Iran conflict and the global economy: The joint US-Israel attack on Iran has turned a regional military escalation into a global macroeconomic risk. The immediate market instinct will be to watch Brent crude. That is too narrow. The larger danger lies in the combination of oil disruption, LNG uncertainty, rising freight and insurance costs, tighter financial conditions, and another blow to business confidence at a time when the IMF already expects global growth to slow to 3.1% in 2026.

Iran conflict matters to energy markets not only because it produces about 3.3 million barrels a day of crude, but because it sits astride the Strait of Hormuz. In 2024, about 20 million barrels a day moved through the strait, equal to about one-fifth of global petroleum liquids consumption. More than one-quarter of global seaborne oil trade and around one-fifth of global LNG trade also passed through that waterway.

That is why the economic damage of the Iran conflict can begin even before any refinery, pipeline or terminal is hit. Reuters reported on February 28 that several tanker owners, oil majors and trading houses had already suspended crude, fuel and LNG shipments via Hormuz after the attack, while LNG tankers were slowing, stopping or turning back. When ships refuse to move, the market no longer waits for physical scarcity. It starts pricing fear, delay and insurance risk.

READ I Why Trump tariffs and protectionism may misfire

Oil prices may rise faster than supply can adjust

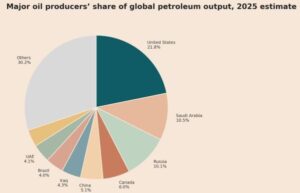

The comforting argument is that the world oil market is better supplied than it was during earlier Middle East crises. That is partly true. The International Energy Agency said in June 2025 that, absent a major disruption, oil markets looked well supplied, with global supply projected to rise by 1.8 million barrels a day in 2025 and by 1.1 million barrels a day in 2026. Inventories had also been building.

But that argument weakens sharply once the disruption caused by the Iran conflict is not geological but logistical. Saudi Arabia and the UAE do have pipelines that bypass Hormuz, but the EIA estimates that only about 2.6 million barrels a day of spare bypass capacity may be available. That is useful, but small relative to the 20 million barrels a day that normally move through the strait.

Markets understand the arithmetic. Barclays said even a 1 million barrel-a-day supply outage could push Brent to about $80 a barrel. Reuters also reported analysts warning that Brent could reach $100 if fighting persists. In other words, the real issue is not whether every Gulf barrel disappears. It is whether enough doubt enters the system to reprice energy, freight and risk premiums simultaneously.

READ I Trump tariffs overturned: What it means for the world economy

LNG, shipping and insurance could spread the shock

The oil narrative understates the gas problem. Qatar’s LNG exports depend heavily on Hormuz, and EIA data show that around one-fifth of global LNG trade moved through the strait in 2024. Reuters reported that at least fourteen LNG tankers had already shown signs of slowing, stopping or reversing course.

That matters because gas shocks travel quickly into electricity prices, fertilizer costs, industrial input prices and household inflation. It also matters because UNCTAD has already warned that disruption around Hormuz can raise shipping costs, delays and insurance premiums, while alternative routes are insufficient to offset maritime disruption. Its 2025 review notes that the strait facilitates 11% of global maritime trade by volume, 34% of seaborne oil exports and 30% of LPG exports.

This is how the Iran conflict becomes a global growth problem. Energy prices rise first. Then freight rates, marine insurance, airspace disruptions and working-capital needs move in the same direction. Importers pay more, central banks become more cautious, and investment decisions are postponed.

READ I Global economy’s 2026 optimism masks deep fault lines

Iran conflict may revive inflation threat

The timing of the Iran conflict is awkward. The global economy was only beginning to move beyond the inflation shocks of the last few years. The IMF’s October 2025 World Economic Outlook still expected global inflation to decline, though it warned that risks remained tilted to the downside for growth and to the upside in some countries for prices.

Oil shocks have a record of undoing disinflation. World Bank research shows that oil price shocks have been the single largest driver of variation in global inflation over the past five decades. A positive oil price shock of around 10% raises global inflation by 0.35 percentage point within a year. The OECD has separately warned that geopolitical tensions in oil-producing regions could lift energy prices, raise short-term inflation expectations and leave policy rates higher than otherwise.

That creates an old but dangerous policy mix: softer growth with stickier inflation. The ECB has noted that geopolitical shocks can raise inflation and reduce industrial production, while also tightening financing conditions. For heavily indebted governments and energy-importing emerging markets, that is the wrong macroeconomic combination at the wrong time.

Asia will bear the first external shock

The first-round pain of the Iran conflict will fall most heavily on Asia. EIA estimates that 84% of the crude and condensate, and 83% of the LNG, moving through Hormuz in 2024 went to Asian markets. China, India, Japan and South Korea were the main destinations for crude flows through the strait.

That makes this a direct issue for India, not a distant geopolitical drama. A sustained rise in crude and LNG prices would pressure the current account, complicate fuel pricing, feed into fertilizer and transport costs, and test the RBI’s inflation glide path. India is better placed than many peers on growth, but it is not insulated from an imported energy shock. The same is true, in varying degrees, across much of Asia.

The best-case scenario is still expensive

It is possible that the worst does not happen. Reuters reported no confirmed damage so far to major Gulf oil and gas infrastructure, and ADNOC said its operations were continuing without interruption. OPEC+ is reportedly considering a larger output increase, while Saudi Arabia and the UAE have already raised exports. These are important stabilisers.

But even the best-case scenario is costly. Reuters reported that Israel has already shut parts of its gas production system, including the Leviathan field, as a security precaution. That is a reminder that wars do not need a formal blockade to produce real economic losses. Persistent insecurity is itself a tax on trade.

The larger point is simple. The world economy entered 2026 weakened by trade friction, fiscal stress and fragile confidence. A prolonged US-Israel-Iran confrontation would not merely add a temporary oil premium. It would deepen fragmentation in energy markets, harden inflation risks, and make global growth more brittle. The shock, if it persists, will not be remembered only as an oil story. It will be remembered as the moment geopolitics once again overruled economics.