The latest US inflation data has dispelled hopes of a fast decline in inflation and an end to interest rate hikes by the Federal reserve. Going by the current trend, annual benchmark inflation is likely to stay above 4%, a far cry from the target of 2%.

The Fed expects the impact of rate hikes to manifest in the coming months. If the inflation remained sticky, the Fed will have to announce more rate hikes. The persistently high inflation will force policy makers to look beyond the demand-supply dynamics and identify structural issues that keep prices at elevated levels.

This is not the story of the US alone. Most developed and emerging economies too are struggling to tame the persistently high inflation.

READ | G20 presidency may help India leverage its geopolitical moment

Like its counterparts in the US, the RBI also is expected to raise the repo rate to address high inflation. A Bloomberg survey of economists has forecast another 25 basis points hike in the benchmark rate in the first quarter of the financial year beginning April 1. It was widely believed that the RBI would not effect any further hikes from the current rate of 6.5%. After easing from its peak level, the consumer price inflation rose above the RBI’s upper tolerance limit of 6% in January.

India annual consumer inflation rate

For the past year, the RBI has been on a rate hike spree taking cues from other major central banks as policymakers and the government scrambled to rein in runaway inflation. With moderation witnessed in the past several months, it was expected that the apex bank could provide some relief to consumers now on the interest rate front. However, that may not be the case now. The inflation rate was 5.7% in December which was a steep fall from 7.4% in September.

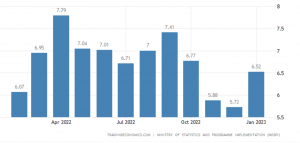

India annual GDP growth rate

In its last MPC meet on February 8, the RBI raised the repo rate — the interest rate at which it lends money to the banking system — by 25 basis points. With higher interest rates, the overall demand for goods and services is bogged down due to costlier funds. While low demand means lower inflation, it also translates into lower growth, something that is not a desirable case for India. The Indian economy grew at 4.7% in the third quarter of the current financial year ended December 2022. It is expected to expand 6.9% in the 12 months to March 31.

Each passing jump in the interest rate, while doing its bit towards containing inflation, by design also hurts India’s economic growth which is necessary for creating gainful employment. With the January jump, the MPC is unlikely to drive interest rates down. RBI is currently stuck in an unenviable position.

Why is India witnessing sticky inflation

Sticky inflation simply means that things have been costlier for a whole now and inflation is taking longer than expected to fall. This also means that hiked food and fuel prices have permeated into the broader economy and made other things costlier along with them. Currently, the main issue causing inflation is higher food prices. In particular, it was the grains such as wheat and maize that seem to have shot up.

Two, core inflation has also inched up. Core inflation is a measure of inflation arrived at by removing the prices of food and fuel. Super core inflation is calculated by removing gold and silver price inflation from core inflation.

Analysts believe that higher inflation is also on account of firms continuing to pass on higher input costs to consumers. RBI has also weighed in the situation. According to a paper titled Anatomy of Inflation’s Ascent in India, which was published in December 2022, RBI Deputy Governor Michael Debabrata Patra and others said that inflation began as a shock to food and fuel prices but got increasingly generalised over ensuing months. As input costs were higher, the same reflected in output prices too. This was especially true for goods prices, in spite of muted demand conditions and pricing power.

India is not the only country which is in a fix on the inflation front. Its peers such as the United States and European countries are also struggling to rein in sticky inflation.

Problem with persistently high inflation

India and other world economies are currently trying to come out of the twin shocks delivered by the coronavirus pandemic and then by the ongoing war in Russia and Ukraine. If inflation stays persistently high or sticky, it would necessitate the RBI to keep raising interest rates. Even if it desists from hiking rates further, the need will remain to keep the rates high for a long period of time which is bound to hurt the economy which is reeling under various macroeconomic headwinds.

With the Reserve Bank of India struggling to keep inflation in its target zone, it is expected that it will increase its main interest rate by 25 basis points to 6.75% in April. However, it is also expected that the apex bank will not undertake any rate hike until the end of 2023, according to economists. RBI is hawkish for now and will need to see a decisive fall in inflation for them to change their stance to neutral, according to analysts. The major concern remains the volatility in food prices. Globally, persistent inflation is prompting major central banks to continue tightening monetary policy until price pressures are tamed.