The Pakistan economy has been in trouble for quite some time, but it is now on the brink of collapse. The Pakistan government’s negotiations with the International Monetary Fund for a $1.1 billion bailout have failed. The economy is facing an unprecedented crisis with foreign exchange reserves just enough to cover about a month’s imports. Pakistan had secured a $6 billion support from the IMF in July 2019.

Pakistan has already exceeded the IMF’s quota for advances by a whopping 210%. The financial agency had earlier said that it has been generous with the South Asian country with a belief that the funding will support the economy and save lives and livelihoods. Pakistan has secured 13 bailout packages from the IMF since the late 1980s. The country is facing high inflation, depreciating currency and plummeting foreign exchange reserves. Pakistan’s economy was already a ticking time bomb when a devastating floods hit it last year. Many economists fear that Pakistan may face a Sri Lanka-like economic crisis.

READ | Public health outlay inadequate; Govt must focus on non-communicable diseases

What is ailing Pakistan economy?

The country has struggled on the economic front ever since its formation. Political instability aggravated the economic situation with successive governments resorted to seeking IMF support to tide over a series of crises. Like every other developing economy, Pakistan also is feeling the heat of the geo-political crises with retail inflation soaring to a 48-year-high of 27.6% in January 2023. Both urban and rural food inflation have remained in double digits in the last 10 months. The country’s currency sank to a record Rs 275 a dollar.

Pakistan GDP growth (%)

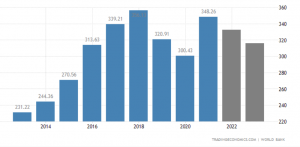

Pakistan external debt ($ million)

The Russia-Ukraine conflict exacerbated Pakistan’s problems and led to energy and food shortages which were aggravated by the worst floods in the country’s recent history. The floods last year had a catastrophic effect on the economy and wiped out an estimated $30 billion in output. Pakistan is also cursed with managers who have rarely stuck to the path of fiscal prudence. The result has been large budget deficits for at least a decade now.

Factors that contributed to Sri Lanka’s economic crisis have also had a significant impact on Pakistan as the economy faces similar challenges. The country is reeling under a large amount of debt. Coupled with a spike in unemployment and a lot of other macroeconomic problems such as import dependence for essential commodities, Pakistan is failing to thrive. Any economy which has high import dependence but refuses to liberalise its export rules is bound to suffer as this situation eventually leads to current account deficit. Restrictions on free trade is among the major causes of Pakistan’s economic woes.

Pakistan needs to fix the chaos

For becoming a stable economy, Pakistan needs to fix political instability which has resulted in the gross neglect of the economic fundamentals. The mismanagement of the economy by successive governments and their reliance on foreign aid have landed the country in a debt trap. Pakistan is currently a visionless and directionless economy which is alarming considering that it has a population of 22 crore. Its GDP growth rate is around 2.4%, while poverty levels are as high as 35%.

Pakistan has faced a persistent balance of payments (BoP) crisis in recent years, characterized by a large trade deficit, declining foreign exchange reserves, and increased borrowing from international institutions. This has been driven by several factors, including a high import bill, low exports, and limited foreign investment.

The trade deficit, which is the difference between imports and exports, has been increasing, putting pressure on the country’s foreign exchange reserves and making it difficult to finance imports and meet debt obligations. This has led to a reliance on borrowing from international organizations, including the International Monetary Fund (IMF), which has provided support to help stabilize the economy.

Like India, Pakistan is also blessed with one of the most fertile lands in the world and hence is an agrarian economy. The Pakistan government may take a leaf from India’s playbook and focus on the agriculture sector. That the country continues to import items of daily use like cooking oils, cotton, wheat, onion, and tomato despite having one of the most fertile lands in the world is a testament to the economic mismanagement. About 22% of Pakistan’s GDP come from agriculture.

The agriculture sector, which employs a large portion of the population, has shown steady growth, while the services sector, including the IT industry, has also been expanding. The country has also been making efforts to increase its exports and reduce its reliance on imports. Despite these efforts, the economy of Pakistan remains vulnerable to external shocks and uncertainty in the global economic environment. The COVID-19 pandemic has also had a significant impact on the economy, with many businesses and industries affected.

Services sector accounts for approximately 56% of the economy, while industry contributes around 23% of the GDP. The industry sector which includes manufacturing, mining, and construction.