By Saloni Roy and Mausumi Saikia

GST relaxations amid Covid-19 crisis: Businesses were getting back to normal earlier this year when the second wave of Covid-19 caught India by surprise, causing disruption of economic activity and unprecedented losses. The government announced several measures to support businesses with their cash flow, reportings, and tax obligations, like it did last year during the first wave of the coronavirus pandemic. However, considering the vast impact of the pandemic this time round, broader measures are needed to mitigate the adverse impact.

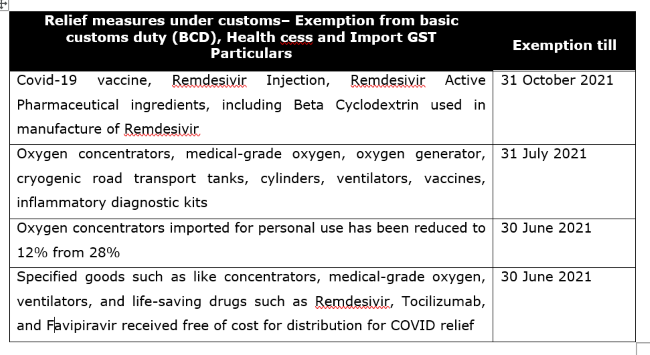

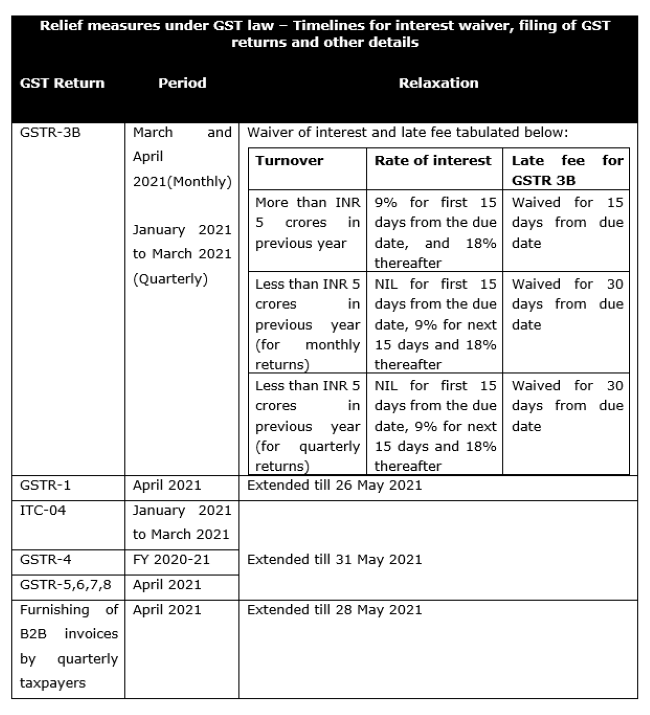

Exemption from basic customs duty, health cess and import Goods and Services Tax (GST) on free of cost imports (i.e. gifts and donations from overseas) of specific relief materials; 15 days extra time to discharge GST for March and April 2021 without interest/reduced rate of interest of 9% (vs 18% regular rate); waiver of late fees in filing GST returns within prescribed timelines; input tax credit (ITC) provisionally in the interim on a cumulative basis for April and May 2021 etc., are some of the measures introduced by the Narendra Modi government.

Customs and central GST authorities are prioritising processing of refund and drawback claims between 15 – 31 May 2021. Timelines of procedures and proceedings have also been relaxed. Verification and approval of fresh GST registration applications due in May 2021 have been extended to 15 June 2021. Time limits for notices, replies, orders, appeals etc. falling due between 15 April and 30 May 2021 have been extended to 31 May 2021.

READ I Legends of the fall: Government, regulators must offer clarity on cryptocurrencies

In August 2020, it was mandated that hearings under Customs, GST and erstwhile central indirect taxes would be conducted through video conferencing. Similar instructions were also issued by state authorities in 2020 for proceedings under Value Added Tax.

List of GST, BCD exemptions and relaxations on compliance timelines

Importers and exporters have been permitted to submit an undertaking, in lieu of bond, for clearance of goods under provisional assessment, and filing bills of entry for warehousing till 30 June 2021 (bonds required to be submitted by 15 July 2021). Validity of Registration cum Membership Certificate, expiring on or before 31 March 2021, for availing any incentives/ authorisations has been extended till 30 September 2021.

Further, COVID-19 Helpdesk has been constituted in April 2021 to address issues arising in international trade such as licensing, delay in Customs clearances, documentation requirements, bank guarantees etc.

READ I Climate summit 2021: Economics may trump ethics, environment

Recommended GST exemptions

While the government has temporarily exempted import GST on specific relief items, it has created a disparity between import of donated items vis-à-vis imports on payment, since this exemption is allowed only on free of cost imports by a relief agency authorised by the state government (to be certified by a nodal authority before import). Government intervention is required to extend this exemption to imports on payment and temporarily remove the requirement of certification from a nodal agency, till the crisis subsides, to enable ease of availing this exemption. Further, the specified list of COVID relief materials could be expanded to include other medicine and medical products under this exemption.

Introduction of reduced GST rate or zero rating for relief materials and other healthcare services/products needs consideration. Owing to the unprecedented nature of the crisis, a re-evaluation and expansion of the scope of zero-rated supplies to include relief items and healthcare services/products is desirable. Zero GST rate will enable input tax credit by local suppliers. An exemption would lead to blocking of credits and increase in prices; hence zero rating/reduced rates should be introduced to help tide over the pandemic impact.

Input tax credit should be allowed on COVID-related expenses such as donations towards COVID-19 relief, items such as PPE kits, masks, and sanitizers by businesses. As the pandemic is impacting all taxpayers, relaxation of interest (complete waiver of 15 days delay in filing of returns) on delayed payment of GST is urged to be extended to large taxpayers (turnover above Rs 5 crore) as well. Relaxation of interest and late fee should be permitted for return period April–June 2021, till 31 July 2021 for both large and small taxpayers. The deferral of filing of GST returns (GSTR-1, 4, 5, 6, 7 and 8) for return period April–June 2021, is urged to be extended till 31 July 2021.

To conclude, the impact of the crisis requires the government to recognise the challenges faced by the country and support should be extended in the form of tax deferrals, relaxation of interest, duty/tax exemptions, processing of all central and state refund claims etc., till the situation stabilises.

(Saloni Roy is Senior Director and Mausumi Saikia is Senior Manager with Deloitte Haskins and Sells LLP.)