Five months into his second term, President Donald Trump has done more than tweet laser-eyes on Bitcoin. He has signed two executive orders—one creating a President’s Working Group on Digital Assets, another floating a strategic bitcoin reserve—and turned a $10,000-a-plate dinner with backers of the $TRUMP memecoin into Oval Office policy theatre. The message is unmissable: Washington will court the crypto vote and the crypto lobby in equal measure.

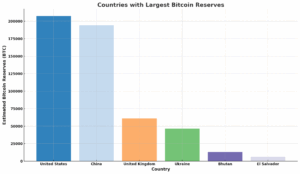

The aftershocks are global. Pakistan, otherwise teetering on an IMF lifeline, has inked a memorandum with World Liberty Financial, a firm tied to the Trump family, to build South Asia’s first sovereign Bitcoin reserve. Islamabad hopes the optics will impress the White House; its critics fear a replay of every boom-and-bust experiment that has ended with capital flight and a begging bowl.

READ I Repo rate cut done—now the hard work of reform begins

Alarm bells in Washington, Frankfurt—and Delhi

Technocrats are aghast. Gita Gopinath, First Deputy Managing Director of the IMF, warns that the unmonitored proliferation of crypto assets in developing economies could disintermediate banks, dollarise entire economies and weaken already fragile tax bases. European Central Bank president Christine Lagarde recently told the International Monetary and Financial Committee that stable-coins—tokens pegged one-to-one to fiat currencies—“may look harmless at $200 billion, but at $2 trillion they become a run risk for the global system.”

That $2 trillion figure is no scare tactic. A bipartisan Bill before the US Congress—the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act—would allow licensed issuers to float dollar-backed tokens so long as every coin is matched by a dollar or a super-safe Treasury bill. Standard Chartered reckons the float of stable-coins could jump 10-fold if the Act becomes law. Senator Elizabeth Warren calls the legislation “a gift to Wall Street in fintech clothing,” pointing out that retail holders would get no Federal Deposit Insurance protection even as issuers reap windfall profits.

For Pakistan the stakes are existential. A Bitcoin reserve may woo a tweet from Trump, but it also hands speculators an escape hatch: if the rupee wobbles, money can flee at the tap of an app. The central bank’s ability to defend its currency—already constrained by thin reserves—could evaporate overnight. Crypto zealots call this market discipline; economists call it a recipe for sovereign insolvency.

India’s half-way house

India has so far opted for what might be called a half-embrace, half-rebuff. Crypto profits face a punishing 30% tax. Every sale attracts a 1% tax deducted at source, and exchange fees attract GST. Crypto intermediaries are classified as “reporting entities” under the Prevention of Money-Laundering Act, which means they must file suspicious transaction reports like banks.

Yet there is still no comprehensive law. In 2021 the Supreme Court quashed the Reserve Bank of India’s 2018 circular that barred banks from servicing crypto firms. Earlier this year the Court compared Bitcoin trading to an “elegant form of hawala” and asked New Delhi for a clear-cut policy. RBI Governor Sanjay Malhotra echoes the concern: unregulated stable-coins, he says, would “undermine monetary sovereignty and financial stability.”

The result is a policy vacuum. Taxes are high enough to push some trading to Singapore or Dubai; supervision is patchy; investors have little legal recourse. An inter-ministerial group is drafting a discussion paper, but the global context is shifting faster than the committee can write.

A five-point roadmap for crypto regulation

Given these developments, the question naturally follows: what specific course of action must New Delhi now chart to safeguard the rupee, protect its financial system, and still leave space for responsible innovation?

Licence—don’t prohibit: Blanket bans drive activity underground or offshore, depriving regulators of visibility while doing nothing to quash demand.

Ring-fence the rupee: Retail holdings of dollar-pegged stable-coins should be capped. Any rupee-linked token must keep full, high-quality reserves with supervised banks and submit to daily disclosure.

Enforce the FATF “travel rule” end-to-end: Exchanges, wallet providers and payment gateways must attach know-your-customer data to each transfer so that illicit flows can be traced in real time.

Copy the G20 roadmap India itself helped draft in 2023: Aligning domestic rules with global norms will prevent regulatory arbitrage and reassure foreign investors.

Accelerate the retail e-rupee: A central-bank digital currency offers households a safe, low-cost alternative without ceding ground to privately issued coins.

The stakes for monetary sovereignty

Crypto’s promise is real: cheaper remittances, programmable contracts, a shot at financial inclusion. But so are the externalities. At scale, stable-coins could become the new money-market funds of the shadow banking system—yielding in good times, sparking bank-run dynamics in bad.

President Trump’s bet is that America, by blessing dollar-backed tokens, can cement the greenback’s dominance deep into the digital era. India must decide whether to draft the rule-book—or be ruled by someone else’s.

Regulation is not a romance; it is insurance. The rupee, unlike a meme coin, underwrites the savings of 1.4 billion people. Before the global tide of digital dollars rises, New Delhi must build the flood-walls. If the government hesitates, it may soon discover that the cost of reclaiming lost monetary ground is far higher than the price of writing smart rules today.