush Dharnidharka

The world is in the throes of an unprecedented crisis – a pandemic wreaking havoc across the globe coupled with a deep recession, comparable only to the Great Depression of 1930s. The International Monetary Fund expects the global economy to shrink 3% in 2020, followed by a partial recovery in 2021. It quantifies the losses to the global GDP at $9 trillion, more than the combined GDPs of Japan and Germany. The US economy is seen contracting 5.9% in 2020 and rebounding 4.7% next year in the best-case scenario. Eurozone economy is expected to shrink 7.5%. India and China are the only major economies that will experience growth, albeit at the slowest pace in decades. China is seen growing 1.2 % in 2020 and bouncing back at 9.2 % in 2021 due to resumption of economic activity aided by significant fiscal and monetary stimulus. IMF sees India growing at 1.9% in 2020. The Washington-based financial institution expects the Indian economy to rebound at 7.4% in 2021.

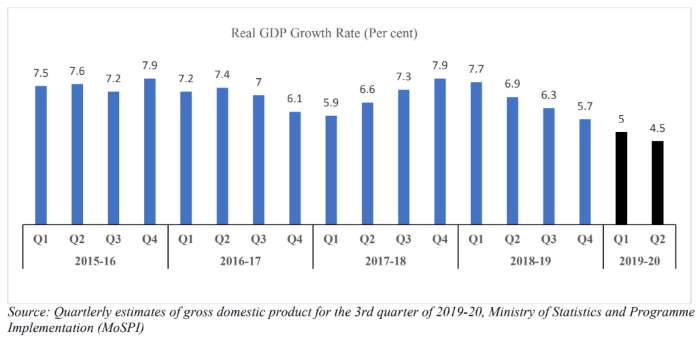

Even before the onset of the Covid-19 pandemic, the global economy was experiencing weak growth and disruption in trade flows. The Indian economy was no exception. Due to a lack of consumption demand, which was the pillar on which the economy was growing at a faster rate, the government also had cut the growth forecast to 5% for FY 2020-21.

The Indian economy is expected to shrink due to the sudden shock of the new coronavirus outbreak on all industrial activity and restrictions on foreign trade and transport. The Narendra Modi government has announced a 21-day nation-wide lockdown on March 25 that was extended to May 3. The financial markets reacted to the pandemic with a 32% crash in benchmark indices in March. One of the most affected industries was the banking and financial services sector, as the entire effect of slowdown reflected strongly on the industry. The Nifty Bank index has declined by 36% in just one-and-a-half months from above 30,000 levels to below 20,000.

Due to uncertainties related to the new coronavirus outbreak and the collapse of business activities in the economy, overall consumption in the country will shrink. The unemployment rate has already jumped threefold from 8% to 24%. A large section of the population would cut their discretionary spending, depriving the economy of a demand driver in the near future. This will, in turn, lead to reduced investments by various businesses. A massive economic stimulus is needed from the government to re-ignite the economy and take it to the pre-pandemic levels. Therefore, all the multilateral organizations, including rating agencies, have cut the growth forecast for India to the range of 0-3.5% for the current financial year.

To counter the challenges mentioned above, the government has already announced a fiscal package of close to Rs 2 lakh crore. Further, the RBI has cut the benchmark repo rate to 4.40% and provided liquidity to the tune of Rs 3.74 lakh crore through long-term repo operations (LTRO) and cut CRR from 4% to 3%. The apex bank has allowed a repayment moratorium of three months on all the loans outstanding as on March 1, 2020 to all borrowers.

READ: Covid-19: Why not a salary challenge at the national level?

To ensure smooth functioning of their activities, banks and financial institutions will have to track the underlying collaterals on outstanding loans. Given the economic situation, the collaterals may also have been depreciated, and therefore, banks have to monitor them along with identifying and providing for bad assets. They will have to undertake a thorough review of all the financial statements along with the quarterly reports and monitor the same. Banks will have to use their judgment in analysing the business of the borrowers and, accordingly, should take proactive measures. Further, there could be circumstances where the borrowers may breach the loan covenants like the meeting of specific ratios or downgrading by credit rating agencies. In these circumstances, the banks should respond judiciously while dealing with the cases and should allow the option of restructuring of loans on a case to case basis.

Another critical issue emanating from the crisis is the growth of stressed assets of banks and financial institutions. As per the RBI Financial Stability Report published in December 2019, the gross NPAs of banks would rise from 9.3% in September 2019 to 9.9% in September 2020. The report, however, was prepared before the pandemic, and given the nation-wide lockdown, the stressed assets are expected to increase at a much higher rate than expected.

Due to the lockdown, all the commercial activities, barring specific service sectors, have come to a grinding halt and it is hoped that the outbreak will be under control in the next 2-3 months. This will cause many borrowers, especially small and medium enterprises (SMEs) not to repay the loan even after the moratorium period. Therefore, it is essential to support banks and financial institutions by delaying the repayment schedule, and a line of credit from the RBI to the commercial banks and financial institutions may be provided to enable them to continue their lending to NBFCs and MSMEs.

READ: Covid-19: How Kerala fought the deadly virus

Further, the asset quality and performance of the banks and financial institutions largely depend on the policies taken by the government and the RBI. Based on the experience of the 2008 sub-prime crisis, if adequate time is given to businesses, the same will flourish again and the burden of stressed assets will decrease.

The most likely impact on the banks post the pandemic would be the stress on profitability due to reduced demand for money, which will lead to lower net interest margins. They will also see a fall in forex income due to the fall in cross-border trade, and a drop-in overall fee income on trade finance products such as letters of credits and wealth products. However, on the liability side, savings and fixed deposits may increase, as funds would flow from capital markets (due to high volatility and uncertainties) to a safer mode of investment.

On a broader level, the regulator should roll out policy measures to curb the amplification of the issues in the financial sector. The RBI has taken measures to improve liquidity. It should take similar steps to contain stressed assets, as the resumption of business activities would be gradual. In this context, the regulator should provide relief to banks and financial institutions in terms of classification of stressed assets into NPAs post moratorium period. A period of 270 days should be provided after the moratorium to classify an asset as an NPA. After that, as the economic conditions improve, the same may be brought down to 90 days over some time in a phased manner.

READ: Coronavirus and capitalism’s hour of crisis

This will give some breathing space to businesses to repay their debt obligations. Banks should permit restructuring of loans, especially with respect of SMEs. The government may have to come up with further recapitalisation of public sector banks. However, in this context, the government and the RBI should provide loans directly to private sector banks/ NBFCs to finance their current needs. This should be part of the fiscal stimulus package of the government.

Crises have always resulted in a spurt in imagination, creativity, innovation, and initiatives. This, in turn, results in development of science, technology, and institutions. When human beings face fear, they seek freedom through creativity. Hence, there is an opportunity for many organisations to innovate, imagine and discuss how they can develop technologies, marketing models, and delivery networks to transform their businesses.

(Dr Naliniprava Tripathy is professor (finance) at IIM Shillong. Sushant Sant and Ayush Dharnidharka are final year PGP students)

Naliniprava Tripathy is an Indian economist based in Shillong. She teaches finance at IIM Shillong.