India will soon face a reality that Japan, South Korea, China, Italy and Germany are already grappling with- a rising share of dependent ageing population. In India, that challenge will be harsher. Income gaps are wide. Social security remains thin. Family support is still treated as the default insurance against old age. That will not hold for long.

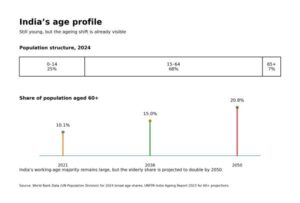

The issue does not yet feel urgent. It should. India already has a large elderly population, and it is set to rise sharply by mid-century. LASI 2021 estimates the elderly at about 12% of the population and projects the elderly population to rise to about 319 million by 2050.

For three decades, India’s reform story has been about expanding opportunity and lifting millions. Social protection has not kept pace. Old-age security still depends largely on family support, a government job, or patchy welfare transfers. The pension system remains thin, fragmented, and unequal. In an economy where over 90% of the workforce is informal, contributory retirement schemes cover only a narrow slice of the labour force.

READ I The ageing truth: Care and policy for India’s silver future

India’s ageing population challenge

India is still a young country. It will not remain one. Fertility is falling. Life expectancy is rising. The share of the population above 60 is projected to cross one-fifth by 2050, and the “oldest old” will grow faster still.

Ageing will also be uneven across states. The India Ageing Report notes that southern states such as Kerala and Tamil Nadu, and states such as Himachal Pradesh, Maharashtra, Odisha and Punjab already have a higher share of senior citizens than states such as Uttar Pradesh, Rajasthan, Madhya Pradesh and Bihar. That matters because pension vulnerability will rise first where family size is falling fastest and longevity is already higher.

Old-age insecurity is also not gender-neutral. The same report flags the feminisation of ageing and the predominance of widowed, highly dependent very old women within the rapidly growing 80+ cohort. Old-age income security cannot remain a residual welfare question. It has to become a core public institution.

READ I Heatwaves and ageing: India’s silent mortality burden

Pension coverage is thin and uneven

India does run targeted pensions for the poor. The Indira Gandhi National Old Age Pension Scheme provides a small central assistance pension (₹200 per month up to age 79, and ₹500 per month thereafter), with states topping up at their discretion. Benefit adequacy is therefore low in many places, and uneven across the country.

Formal sector workers have the Employees’ Provident Fund Organisation and the National Pension System. The Atal Pension Yojana tries to bring in informal workers. Even so, the overall pension net remains limited. For most informal workers, the binding constraint is not awareness. It is irregular work, intermittent contributions, and low surpluses to save.

READ I India’s ageing crisis has a gender angle

Universal retirement account

One answer is to stop waiting for workers to build retirement savings through irregular contributions over an unstable working life. Start earlier. Start at birth.

The idea of a universal retirement account is simple. Every child would receive a government-funded seed contribution into a lifelong account invested in low-cost equity index funds. The account would stay locked until age 60. Withdrawals after that would be capped to protect the real value of the corpus. The balance could be inherited. Families, employers, state governments, or philanthropic institutions could add to it over time. If the account were kept tax-exempt, compounding could work uninterrupted over six decades.

That matters because time matters more than contribution size. If real returns average about 4% a year, even modest early contributions can grow into meaningful retirement assets. Compounding over 60 years will do more than contributions that begin only in mid-career. In an economy where technology may raise the share of income going to capital, early asset ownership can become a structural equaliser.

Cost is manageable, but transition must be explicit

A public contribution of Rs 1,500 a year from birth to age six appears manageable. Even with around 25 million births annually, the total cost would be modest relative to overall public expenditure. This should be seen less as a subsidy and more as a long-term capital endowment.

Fiscal space can be created through better subsidy rationalisation and higher tax buoyancy. The cost also has to be weighed against what the state would otherwise spend later on old-age poverty, income support, and social assistance.

But one point should not be left vague. A birth-seeded account is a future-cohort instrument. It does little for citizens who are already old, or close to retirement. Any credible reform package must therefore sit alongside a clearer plan for today’s elderly poor, not replace it.

Pension design must be rule-based

If such a scheme were run through the Employees’ Provident Fund Organisation, it would build on an existing retirement architecture. But governance would need strengthening. Administrative costs must stay low. Investment management must be professional. Funds should go into broad, low-cost index products so allocation remains rule-based rather than vulnerable to discretion or politics.

Investment risk cannot be hand-waved away. Equity delivers over long horizons, but volatility matters near retirement. A lifecycle glide-path can reduce risk as the beneficiary approaches 60 without turning the scheme into a discretionary product.

The lock-in until age 60 is essential. So is a limit on annual withdrawals thereafter. Without those guardrails, the account would lose its character as retirement protection.

Asset ownership can reduce inequality

A universal retirement account is not a conventional pension. It is not a pay-as-you-go welfare transfer where current workers finance current retirees. Nor is it just another contributory promise. It gives each citizen a small stake in long-term capital accumulation from the beginning of life.

That matters more in an economy shaped by technological change. Artificial intelligence may raise productivity, but it can also concentrate income among those who already own capital. If returns to capital keep compounding and access to capital remains unequal at the start, inequality will widen even in a growing economy. Universal asset ownership at birth is one institutional response.

Inheritance already shapes life chances. Children born into asset-poor households start far behind. A universal retirement account will not erase that gap. It can narrow it. More importantly, it can establish a minimum floor of financial dignity in old age.

India has often tried to balance welfare politics with fiscal caution. This idea speaks to both. It is redistributive in reach, but disciplined in design.

India still has time to act before ageing becomes acute and before technology-driven wealth concentration hardens inequality further. Waiting until old-age poverty becomes a mass reality will be far more expensive.