Greening steel industry: Anthropogenic CO2 emissions have increased atmospheric concentrations to unsustainable levels, impacting the planet’s climate. It is estimated that CO2 levels in the atmosphere are about 50% higher than the 280 ppm of pre-industrial times. The use of fossil fuels for power generation, transportation, and other industrial applications has resulted in the release of about 37 gigatonnes (Gt) of CO2 annually, leading to global warming and erratic weather conditions. There is a need to accelerate the reduction of global greenhouse gas emissions to prevent climate change.

To restrict global warming to between 1.5 and 2 degrees Celsius, as agreed under the Paris Agreement, efforts will require targeting almost all major sectors. According to McKinsey, every tonne of steel produced in 2018 emitted an average of 1.85 tons of CO2, equating to about 8% of global CO2 emissions, second only to the road transport sector at 11.9%.

Steel remains the most widely used material and is unlikely to be replaced soon due to its excellent mechanical properties and the easy availability of iron ore. Global steel demand has grown at 2.5% per year since 2012. As much of the world aspires to develop, steel demand is bound to increase further. For example, though India has become the second-largest consumer of finished steel in the world, its per capita steel consumption is still around 77.2 kg, only one-third of the global per capita consumption of 233 kg.

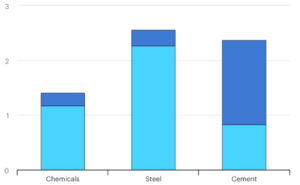

Gigatonne of carbon emissions by industries

READ I India-UK FTA poised for take-off, but concerns linger

China, with a figure of around 650 kg, is far ahead, while other developing countries in Asia and Africa consume almost 10% of China’s per capita consumption. However, the processes currently employed for steelmaking are highly energy and fossil fuel-intensive, making them a major GHG-emitting source. The emission rate varies from 0.67 to 2.32 tons of CO2 per ton of crude steel, depending on the production process.

Of the processes currently followed, the Electric Arc Furnace (EAF) using steel scrap emits the least amount. Overall, given that about 3.3 Gt CO2, or 9% of all CO2 emissions, is attributed to the iron and steel production, decarbonising the steel industry has to be a key part of the overall effort towards reaching net-zero emissions.

Technology options for steel industry

In 2023, 1.89 billion tonne of crude steel were produced worldwide, with China, the world’s largest producer, accounting for 54% of the world’s output, while India, the second largest, produced 129 million tonne, accounting for around 7%. The commonly used Blast Furnace (BF)-based iron-making process consumes more than 500 kg of fossil fuel (coal and/or natural gas) per ton of hot metal produced, and the carbon thermal reduction process results in the emission of approximately 340 m3 of CO2 due to coal use.

To avoid GHG emissions from the steel-making process, blast furnaces would need to be replaced by EAFs. If the entire current global production of steel were converted into green steel, it would significantly reduce the carbon footprints of industries dependent on steel, such as transportation, construction, energy, and other fabrication industries. However, the challenge is multifaceted.

One estimate suggests that decarbonising the steel industry alone will require around $1.4 trillion of investment to meet the challenge of restricting global warming to 1.5 °C. Commercialising new technologies, such as hydrogen-based direct reduced iron (DRI) and molten oxide electrolysis running on renewable energy, has the potential to reduce emissions to zero. However, not only must the production process move from the blast furnace-basic oxygen furnace (BF-BOF) to EAF, but the EAFs must also be powered by renewable energy.

Additionally, improving energy efficiency, using better quality iron ore, and increasing the use of less carbon-emissive feedstock, such as green hydrogen and scrap in steelmaking, will be required. To achieve commercial viability, the cost of green hydrogen supply must be around $2/kg, which is another major challenge. Estimates suggest the global steel sector will require around 50 million tons of competitively priced green hydrogen and around 2,000 GW of dedicated renewable generation capacity annually to meet the estimated demand of 2.2 trillion tons of steel by 2050.

Recycling more steel scrap is another necessity, as producing steel from scrap is 85% less carbon emissions intensive compared to the BF-BOF process. The last but equally important step for steelmakers is capturing and storing carbon to meet their emission targets. Some technology trends are mentioned below:

HYBRIT Technology: The Hydrogen Breakthrough Iron-making Technology (HYBRIT), developed by European companies SSAB, LKAB, and Vattenfall, involves reducing iron ore pellets to sponge iron using hydrogen instead of coal and coke, thus eliminating all CO2 emissions from iron and steel production. The first pilot plant using this technology was commissioned in July 2021.

HDRI: Germany’s ThyssenKrupp is replacing its fossil fuel-based blast furnaces with HDRI shafts, thus avoiding CO2 emissions.

Hydrogen Injection in BF: Using hydrogen injection in the blast furnace to replace fossil fuels is the most common technology being adopted in North America as a reductant and fuel.

Electrochemical Process: US startup Electra has recently commissioned its pilot plant with a novel technology that electrifies iron making. Based on electrochemical and hydrometallurgical processes, Electra’s breakthrough process operates at merely 60°C and can use high-impurity and discarded iron ores with low ferrous content along with intermittent renewable energy resources.

Carbon capture, utilisation, and storage: Regardless of the deployment of clean and efficient energy solutions, CCUS technologies need to be applied to remove carbon dioxide from the fumes or atmosphere. CCUS technology can also capture and reduce carbon emissions during hydrogen production from fossil sources. This gradual transition helps avoid abrupt technological changes and sharp cost increases. However, the use of CCS technologies will drive costs upward and cannot capture all emitted CO2, making them a temporary solution.

Global steel industry practices

As the largest steel producer and consumer, China has a critical role in promoting green steel. With a share of 54% in global steel production, China accounts for around 62% of global steel emissions. Success in global steel decarbonisation depends on their adherence to greener goals. In 2021, 89.4% of China’s total crude steel was produced using the BF-BOF route, while 10.6% was produced by the EAF route.

On average, China generates over 2 tons of CO2 for every ton of steel it produces, while the global average is 1.91 tons CO2/ton. Despite investing in coal-based steel plants, which contradicts their climate commitments of achieving carbon neutrality before 2060, China’s steel sector plans to replace primary steel production using blast furnaces with secondary steel making using electric EAF with a higher proportion of steel scrap. This strategy, however, may not be sufficient. China will require new technologies such as CCS and hydrogen-based steel-making.

China has introduced the “Regulations on the Administration of Carbon Allowance Trading,” which took effect on May 1, 2024. Along with the Chinese Certified Emission Reduction (CCER) Scheme, the development and strengthening of China’s emissions trading scheme (ETS) is expected to limit carbon dioxide emissions growth and achieve carbon neutrality by 2060.

In Europe, the BF-BOF route accounts for 60% of steel production. The steel manufacturing sector has a share of 4% of the total CO2 emissions and 22% of industrial carbon emissions. Established in 2005 by the European Union (EU), the European Union Emissions Trading System (EU ETS) is the cornerstone of Europe’s strategy for mitigating climate change and has established a stringent cap on the total volume of greenhouse gases permissible for specific industries, including iron and steel.

The industrial sectors covered by the EU ETS must cut their emissions by 62% by 2030 from 2005 levels. If these emissions exceed the industry-specific cap, penalties are imposed. Moreover, to meet climate objectives, the EU ETS will systematically reduce the ‘cap’ for identified sectors. Under the agreement, by 2034, the EU’s free carbon emission allowances will expire. The carbon allowance mechanism allows industries covered by the EU ETS to emit a certain amount of CO2e. EU Allowances (EUAs) can be bought and sold on the market, and the variable market price of EUAs reflects the cost of reducing emissions.

Technologically, all major steel projects in Europe will be ready to use hydrogen by 2026-27. However, the constraint is in the supply chain and cost. An estimated 5 million tons of hydrogen per year is needed to decarbonise the European steel industry. Conventionally produced hydrogen is priced at €10-11/kg, but to be competitive, it has to be available at €2-3/kg. Europe will take another 20-25 years to secure sufficient hydrogen supplies at a competitive cost. Until then, carbon capture and storage (CCUS) technology will be crucial for the sustainability of Europe’s steel industry.

European governments are supporting their steel producers in achieving net-zero transitions through the transition from the BF-BOF to the DRI-EAF route. European countries announced €10.5 billion in grants to steelmakers from January 2023 to March 2024. ArcelorMittal, with a clear-cut decarbonisation roadmap, is stated to be the largest beneficiary with a share of 28% of total aid.

In the US, 33% of crude steel is produced via the BF-BOF route and the rest via the EAF route. Currently, the U.S. performs better than the global average in emissions intensity for both steel production routes, BF-BOF and EAF. To further reduce the carbon footprint of the steel sector, on March 25, 2024, the US Department of Energy announced a proposal to invest $6 billion in 33 projects under the Bipartisan Infrastructure Law (BIL) and Inflation Reduction Act (IRA) to decarbonise energy-intensive industries and reduce industrial GHGs.

Of the $6 billion investment committed, $1.5 billion was awarded to six projects in the iron and steel industry currently using coal. The fund would be utilised for replacing blast furnaces (BF) with hydrogen-ready direct-reduced iron (DRI) plants and for setting up electric melting furnaces (EMF).

Initiatives in India

India, which produced about 129 million tons of crude steel in 2023, is projected to produce 227 million tons by 2030, 347 million tons by 2040, and 489 million tons by 2050. In India, 68% of steel is made through the BF route, where coking coal is the primary reductant. India is also the largest producer of sponge/direct reduced iron (DRI), estimated at 34.15 million tons annually.

Globally, natural gas is the fuel used for DRI production, while in India, 82% of DRI production is coal-based. The Indian steel industry, which is not yet as technologically advanced as developed countries, thus faces an uphill task of achieving net-zero emissions by 2070. The New Steel Policy launched in 2017 envisioned creating a technologically advanced and globally competitive steel industry in India while increasing per capita consumption to 170 million tons by 2030-31, reducing import dependency on steel and coking coal.

In terms of policy, integrated steel plants would also be encouraged to reduce their coking coal consumption and bring it down to par with global best practices by resorting to auxiliary fuel injection technologies like Pulverised Coal Injection (PCI) or natural gas/syngas injection.

To promote a circular economy with increased use of scrap-based steel-making in the country, the policy also envisaged increased efforts to ensure the availability of good quality steel scrap and electricity to the sector. However, despite a comprehensive Steel Scrap Recycling Policy announced in 2019 to reduce import dependency on steel scrap, the total value of imported steel scrap for re-melting has increased by almost 100% since then. By 2030, the import quantity is expected to increase to 20 million tons, making India the largest importer of steel scrap unless the ecosystem for steel scrap management is strengthened in the country.

Several steps in the direction of decarbonisation have been initiated by steel-making units; however, the efforts made so far look patchy given the enormous size of the task. Steel Authority of India Limited (SAIL) is working with Primetals Technologies and SMS group to green the steelmaking value chain, including CCUS, hydrogen-based steel production, electric steelmaking, and the like. ISP, Burnpur, IIT Bombay, and GEECL have an MoU to promote joint research and technology transfer to enhance carbon capture and its utilisation, including CBM recovery.

Other SAIL units are also working on capturing carbon emissions and converting them into useful products. Tata Steel has conducted trial runs for hydrogen injection in their blast furnace at Jamshedpur, recycling of steel scrap, use of biochar in place of coke in DRI furnace, and setting up a carbon capture plant with a capacity of 5 tons per day at Jamshedpur. The Jindal group has earmarked $1.25 billion for CO2 emission reduction in their plants through natural gas/hydrogen injection, CCUS, plastic waste use, syngas application, and more green energy generation in their carbon steel and stainless steel production facilities to achieve net zero by 2050.

The way ahead for steel industry

The country needs more steel for developmental needs, but balancing increased production with minimal environmental damage is vital. To achieve the net-zero target, the carbon intensity of steel production needs to be reduced to 1.75 tons per ton of crude steel from the existing emission rate of 2.4-2.8 tons per ton of hot metal. Before initiating steps on the decarbonisation path, steel producers need to assess and evaluate the technology options and decide the most viable one to decrease their carbon footprint. Broadly, the actions to be initiated should cover the following:

- Pre-treatment/beneficiation of iron ore and coke to improve energy efficiency.

- Waste heat recovery at coke ovens, sintering plants, and blast furnaces.

- Improvement in resource/material efficiency.

- Use of composite blast technology with a combination of natural gas and oxygen to reduce coke consumption in BF.

- Gradual use of greener fuels like PNG and green hydrogen for combustion and reheating in BF, steelmaking furnaces, and slab/plate reheating in rolling plants.

- Adoption of innovative low GHG technologies in iron and steel production.

- Use of EAF for steel making with a larger proportion of steel scrap.

- Use of renewable energy.

The transition calls for an integrated approach across the steel value chain to convert challenges into opportunities. The transition to a low-carbon trajectory in the steel sector has the potential to create business opportunities for equipment developers and suppliers for steelmaking, green energy generation, and the hydrogen ecosystem. In this gigantic task of technology and energy transition, government involvement is necessary to shape the direction of these changes. The Steel Policy of 2017 urgently needs to be revisited in light of updated NDC and recent technological developments in both the steel sector and the renewable energy domain, especially hydrogen, to achieve long-term sustainability.

The ministry of new and renewable energy (MNRE) has issued guidelines for undertaking pilot projects for using green hydrogen in the steel sector, which is a step in the right direction, but a total budgetary outlay of Rs. 455 crores until FY 2029-30 is considered too modest. While subsidy supports are crucial for transition, no country can subsidise its industry until carbon neutrality is achieved. The transition needs to be driven by demand aggregation and market-based incentives. To achieve this, demand for carbon-neutral steel and products made from it should be encouraged through green public procurement.

The concept of the circular economy could be another enabler in stimulating market demand and reducing pressure on resources, including energy. Finally, emissions that cannot be avoided could still be tackled through CCUS. Decarbonising steel production will require a revolution at every stage of the industrial value chain, from mining to consumption. In India, however, a one-size-fits-all approach would not work for the entire sector.

To produce truly green steel, a holistic transformation is required by developing and embracing new innovative technologies and greener energy sources like hydrogen. Each technology has its challenges to overcome, with the most common being a stable supply of green electricity to power the processes. Due to the increasing demand for clean electricity by several industries, availability will be a challenge. But the scale of the challenge offers enormous opportunities too. Stakeholders in sectors like renewable power, low-carbon hydrogen, and CCUS will be major beneficiaries of the move towards net-zero emissions.

Krishna Kumar Sinha is an industrial policy and FDI expert based in New Delhi. His last assignment was as an industrial adviser in the department of industrial policy and promotion, DIPP, currently known as DPIIT, under the ministry of commerce and industry of the government of India.