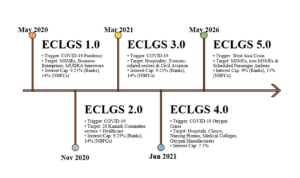

The Union Cabinet has approved Emergency Credit Line Guarantee Scheme 5.0 (ECLGS 5.0) to help MSMEs, non MSMEs and scheduled passenger airlines manage short-term liquidity stress caused by the West Asia crisis. The scheme offers 100% guarantee cover for MSME loans and 90% cover for non-MSMEs and airlines through the National Credit Guarantee Trustee Company Ltd. It targets additional credit flow of ₹2.55 lakh crore, including ₹5,000 crore for airlines.

The scheme is narrower than it first appears. MSMEs and non-MSMEs must have existing working capital limits as of March 31, 2026. Airlines must have outstanding credit facilities on that date. In both cases, accounts must be standard. The additional credit is capped at 20% of peak working capital utilisation during Q4 FY26, subject to a ceiling of ₹100 crore. Airlines can borrow up to 100% of peak credit outstanding, capped at ₹1,500 crore per borrower, subject to conditions. Loans must be sanctioned by March 31, 2027.

READ | MSME credit boom bypasses India’s smallest firms

The purpose is clear. Firms exposed to higher freight costs, costlier crude, export delays, disrupted supply chains and working-capital pressure need temporary support. Airlines face the added burden of higher aviation turbine fuel prices, airspace closures, lower aircraft utilisation and route disruption.

A credit guarantee can prevent a liquidity shock from becoming a solvency shock. It can also keep lenders from withdrawing credit when risk aversion rises. But ECLGS 5.0 should not be mistaken for MSME reform. It is an emergency instrument. Its value lies in preventing disruption. Its limits were visible in the earlier rounds.

The original ECLGS was launched in May 2020 during the Covid-19 shock. It offered government-backed, collateral-free additional credit to firms facing a revenue collapse. The scheme was later expanded to stressed sectors such as hospitality, tourism, healthcare, aviation and oxygen-related industries. Earlier ECLGS rounds expired on March 31, 2023.

ECLGS impact was uneven

The problem was not that ECLGS failed. It did what emergency credit schemes usually do. It bought time.

The problem was distribution. Larger and more bankable enterprises were better placed to secure additional credit. Micro units, informal firms and first-time borrowers had weaker balance sheets, thinner documentation and less bargaining power with lenders.

READ | Viksit Bharat needs a different MSME playbook

This is not a design accident. Credit guarantee schemes work through banks and NBFCs. They reduce lender risk. They do not create borrower capacity. Firms outside the formal credit system remain difficult to reach even when the state absorbs a large part of the default risk.

The eligibility rules under ECLGS 5.0 reinforce this point. The scheme is available only to borrowers with existing working capital limits or outstanding credit facilities as of March 31, 2026, and only if their accounts are standard. That makes operational sense for lenders. It also means firms already outside formal credit channels will remain outside the main benefit stream.

ECLGS loans and default risk

There was also a repayment problem. Interest-rate caps reduced the risk of extreme pricing. But they did not make credit cheap for all borrowers. Smaller firms often depended on NBFCs because they had weaker access to banks. That meant higher borrowing costs and greater repayment stress.

The RBI’s Financial Stability Report of June 2023 gives the clearest evidence. Scheduled commercial banks accounted for almost 90% of ECLGS disbursals, worth ₹2.91 lakh crore. Contact-intensive services and traders were the major users. One-sixth of ECLGS accounts and one-twentieth of the amount disbursed had turned non-performing. Stress was concentrated in micro enterprises, where nearly one-fifth of borrowers and one-tenth of the amount disbursed had become delinquent.

This is a useful distinction. The stress was wider by number of accounts than by amount. That points to distress among small borrowers. It does not show a systemic banking crisis. It shows the vulnerability of small enterprises that survived the first shock by taking on more debt.

This is the central policy lesson. A guarantee can move credit. It cannot restore profitability. It cannot repair broken supply chains. It cannot raise the bargaining power of small firms facing delayed payments. It cannot substitute for formalisation, infrastructure and technology adoption.

MSME credit gap remains large

India’s MSME finance problem predates Covid-19. The RBI’s U.K. Sinha Committee estimated the MSME credit gap at ₹20-25 trillion. The IFC’s study on financing India’s MSMEs estimated the addressable credit gap at ₹25.8 trillion.

This gap persists because MSME lending is still constrained by information, collateral and cost. Banks continue to rely on immovable collateral. Micro and small firms often lack titled assets, audited accounts and formal cash-flow records. First-time borrowers face the steepest barrier.

Informality compounds the problem. Informal firms have weaker access to institutional finance, government schemes and legal remedies. They also remain less visible to lenders that increasingly rely on data-based credit assessment.

READ | India’s MSMEs face a cash-flow crisis as Iran war prolongs

The weaknesses are familiar. They include poor logistics, unreliable infrastructure, limited testing facilities, low technology absorption, weak management capacity and delayed receivables. A loan can cover a wage bill or a supplier payment. It cannot remove these bottlenecks.

Credit guarantee is not MSME reform

ECLGS 5.0 is best understood as a shock absorber. It may help firms affected by the West Asia crisis avoid abrupt closure. It may protect jobs in firms that are otherwise viable. It may prevent lenders from tightening credit at the worst moment.

But repeated reliance on such schemes reveals a deeper weakness. The MSME sector remains undercapitalised. Many firms have low reserves, limited market power and weak access to formal finance. External shocks expose these weaknesses quickly.

The policy risk is that emergency credit becomes a substitute for reform. That would be a mistake. India needs better invoice discounting, faster payment discipline, deeper cash-flow lending, stronger credit information systems, cluster infrastructure, testing facilities and technology support. These are slower reforms. They are also more important.

Credit support may keep enterprises alive. Without institutional finance, infrastructure and technology, debt-financed survival can become financial fragility. ECLGS 5.0 should buy time. It should not become another reason to postpone the harder MSME agenda.

Sanjana is a Research Scholar, and Santosh Kumar Das Faculty at Institute for Studies in Industrial Development, New Delhi.