India’s rupee has been sliding since July 2025 under the weight of structural pressures, energy shocks, tariff frictions, and weaker demand from key markets such as the United States and the UAE amid the Israel-Iran conflict. The jump in crude, LNG, and fertiliser prices has widened India’s external imbalance and made some depreciation inevitable.

But fundamentals do not explain the whole move. Speculative pressure has amplified volatility. The rupee-basis trade between onshore markets and offshore non-deliverable forward markets, along with persistent foreign portfolio outflows driven by high US bond yields and a stronger dollar, has added momentum to the slide. Other pressures, including softer remittance expectations, export disruption through Dubai’s Jebel Ali hub, and stress on India’s reserve position, have deepened the strain.

READ | Rupee under pressure from oil shock and foreign outflows

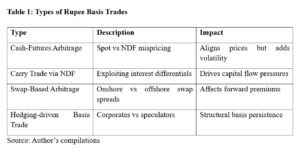

Rupee basis trade and offshore price discovery

The RBI has broadly stayed with a managed float. It has allowed an orderly adjustment rather than forcing an artificial level. That approach held as long as exchange rate movements broadly reflected fundamentals. The Israel-Iran conflict changed that equation by driving up fuel and fertiliser costs, worsening the trade balance, raising current account pressure and increasing the risk of a wider fiscal burden.

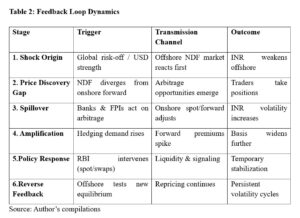

Yet the rupee’s move towards ₹95 to the dollar also appears to reflect speculative distortion. The gap between onshore forwards and offshore NDF pricing has become a channel through which volatility is imported into the domestic market. India’s capital controls leave offshore centres such as Singapore, London and Dubai with disproportionate influence over price discovery during periods of stress.

When the offshore market prices a weaker rupee than the onshore market, arbitrage follows. Traders sell offshore and buy onshore forwards to capture the spread. Banks and other participants then hedge these positions domestically, creating dollar demand not rooted in trade flows. That tightens liquidity and reinforces depreciation. The process becomes self-feeding: offshore sentiment shapes onshore demand, which in turn validates the offshore signal.

RBI exposure limits are a defensible intervention

That is why the RBI’s decision to reduce exposure limits from $500 million to $100 million is a defensible regulatory response. It does not alter the exchange rate regime. It targets the channels through which speculative positioning and offshore arbitrage distort domestic price discovery.

READ | RBI monetary policy and the rupee’s warning signals

The logic is straightforward. The rupee-basis reflects the spread between regulated, deliverable onshore markets and speculative offshore NDF markets. Differences in liquidity, regulation and market composition create arbitrage opportunities. In normal conditions, the onshore market leads. In periods of stress, the offshore market can seize that role and push volatility back into India’s financial system.

The RBI’s curbs seek to contain that spillover. By limiting oversized positions, the central bank is trying to reduce artificial dollar demand, restore discipline in the derivatives market and reassert onshore primacy. That is prudence, not panic.

RBI policy tools have limits

The RBI’s room for manoeuvre is limited. It must manage growth, inflation and financial stability at the same time. Spot intervention, swaps, liquidity tightening and rate signalling can damp volatility, but none can fully offset a shock driven by oil, geopolitics and global dollar strength. Longer-term measures such as deeper onshore derivatives markets, reserve accumulation, swap lines and rupee internationalisation matter, but they do not offer immediate relief in a fast-moving crisis.

Government-side measures are equally constrained in the short run. External turbulence cannot be neutralised by administrative signalling alone. That is why temporary market discipline has become necessary.

FCNR and NRE windows can ease pressure

Administrative tightening, however, cannot be the only response. If pressure persists, the RBI should actively consider FCNR(B) and NRE deposit windows to mobilise stable foreign exchange inflows. With suitable swap support, these instruments can attract non-resident deposits without exposing depositors to exchange-rate risk. India has used them effectively in earlier periods of stress.

READ | West Asia war puts the rupee under fresh pressure

A calibrated relaxation of external commercial borrowing norms could also be considered if geopolitical disruption becomes prolonged. That would allow corporates to access cheaper offshore funding under defined conditions, improve dollar liquidity and reduce pressure on domestic markets.

The objective is stability, not a fixed rupee level

The broader task is to contain volatility while addressing the structural sources of weakness. That means maintaining adequate reserves, diversifying energy sourcing, reducing vulnerability to benchmark shocks, and improving export competitiveness. The purpose is not to defend a symbolic exchange rate. It is to ensure that movements in the rupee reflect macroeconomic fundamentals rather than speculative feedback loops.

In that context, the RBI’s current approach is justified. Its combination of exposure limits, tighter derivatives discipline and calibrated signalling is an attempt to prevent offshore speculation from overwhelming domestic fundamentals. In a period of external shocks and fragile sentiment, that is the correct priority.

Dr Ram Singh is Professor & Head, IIFT New Delhi. Views are personal.