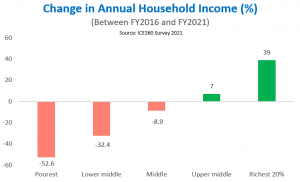

Savings instruments and social security: The Covid-19 pandemic and the economic crisis triggered by it have impacted all strata of Indian society but the richest few. Imagine one partner in a young double-income couple losing their job or facing a salary cut. Or consider the case of an elderly couple losing their savings in speculative securities. Such events not only affect household incomes, but also have an impact on the social security burden of the government. The pandemic has seen several middle class families getting financially ruined, if not pushed into poverty.

India has a large number of small savings accounts held by people with low risk-taking ability. When inflation reaches 5-6%, insecurities are bound to increase. Inflation is a big threat for people with savings and investments as it reduces the purchasing power of their money. Retail inflation measured by the Consumer Price Index rose to a five-month record of 5.59% in December 2021. Wholesale inflation for the month was 13.56%.

READ I Spectre of inflation comes back to haunt Indian economy

The stock indices kept rising during the pandemic crisis, which was not a reflection of economic fundamentals. The economy got caught in a vicious circle of low aggregate demand and high unemployment. To rectify the situation, the country needs out-of-the-box thinking that will trigger the virtuous cycle of sustainable growth.

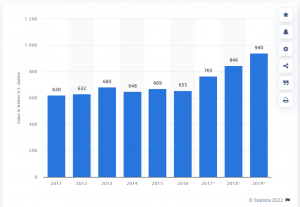

Value of gross national savings from 2011 to 2016

In 2019, the value of gross national savings in India was around $940 billion. This was a sharp increase from about $669 billion in 2015. Small savings schemes such as Senior Citizen Savings Scheme, 15-year Public Provident Fund, National Savings Certificate and Sukanya Samriddhi were major contributors.

As India offers no social protection for education or healthcare, both the young and older sections of the middle class were affected. Hence there is a need to come up with a product that will take care of any future shock. This will secure the future by putting money into creating demand and give confidence to banks to lend more instead of depositing funds with RBI even at low reverse repo rates. The RBI could not contain inflation in the last three years and now grapples with inflation in the range of 6%.

READ I Universal pension can transform Indian economy

A secure savings instrument

The government uses savings to trigger growth in the economy by investing in quality infrastructure. It is saddled with huge fiscal deficits and is always aiming to cut expenditure. The government needs an avenue to generate revenue. To solve the crisis, there is a need for a secure product to encourage long-term deposits. RBI bonds in the range of Rs 25 lakh, Rs 50 lakh and Rs 100 lakh to a maximum of Rs 200 lakh per couple can attract investors that are facing job uncertainties and are looking to retain their standard of living. The net present value of money is eroding consistently due to creeping inflation.

People at both ends of the spectrum — those who are young and have just begun their working lives and those who are at the end of it — need a safety net. Government bonds with an high yields and tenors of 5-10 years will be attractive to them. Cautious older people who are unable to grasp the ways of the market and youngsters who are afraid to lock their money are possible investors. The government too is severely fiscally constrained. A long-term saving instrument will enable it to channelise more funds for development needs.

The instrument could offer a tax-free interest rate of 12% per annum. India has 25-30 crore households. Of these at least 10 crore are possible investors in such a scheme. RBI bonds currently offer 7.15% interest. The government can enhance it to 12% as a safety net to investors irrespective of their age. Rs 20 crore invested in the instrument for 10 years will entail an outgo of just Rs 24 crore.

The most important outcome will be an increase in demand as the investors’ future needs will be secured. This will trigger growth of FMCG and consumer goods industries. Increase in demand will trigger growth, curtail inflation and create jobs. Higher earnings and employment will trigger a virtuous cycle of growth.

Dr Aruna Sharma is a New Delhi-based development economist. She is a 1982-batch Indian Administrative Service officer. She retired as steel secretary in 2018.