Financial inclusion is a focus area for policymakers across the world. In India, financial inclusion is crucial for the economic development of the country and for eradication of poverty, but it is not enough. Financial literacy is equally important to empower individuals and enable them to make informed financial decisions.

Financial literacy refers to the knowledge, skills, and attitudes required to make sound financial decisions. It encompasses understanding various financial concepts such as budgeting, saving, investing, and managing debt. A financially literate population can better utilise financial products and services, protect their financial resources, and contribute to the overall stability of the financial system.

READ I Financial literacy can liberate future generations

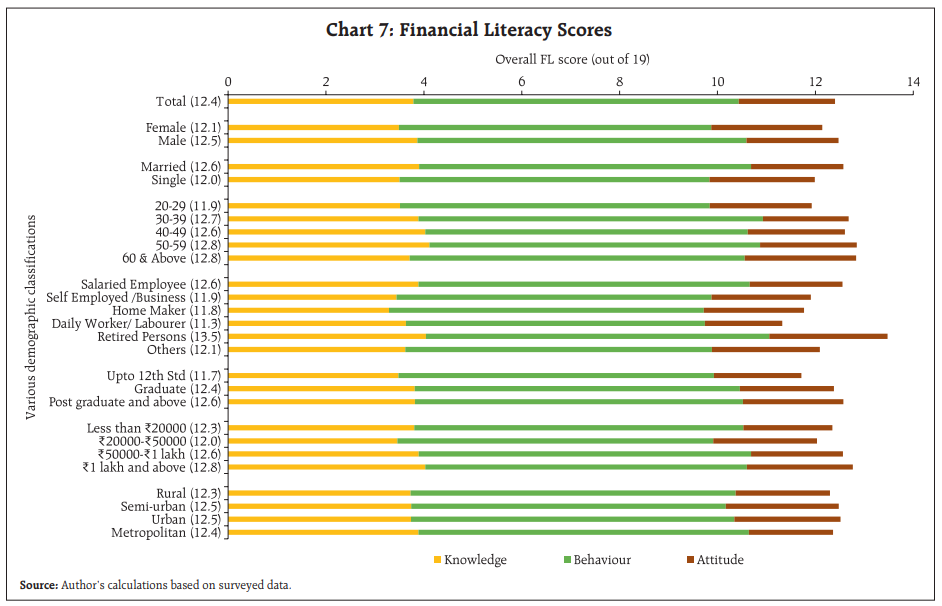

The Reserve Bank of India and other financial regulators have been working to improve financial literacy among Indians. The RBI Bulletin for June 2023 published last week contains an article, Financial Literacy in India: Insights from a Field Survey. The field survey was conducted using a structured questionnaire which consisted of 28 questions divided into two sections: financial literacy and identification. A total of 584 responses were received over 45 days. The respondents represented a diverse range of demographic characteristics, including age, gender, occupation, education level, and income level.

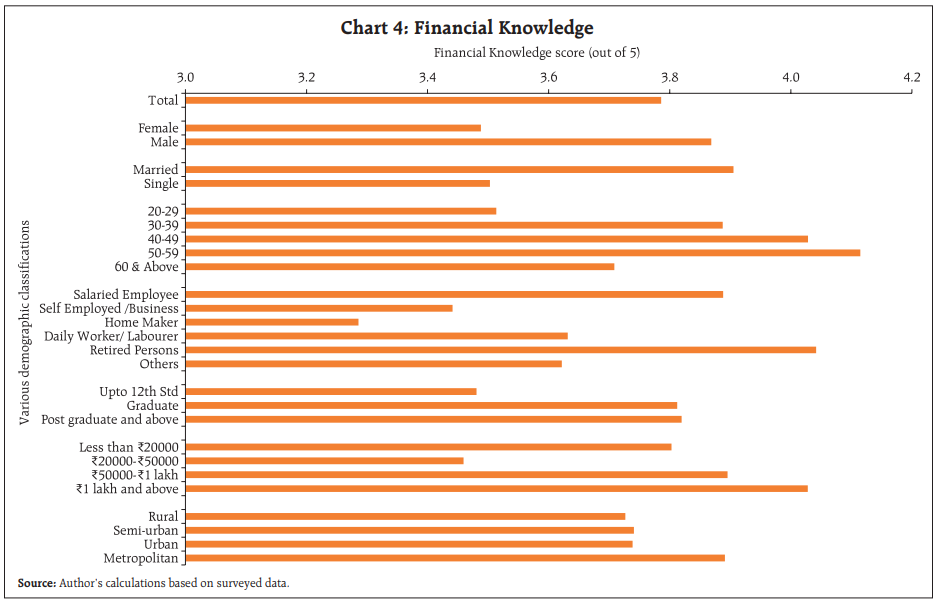

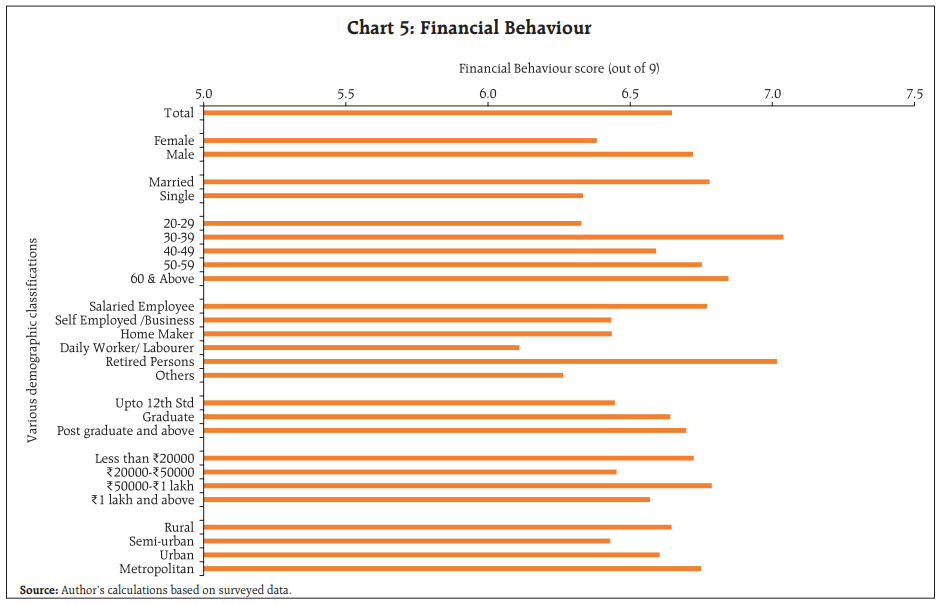

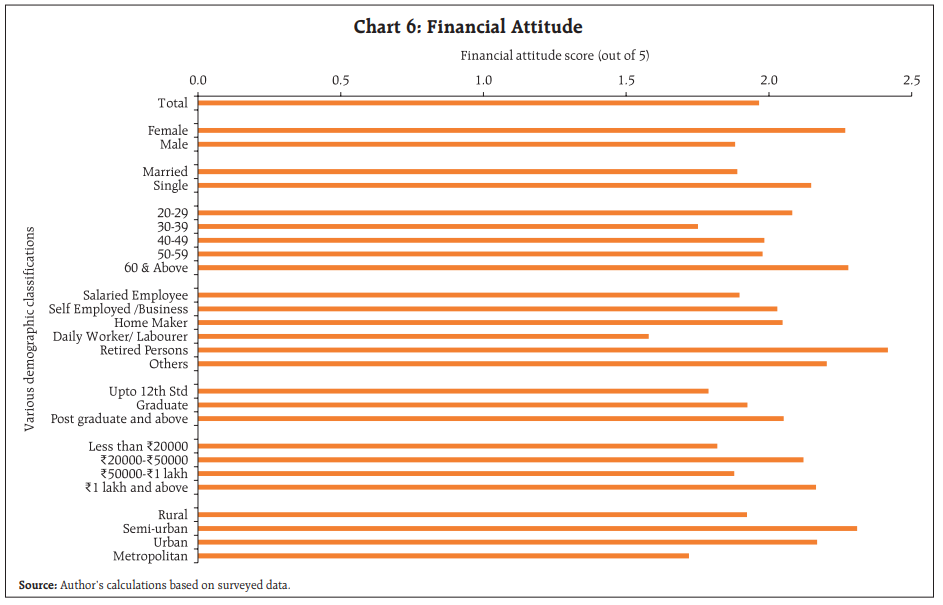

The survey assessed financial literacy across three components: knowledge, behaviour, and attitude. Each component was measured using specific questions and indicators. Below are some key findings for each component:

Knowledge: The knowledge component aimed at gauging the understanding of basic financial concepts and products. The survey included questions on topics such as interest rates, inflation, risk diversification, credit scores, and financial planning. The results revealed that there were significant knowledge gaps among the respondents. Many struggled to answer questions related to compound interest, inflation’s impact on purchasing power, and the benefits of diversifying investments. This indicates a need for improving financial education and awareness.

Behaviour: This component focused on financial practices and habits. It examined factors like savings, budgeting, debt management, and investment behaviour. The survey found that a considerable number of respondents did not maintain a budget or track their expenses regularly. Additionally, a significant portion of the respondents had limited savings and were not actively investing their money. This suggests a lack of financial discipline and the need for promoting responsible financial behaviours.

Attitude: The attitude component assessed respondents’ attitudes and beliefs towards financial matters. It explored aspects such as risk tolerance, financial goal setting, and confidence in financial decision-making. The survey results indicated that while many respondents expressed positive attitudes toward financial planning and goal setting, they lacked confidence in making complex financial decisions. There was also a significant proportion of respondents who displayed a low-risk tolerance, preferring safer but lower-yielding financial options. This highlights the importance of fostering a more risk-aware and confident attitude toward financial decision-making.

Enhancing financial literacy

Based on the survey findings, several policy implications and recommendations were drawn to enhance financial literacy in India:

Strengthen financial education: There is an urgent need for comprehensive financial education programs at various levels, including schools, colleges, workplaces, and community centres. These programs should focus on imparting knowledge about fundamental financial concepts, money management skills, budgeting, savings, and investments. Integrating financial literacy into the formal education curriculum can help equip individuals with essential financial skills from an early age. As a Board member of ayu ecosystem, an organisation that has built a comprehensive Financial Literacy curriculum starting at grade 1 i.e. age 5 (and all the way to grade 12), I believe this recommendation is key.

Promote accessible and tailored financial information: Financial information should be made more accessible, understandable, and tailored to the needs of different population segments. This can be achieved through the development of user-friendly online resources, mobile applications, and interactive platforms that provide personalised financial guidance and tools. Simplifying financial jargon and using visual aids can aid in comprehension and engagement.

Collaborate with financial institutions and employers: Collaborative efforts between financial institutions, employers, and government agencies can play a vital role in promoting financial literacy. Financial institutions can provide educational materials, workshops, and counselling services to their customers. Employers can incorporate financial wellness programs as part of their employee benefits, empowering individuals to make informed financial decisions.

Target vulnerable and marginalised groups: Efforts should be directed towards reaching out to vulnerable and marginalised groups, including women, rural populations, and low-income individuals. Tailored financial literacy initiatives, focusing on their unique challenges and needs, can help bridge the financial literacy gap and promote inclusive economic participation.

India must focus on bridging the significant financial literacy knowledge gaps, behavioural challenges, and attitudinal factors that hinder informed financial decision-making. We need a multi-faceted approach involving educational institutions, financial service providers, employers, and government bodies. By prioritising financial education, promoting responsible financial behaviours, and fostering a positive attitude toward financial decision-making, the country can empower individuals to build a more secure and prosperous financial future.

Ram Kapadia is a thought leader and entrepreneur based in Mumbai.