A recent study on the Indian electronics industry from the New Delhi-based think tank ICRIER titled Globalise to localise suggests that Indian policymakers’ ongoing attempts to simultaneously achieve both exports at scale (globalise) and increase the share of domestic value addition (localise) is unlikely to succeed, due to the absence of a competitive domestic ecosystem of ancillary suppliers. The study, therefore, proposes that India should adopt the mantra of “first globalise, then localise”.

The Report contends that implementing their suggestion will require a change in the existing policy regime so that the electronics industry should be able to source inputs from the lowest cost suppliers anywhere in the world until it achieves global scale. The Report’s policy suggestions are: remove duties on intermediate items, temporarily suspend localisation requirements in government procurement tenders, and accelerate integration through bilateral and regional FTAs.

ALSO READ I Electronics industry: Policy choices for manufacturing success

If these policy suggestions had come directly from the Indian Cellular and Electronics Association (ICEA) which sponsored the study, they would not generate any surprise. The underlying rationale of combining ongoing policies including SPECS (Scheme for Promotion of Manufacturing Electronics Components and Semiconductors), Preferential Market Access (Public Procurement- Preference to Make in India), the Production-Linked Incentive (PLI) Scheme and customs duty increases is to achieve a re-orientation of China-centric electronics supply chains by building local capacities in India.

There is resistance from the ICEA member companies which include foreign original equipment manufacturers (OEMs) and electronics manufacturing services (EMS) companies to re-align their supply chains that are set for China-centric sourcing models.

The policy proposals for the Indian electronics industry to “first globalise, then localise” are rendered in a report from a national-level economic research institution and warrants serious consideration. These proposals are based on a fallacious obliteration of Indian electronics industry’s existing globalisation experience of a quarter century.

READ I Hype vs Reality: Green hydrogen capacity in 2030 may fall short by a mile

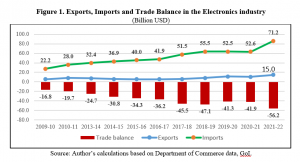

Electronics industry’s globalisation experience

The virtues of globalisation sans industrial policy have been sold to the Indian electronics industry ever since the decision to implement the WTO’s Information Technology Agreement (ITA-1) in 1997. Between 1997 and 2005, Indian tariffs on 165 products belonging to computers, telecom equipment, semiconductors, semiconductor manufacturing and testing equipment, software and scientific instruments were eliminated under the ITA-1.

From the mid-2000s, additional liberalisation was carried out by India under its FTAs with Thailand (Early Harvest Program:2004), Singapore (CECA:2005), ASEAN (2010), South Korea (2010) and Japan (2011). These FTAs extended zero duties to several non‐ITA-1 electronics products, including consumer electronics and home appliances as well as professional, medical and scientific instruments and their parts.

With only less than 4% of non-ITA-1 electronics tariff lines excluded from tariff liberalisation, the ASEAN FTA was the most damaging. The argument has been that the reduction/elimination of tariffs and enlargement of markets through these FTAs would significantly increase export-oriented FDI from MNCs linked to global value chains (GVCs) and enable India to expand exports.

Thus, Indian electronics industry’s globalisation experience has already involved:

- greater access to more competitive/low-cost parts and components from ITA-1 members globally (since 1997) and from FTA partners (since mid-2000s);

- greater access to export markets underITA-1 and FTAs; and

- increased FDI-led GVC integration that increased production scale in recent years.

If such globalisation had improved the electronics industry’s global competitiveness automatically and helped it to export sustainably, India should have been among the leading global exporters of electronics products some years ago.

On the contrary, as this author has argued since 2016, such globalisation that brought about duty-free imports created perverse incentives for local manufacturing by both domestic and foreign investors, including by reducing tariff-jumping FDI into manufacturing(even of final products).

Any advanced component ecosystem needs scale as a starting point to be viable, and entails heavy investments to setup. Under ‘zero duty globalisation’, the domestic ecosystem did not provide the requisite scale, and therefore, the incentives for either existing or new component producers to invest in the required new technologies and capital for expanding/upgrading production.

It was after customs duties were increased in a few product segments like mobile phones, TVs, etc. (under the Phased Manufacturing Program and otherwise from Budget 2016-17 onwards) that even foreign OEMs and EMS companies began setting up or expanding existing local ‘production’ in India, although still mostly in import-dependent assembly plants.

Increased FDI-led GVC integration is supposed to lead to productivity gains, through an increase in intra-industry specialisation and scale economies. But contrary to what much of the GVC literature argues, an ICSSR-funded firm-level study by the author on Indian electronics industry’s GVC participation found that that firm-level “efficiency” gains from increased GVC participation accrued mainly to the lead/parent MNC firms.

The latter control and coordinate their supply chain operations largely within their own subsidiaries and group associates. Therefore, the largest shares of value creation throughout production as well as in services were predominantly captured by the MNC headquarters, followed by their subsidiaries.

Even when some of the firms started exporting from India, the expansion in production drove significant foreign exchange outflows from these electronics subsidiaries through imports and technology payments.

These in-depth studies have established that policies solely aimed at attracting a large volume of export-oriented foreign investments into the industry for local assembly do not in themselves lead to the build-up of the domestic electronics component supplier base.

But the ICRIER Report totally ignores the evidence on the industry’s quarter century of experience with globalisation. Policies aimed at increasing the share of domestic value addition are required precisely because of the absence of a competitive domestic ecosystem of suppliers—a clear market failure under ‘zero-duty globalisation’.

As several technologically advanced countries have done, a fixed period of moderate protection, demand creation/augmentation through government procurement of national products, ingenious policies to promote backward and forward linkages by MNCs, and targeted state-support for R&D investments and technology upgradation are crucial for generating sufficient domestic demand for locally manufactured products/parts and components.

As discussed in the book Industrial Policy Challenges for India, the literature on East Asian industrial and trade policies presents the following stylised facts:

- The development trajectories of countries with advanced indigenous electronics industries such as South Korea, Taiwan, Singapore and China have involved simultaneous trade strategies of import substitution and export promotion, along with various combinations of sector-specific industrial policies for upgrading technological capabilities and skills.

- Forward and backward linkages have been promoted through performance‐linked incentivisation for reducing imports as well as other foreign exchange outflows on account of technology and services payments.

- The risk of failures associated with selective state promotion of industrial activities through subsidies has been managed with mechanisms for monitoring performance and rectifying state assistance.

Additionally, governments of technologically advanced countries have underwritten, and continue to underwrite, the higher cost of developing advanced technological capabilities by national firms—through direct and indirect subsidies (including subsidised financing), government procurement of off-the-shelf and emerging innovative national products and industry-specific infrastructure provisioning.

A test of state’s strategic capacity

The combination of recent Indian policies and programs, despite their weaknesses in design and implementation, are part of an ongoing attempt to create greater policy-driven incentives for increasing the scale of domestic manufacturing as well as domestic value addition. These include the increase in basic customs duties, preferential market access for products with higher domestic value addition through government procurement, and the PLI Scheme.

Globally, concerns related to geopolitical uncertainties, supply chain disruptions and digital security are driving several nations’ strategic industrial policy efforts to build up their indigenous electronic segments and related ecosystem on a mission mode. Yet India faces the tragedy of one of its national research institutions advocating that it is foolhardy to pursue policy objectives to improve domestic value addition and build up national capabilities.

Indian government’s strategic capacity will get reflected in its ability to rise above short-term and sectarian interests, including those of import-dependent assembly-based exporters.

In the ongoing shift of firms’ operations away from a regime of semi-knocked-down (SKD) assembly towards completely-knocked-down (CKD) assembly, it is critical for India to maintain strategic tariff manoeuvring, along with ingenious policies for increasing domestic value addition by foreign and indigenous companies.

It is important that the duration of various ongoing scheme benefits remain limited and benchmark criteria are adhered to. At the same time, new policies must be implemented dynamically, to continuously support indigenous technological upgradation and innovations.

Meanwhile, policymakers must continue efforts to improve the design and implementation of policies to increase their cohesiveness and effectiveness in creating an advanced domestic supplier ecosystem. Without incentivising greater backward and forward linkages, a large share of the value from increased product sales, to which much of PLI incentives are tied at present, will continue to drain foreign exchange to the brand-owning parent firms and other foreign patent holders.

With increasing digitalisation of value chains, it is critical for India to build up domestic synergies between the indigenous design, engineering and software skills that have accumulated with state support over several decades. Therefore, design-led incentives must be increased to make an actual difference.

The continuation of demand creation/augmentation through government procurement of domestically designed and manufactured products has a critical role to play, not only in enabling scale economies and greater investments in technology upgradation by indigenous companies, especially SMEs, but also in rapid commercialisation of indigenous innovations.

It is crucial that design of policies or their implementation must not create perverse incentives for indigenous R&D-intensive production. Simultaneously, the state has to make large investments in R&D in emerging technologies and industry-specific infrastructure, support SMEs in technology upgradation, testing and patenting, as well as promote commercialisation of indigenous innovations.

ALSO READ I Electronics industry: Policy choices for manufacturing success

(The author is an economist based in Delhi. She would like to acknowledge the comments received from PVG Menon, Smita Purushottam and Anirban Dasgupta on a different version of this article. However, the author is solely responsible for the views expressed here.)