By P Vinod Kumar

An election-time review of Kerala economy: Growing inequality, the need for diversity and saving the planet are some of the most talked about topics and shared concerns among policy makers across the world. While the Occupy Wall Street movement has shot the inequality theme to the forefront in the policy discussions, the #MeToo movement became the tipping point for the growing call for diversity.

A series of extreme weather events that played out spectacularly across national theatres forced the governments, global funding agencies and financial institutions to put the ESG (environment, social and governance) reporting on top on their investment agenda. Taking these themes to the core of Kerala’s development debate and discussions and translating them into actionable plans looks inevitable since Kerala has never left a global opportunity to go waste since it remains India’s most globalised state by many metrics and standards.

READ I India’s war on Covid-19 a success story of triple helix model

Rival fronts ignore concerns over Kerala economy

Curiously, the rival political formations in Kerala – the United Democratic Front led by the Congress and the Left democratic Front led by the CPM — seem to have blissfully ignored the shared concerns of policy makers in their election manifestoes. Instead, they chose to dust out their old promises to shower freebies ranging from an increase in direct transfer of cash to generating employment in lakhs without giving details about how they plan to achieve them when the state has little fiscal space left for expansionary policies. There are promises to set up free bill hospitals when there are already a good number of them operating across the state.

Though it is raining promises from left, right and central political formations with an eye on votes, the colour-coded political fronts are turning their back on the major global concerns, exposing their ideological bankruptcy and lack of interest in addressing issues of sustainability. It is ironical since walls across the state were once adorned by political heroes or villains from Stalin and Saddam Hussain to George Bush and Barack Obama as rival fronts courted global ideas to woo local electorate.

It is disturbing that none of the alliances that vie for votes have opened up their minds on the state of the Kerala economy and how will they find money to fund all the costly welfare schemes. It is revealing and rewarding for many to reread the previous manifestoes of the rival fronts. It looks like history is repeating, now as a farce. High time they made an effort towards a course correction.

READ I Foreign Trade Policy: Protectionism without strong local industry may spell disaster

The state of Kerala economy

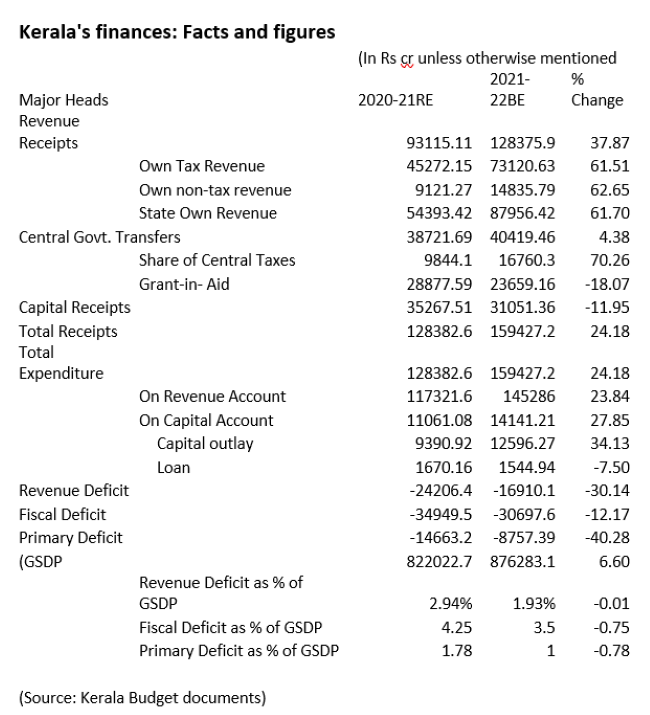

The first stop for anybody who wants to understand the state finances is the budget documents. A nuanced reading of the Budget speech along with the accompanying headline numbers throws up more questions than answers. While it provides a fiscal guidance for the next few years, the election year budget failed to offer new ideas about the shape of recovery in Kerala economy. The general economic growth is penciled in to grow by a conservative 6.6% in the next fiscal from its Covid-19 lows, but a private report has disputed this number by predicting a much higher 13.5%, a notch lower than their growth forecast for the national economy.

This should be music to the ears of policy makers as such elevated growth print is sure to bring more revenues while reducing deficit numbers. Such a higher growth print also makes the budget projections of higher revenue – both tax and non-tax – more realistic. If that is a big positive for the Kerala economy going forward, there is also a notable expenditure switching written all over the state budget. While the overall expenditure is budgeted go up by 24%, what is more encouraging is the lower-than-expected hike in revenue expenditure considering the higher salary and pension bills the government has to foot in from April 1 because of the revised salaries and pensions. And if that is not enough, the state budget 2021 has provided for a 28% hike in capital expenditure and 34% increase in capital outlay. (Table I)

There is no surprise in the marked shift in the government’s spending pattern since finance minister Thomas Isaac pushed ahead with his idea of rolling out a Marshal Plan to rebuild the Kerala economy after a flash deluge left the state economy devastated. It seems that his new found love with Keynesian economic praxis started working as the budget struck a delicate balance between political exigencies of the election year with cautious spending by allocating money to productive sectors including education and healthcare.

Arguably, a major part of the credit for the improvement in the quality of the balance sheet of Kerala economy will go to the decision to fund infrastructure projects through off-budget borrowings. Predictably, this has kicked off a barrage of criticism from deficit vigilantes who see red in the high cost of financing such debt. But they conveniently choose to ignore the fact that the junk rated bonds issued by the state government through its flagship development finance institution KIFB invariably and inevitably have to bear a higher interest rate to attract investors.

The point here is that the critics of KIFB misses the larger picture that the state government bonds counter guaranteed by the RBI turned out to be a roaring hit among investors despite its junk ratings. By all standards, it was perhaps the best option left with the state government to finance the infrastructure mission of such scale. The results of that policy may take some time be visible as the invisible multiplier effect from such spending will play out only with a lag. The KIFB experiment has been replicated by the Union government, which has set up its own version.

READ I Step up Covid-19 vaccination drive to stop the second wave

Legacy issues troubling Kerala economy

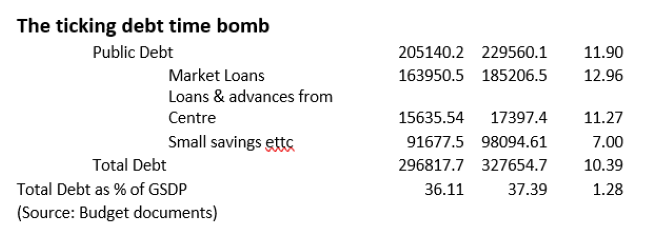

A major stumbling block that the state faces is the legacy issue of mounting debt stock, thanks to the past profligacy. It looks like Kerala cannot escape from its history of living out of borrowed money as three key components in expenditure budget – salaries, pensions and interest payment – remain stubborn and blotted. While the total debt of the Kerala government is budgeted to grow by a tad over 10%, what is more disturbing is the 13% increase in interest bearings loans taken from banks and financial institutions. (Table II)

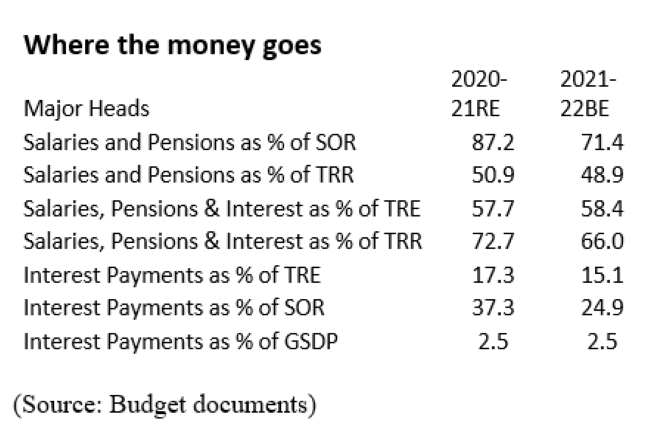

Salaries, pensions and the interest outgo account for 96% of the state’s own tax revenue (SOR), which means that of every Re 1 earned by the government in revenues, 96 paise go to foot in the salary and pension bills and debt servicing. (Table III). However, there are some bright spots in the otherwise gloomy picture as the share of salaries, pensions and interest outgo as a percentage of state government revenue is declining in a progressive fashion.

While the share of salaries and pensions in the state government’s income has declined from 87% in 2020-21 to 71% in 2021-22, the interest outgo is budgeted to shrink by almost 12% from 37% to 25% during the next financial year. This may perhaps be due to the state’s higher revenue collections.

READ I Gathering storms: The perils of ignoring the water crisis

Need a new development manifesto

All these facts and figures suggest that the new administration in the state secretariat needs to do a lot of soul searching to fix the economic fault lines that are running deep. A nuanced thinking to put development back to the agenda is badly needed. For this, a new set of priorities based on a broader political consensus may be in order. Administrators may have to shed many a shibboleth and realise that the Kerala economy is on a road that leads to nowhere.

The dominant narrative on Kerala economy always veers around a singular theme – the so-called Kerala Model and its doubtful sustainability. There is no denying that the oversized government sector with its attendant salary and pension liabilities along with legacy interest cost remains as a major drain on the state exchequer. This forces the government to borrow from every possible source to make both ends meet.

An attempt has been made by the Pinarayi Vijayan government that came into power in 2016 to bring a semblance of discipline in public spending by following some best practices in public finance as well as pushing some time-tested Keynesian economic policies — economy in expenditure, deft debt management and doubling down of job creating, income generating infrastructure projects.

The success of these policies would depend on the incoming government’s resolve to chug along this not-so-beaten path while managing debt in a macro-prudential manner and sprucing up the public goods space. Deficit reduction may have to wait till the state redeems itself from the weight of mounting debt overhang through accelerated growth, leading to all-round development.

(P Vinod Kumar is Kochi-based independent economist and commentator. Views expressed in this article are personal.)