India’s economy is expected to grow above 7% in 2026-27 under the newly rebased GDP series, according to the Chief Economic Advisor and several private forecasters. The global backdrop remains fragile: West Asia is volatile, trade policy is unsettled, and commodity prices can turn quickly.

Against that, a 7% plus headline is not trivial. But the rebasing itself changes what the headline captures. The new GDP series uses 2022-23 as the base year and leans more heavily on administrative datasets such as GST filings, alongside methodological changes such as double deflation in manufacturing and agriculture.

READ I Rupee depreciation is India’s oil warning

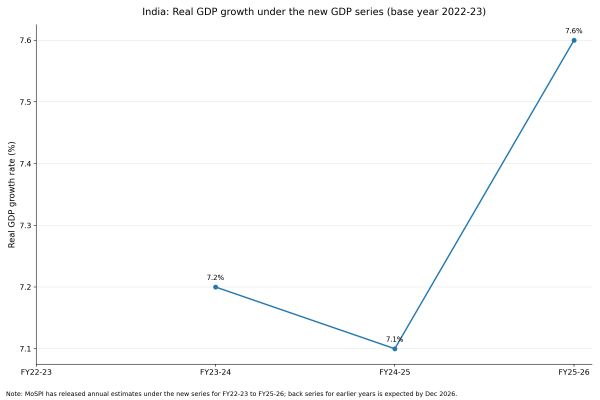

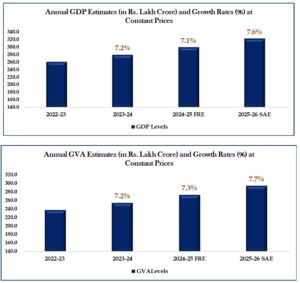

Growth projections under the new GDP series

Chief Economic Advisor V Anantha Nageswaran has put FY27 growth in a 7-7.4% range under the new series, slightly above the 6.8-7.2% range in the Economic Survey. Private forecasts cluster around the same number: Icra at 7%, CareEdge at 7.2%, BofA Global Research at 7.4%. QuantEco remains more cautious at 6.6-6.8%, with an upside bias if global trade tensions ease.

The drivers behind that optimism are familiar. Public capital expenditure remains a key support. Urban demand has held up. Rural consumption has stabilised after weather-related volatility. Monetary conditions are easier than they were. Corporate and banking balance sheets are in better shape than a year ago, which reduces one constraint on investment.

But that list also reveals what the forecast is leaning on: domestic demand and public spending. The harder question is whether private investment follows through at scale.

READ I Indian economy needs a hard oil shield

What new GDP series changes, and what it does not

The statistics office has reweighted sectors to reflect the post-pandemic economy and widened the use of administrative and survey data. The press note on the new series flags, among other changes, expanded use of GST and other administrative sources for quarterly accounts, improved measurement of private consumption using updated classifications, and stronger integration between the production and expenditure sides via Supply and Use Tables.

Manufacturing and agriculture now use double deflation, which removes price effects separately for inputs and outputs. Single deflation is discontinued, and deflators are applied more granularly.

The implication is straightforward. Better capture of formal services and more granular price adjustment can lift measured growth without changing the real economy overnight. The new series does not create new factories, new exports, or new paychecks. It changes the lens.

That is why the FY26 number is best read as a statistical reset, not a sudden break in momentum. Reuters has reported that the revised series places FY26 growth at 7.6%.

READ I RBI dividend windfall cannot replace fiscal reform

Domestic demand, but what kind of demand?

The draft case for demand-led support is plausible. But the quality of that demand matters. A steady consumption number can mask unevenness—between urban and rural India, and between discretionary and mass-market spending.

The new GDP series itself tries to reduce this blind spot by improving household-sector measurement using regular surveys such as ASUSE and PLFS, rather than projecting forward from older benchmarks. That is an improvement in measurement. It does not settle the policy question of whether the current mix of growth is broad-based enough to sustain political and social confidence.

Private investment cycle: The missing hinge

Public capex can support growth for a period. It cannot substitute indefinitely for a decisive private capex cycle. Better balance sheets help, but they are not sufficient conditions.

Private investment responds to a narrower set of triggers: capacity utilisation, predictable demand, export visibility, and a stable cost environment. Oil shocks, tariff uncertainty, and climate-driven food inflation are precisely the kinds of variables that delay long-gestation investment decisions. The FY27 forecast implicitly assumes that these risks remain contained.

That assumption needs to be stated more bluntly, because it is doing a lot of work.

External headwinds: Oil, trade, and services exports

India is not insulated from geopolitics. West Asia risk can feed quickly into oil prices, which then hits inflation management and fiscal arithmetic in the same stroke. Trade policy remains another exposure. Merchandise exports are sensitive to tariff actions in advanced economies, and any interim trade understanding with the United States is not a given.

There is also a newer vulnerability the draft only gestures at: whether parts of India’s tradable services face disruption from rapid adoption of artificial intelligence in client markets. The right stance here is not alarmism. It is to recognise that services resilience cannot be assumed as a permanent hedge.

If an El Nino event materialises in 2026, the near-term transmission channel is familiar: farm output, rural incomes, food inflation, and then a tighter policy trade-off. The macro damage comes less from agriculture’s GDP share and more from its effect on consumption and prices. The growth forecast does not fail because of one bad monsoon, but it becomes harder to defend if weather shocks arrive alongside higher oil and weak exports.

Jobs and income gains: The real test of a 7% headline

One reason the 7% debate matters is that it risks becoming a proxy for policy success. It should not. The core challenge is whether the growth path generates employment and broad-based income gains.

The new GDP series can improve the measurement of fast-growing formal segments. It cannot answer whether those segments are employment-intensive enough. That remains the key gap between a strong national number and the lived reality of households.

QuantEco’s point about the economy still being below its pre-pandemic path is relevant in this context: resilience does not erase lost output, and it does not automatically repair labour-market scarring.

Fiscal space and the capex bet

The post-pandemic growth story has leaned heavily on public capital expenditure. That bet is credible only as long as fiscal space holds.

This is where oil and growth quality converge. Higher oil can widen subsidy pressures and raise the inflation risk premium. If nominal growth or revenues disappoint, maintaining the capex trajectory becomes harder. None of this is a forecast of fiscal stress. It is the basic constraint that sits under the capex-led narrative and should be acknowledged when the forecast leans on capex as a pillar.

Reading FY27 growth under new GDP series

Sustaining 7% growth in a large economy is rare. But the number can conceal as much as it reveals.

Composition matters: consumption versus investment, public versus private capex, exports versus inward demand. Distribution matters too, across income groups and regions. The new series will likely improve the measurement of some dynamic segments. It will not settle the argument about whether India’s growth has become more job-rich, more broad-based, or more resilient to external shocks.

A 7% plus forecast is plausible. It is not a verdict. The road to sustaining it runs through private investment, mass consumption, and employment outcomes—not through statistical rebasing.