The digital revolution has transformed business operations across all industries including the financial services sector. It changed the need for functionality, reliability, and convenience of finance and has led to structural changes in the industry. The financial services industry saw a radical technology-led transformation over the past few years. The broader name given to this evolution is fintech. The pace of change is increasing and financial services institutions are looking to make sure that they are positioned to succeed in the future.

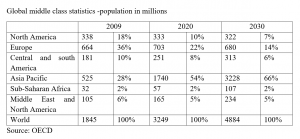

Around the world, the middle class is projected to grow 180% between 2010 and 2040. Asia’s middle class is already larger than Europe’s. Over the next 30 years, it is estimated that 1.8 billion people will move into cities, mostly in Africa and Asia, creating one of the most important window of opportunity for financial institutions. These trends are directly linked to technology driven innovation. Asia has a comparatively young population of digital natives. Asia will emerge as a key centre of technology driven innovation. Asia also has the largest inter-connectivity of flows with other emerging economies.

READ I Regulatory practices in insurance industry must evolve with technology

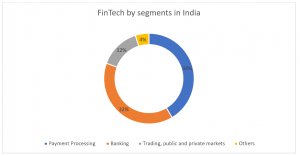

The financial technology sector in India is currently providing services in asset management, payment solutions, insurance, credit rating, and peer-to-peer payment networks. The current landscape for fintech comprises the following types of products.

The Indian economy, which has always been cash-driven, has responded well to the fintech opportunity. This happened primarily because of the penetration of e-commerce, smartphones, and access to the internet by the Indian population. MSME financing is another area where fintechs have given good results.

India is creating an ecosystem that allows startups to grow into big businesses. Fintech start-ups and large organisations are delivering innovation that was previously difficult to achieve.

READ I TechFins: Why India must stop their unregulated, untaxed run

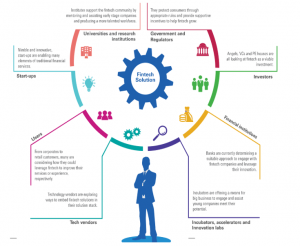

Catalysts of fintech Success in India

Multiple stakeholders have contributed to the growth of the financial technology industry in India. Some of these stakeholders are:

Commercial banks: Banks have high dependency on technology platforms such as e-wallets. They provide smoother back-end operations and customer-friendly services. Some banks are collaborating with fintechs to provide better financial services. Another way the banking sector is promoting the fintech industry is by adopting technology innovation. One of them is blockchain, a path-breaking system used to store large ledgers of data virtually. By shifting the entire gamut of data storage online, blockchain technology will eventually replace the traditional methodologies of making payments, lending funds, and updating KYC documentation.

Payments: The share of digital payments are increasing exponentially in India. Mobile payment solutions like wallets, P2P transfer applications and mobile PoS are enjoying strong user adoption, offering one-stop-shop solutions. Some players in the sector are taking advantage of policy initiatives such as payments bank licences to converge towards a hybrid model where mobile services blend with banking services.

Startup companies: Fintech Startups have an excellent potential for expansive growth. Startups are paving the way and creating initiatives toward digitising India. Demonetization encouraged citizens to go cashless, and the digital movement is becoming a reality. Currently, there are over 600 fintech startups in India across segments that could potentially improve quality and make financial services more cost-effective.

Government bodies: UPI or Unified Payment Interface is a system set up by the government of India. UPI channels multiple banks accounts into a single mobile interface to unify the citizens towards the idea of cashless India. Further, the National Payments Corporation of India launched UPI 2.0. This revised app has additional features such as increased transfer limits and the promotion of merchant transactions. Compared to its predecessor, enhanced security and a user-friendly interface are two modifications that the 2.0 offers. The government has been a driving force behind the fintech revolution.

It is clear that technology is affecting financial services in many ways. Fintech drives new business models. The sharing economy is embedded in every part of the financial system today. Blockchain shakes things up, digital becomes mainstream, customer intelligence becomes the most important predictor of revenue growth and profitability, advances in robotics and AI start a wave of re-shoring and localisation, and the public cloud becomes the dominant infrastructure model.

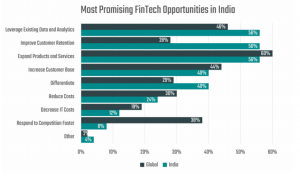

As per a PwC research report, over 95% of financial services incumbents seek to explore fintech. Technologies such as artificial intelligence, machine learning, blockchain, and IoT have a wide range of applications in the fintech industry. Fintech is changing the entire value chain of the traditional financial institutions to establish better connections with customers and provide new offerings in the market. Some of the emergent areas of opportunity for fintech evolution are as below:

Biometric technologies in banking

Digitisation in banking is leading to large-scale data. Banks need to speedily develop a strategic framework and policy mechanism to help ensure data security and promote the use of biometric technologies to prepare for future cyber-attacks. Using biometrics in banking helps provide proof of identity and strengthens the fraud detection mechanism. It also improves transparency by facilitating an audit trial and reduces the processing time significantly. Overall, it has helped increase the customer’s confidence in the banking system.

Blockchain: Blockchain is being perceived in India as a gamechanger. It can offer solutions to many problems in the fintech world. Blockchain is in a very nascent stage and is yet to mature into a mainstream application. However, the technology is still receiving favorable reviews from market players in the country and is a potential future of fintech in India.

Robo Advisors: Robo advisors in India are growing across the retail investing space. Many startups and broking firms have launched Robo advisor services in India, such as Aditya Birla Money’s MyUniverse, BigDecision, ScripBox, and Arthayantra. Demography and fintech development in India have been the prime reasons for the growing opportunities. Robo advisors distinguish themselves as the responders to the digital trend and craft a model with services offered ranging from mutual funds, portfolio allocation, and insurance plan selection to pension fund selection.

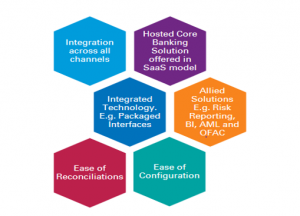

Box in bank Solutions: With digital payments and growing small finance banks in India, Bank in a Box solution is on the rise. The critical aspects of this solution are the integration of:

Bank in a Box solutions have received acceptance by small cooperatives and RRBs (Regional Rural Banks) in India, paving the way for the financial inclusion of the rural sectors of India.

Peer-to-peer lending: In India, the P2P lenders broadly focus their portfolios on microfinance, consumer loans, and commercial loans. For example, 30% of Faircent’s loans are taken by micro and SME sectors, boutique firms, and mom and pop stores; individuals take others for private purposes such as weddings, medical, and home. The growth potential of this lending market in India is vast.

Financial Inclusion: At present, the financial inclusion rate in India is very low. Many fintech companies are working in different ways to contribute toward achieving deeper financial Inclusion in areas such as microfinance, digital payments, credit scoring, and remittances.

A major problem faced by fintechs in India is that there are no regulations or guidelines set by the Reserve Bank of India and the Securities and Exchange Board of India. They are governed by banking regulations. Because of these onerous regulations, some companies find it hard to get permissions and licences on time. Many fintech companies are service-based and are, therefore, intangible. If the investors are not financially and technologically savvy, it will be tough to make them understand the value propositions, and more explanations are needed than in other industries.

One key area where fintech companies are lagging behind traditional financial companies is the human touch in operations. This issue can leave fintech companies struggling to convince big investors. Fintech is currently facing limitations in accessing a large consumer base, market expertise, brand loyalty, and capital.

Over the medium to long-term, fintech players need to challenge their business models. Also, mobiles will be the most important service distribution channel in the future. Hence, they should actively engage with customers over the medium-term. Further, Fintech players will have to invest in innovation, managing risks and building effective partnerships with big financial players. Collaboration can be the way to success for both banks and fintech companies.

Naliniprava Tripathy is an Indian economist based in Shillong. She teaches finance at IIM Shillong.