Sovereign credit ratings have a major influence on global investment flows and in shaping the borrowing costs for nations. However, the objectivity of these ratings is often overshadowed by a bias that favours Western interests, primarily driven by the Big Three credit rating agencies – S&P Global Ratings, Moody’s, and Fitch Group.

Geopolitical influences also play a role in shaping the assessments of credit rating agencies. Often, these ratings are not mere reflections of economic metrics, but are swayed by political relationships and strategic interests. This geopolitical bias can lead to skewed ratings that favour allies of the dominant economic powers, further distorting the global financial system and undermining the objectivity of credit assessments.

READ I Unemployment figures hide widening job gap in South Asia

Western hegemony in credit rating

The dominance of these agencies, based in the US and Europe, extends beyond simple market control; it leads to profound injustice embedded in the system. The financial crisis of 2007–2008 laid bare their complicity, as their overly optimistic pre-crisis evaluations of failing institutions and risky assets contributed significantly to the global economic crisis. Their history of assigning favorable ratings to economies such as Greece and Turkey, only to see these nations experience severe financial crises, casts doubt on the reliability of their assessments. Despite the need for greater accountability, these agencies continue to wield excessive influence over sovereign ratings.

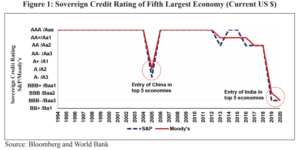

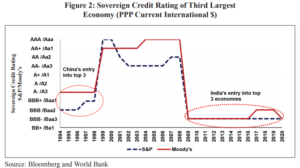

India finds itself caught in this web of these skewed assessments. Despite its rapid ascent to become the world’s fifth-largest economy and a hub of growth, the Big Three consistently underrate its creditworthiness. While India’s economic fundamentals are strong, the opaque criteria used by Western agencies cast a shadow, limiting its access to international capital under favorable conditions.

India has been vocal in seeking clarity on the criteria used by international rating agencies to determine credit ratings, pushing for a move from subjectivity to transparency. The nation has called for a reform of sovereign credit rating methodologies to more accurately reflect a country’s ability and willingness to meet its debt obligations. Despite these efforts, India’s credit rating remains unchanged due to persistent biases, while countries like the US benefit from significantly lower borrowing costs, with interest rates at about half those imposed on India. Unfortunately, the prospect of change remains dim in the near future.

India pays price of skewed ratings

For 15 years, India’s sovereign rating has stagnated, highlighting the difficulties it has faced. Under the governance of the UPA-led government, marked by modest economic growth of three percent and numerous corruption scandals, foreign investors maintained a cautious stance. Consequently, the Big Three assigned India their lowest investment grade. This disparity becomes particularly glaring when compared with Western economies that, despite questionable fiscal discipline, enjoy higher ratings based on assumed defaults. India’s story of fiscal prudence and economic resilience is overlooked, overshadowed by outdated methodologies and subjective evaluations.

India is currently the fifth-largest economy, a testament to its growth potential. Recent economic indicators reveal a significant turnaround, with the economy expanding at an impressive rate of 7.5%. This success is not accidental but the result of decisive reforms carried out by the government over the last decade, which have accelerated growth, revitalised the financing and equities markets, and boosted domestic consumption. Despite the setbacks from the Covid crisis, India has regained its stability, reaffirming its appeal to foreign investors.

The impact of the biased credit ratings extends beyond mere numbers; they directly affect the economic prospects of emerging markets. By imposing higher borrowing costs and deterring investment, unjustifiably low ratings can stifle economic development and exacerbate the challenges faced by these nations. This creates a vicious cycle where countries are unable to break free from the constraints imposed by skewed financial assessments.

But India’s patience is running thin as it stands at the threshold of a new era in the 21st-century global economy. It is time for India to break free from the constraints of Western dominance and chart its own course toward financial sovereignty.

The case for India to establish its own credit rating agency is strong. Such an institution would transform the global financial system, shifting from opaque subjectivity to transparent objectivity. Learning from China’s strategic moves, India should begin its journey to set up its own agency, emphasising inclusivity and accuracy. By adopting a data-driven approach, this agency would rigorously evaluate key economic strengths, fiscal resilience, and institutional integrity, eliminating any room for biased interpretation.

As India pushes for its own credit rating agency, international cooperation could also be explored as a means to enhance the credibility and acceptance of new institutions. By collaborating with other nations that share similar grievances and aspirations, India could help foster a more balanced global rating system. Such partnerships could lead to the creation of a multinational credit rating agency that not only serves the interests of the Global South but also adheres to a more equitable evaluation framework.

As Western financial institutions continue to dominate, India is well-positioned to challenge the status quo and reshape the global financial system. The establishment of a new global credit rating agency, led by India and involving other nations, is a crucial step towards dismantling the entrenched Western influence over global capital allocation. This endeavor is about more than economic empowerment; it represents a movement against the longstanding Western control over global resource distribution, introducing a new era of fairness and equity in international finance.

The road ahead will be filled with challenges and scepticism, but the potential rewards are substantial. Establishing a homegrown credit rating agency would not only empower India but also pave the way for a more equitable global financial system. India’s initiative to lead the creation of a new global credit rating agency holds immense promise for empowering the Global South and rebalancing the scales of international finance. By spearheading this effort, India can ensure that the perspectives and priorities of developing nations are duly considered in assessing sovereign creditworthiness.

However, the effort requires caution and the engagement of key global stakeholders like the International Monetary Fund and the World Bank. While it is important to challenge the dominance of the Big Three, recognising the value of collaborative processes in global finance is crucial. Engaging with established institutions will help understand the complexities of the financial system. This collaborative approach is essential for breaking down old networks and building a just and transparent global financial architecture.

Srinath Sridharan is a strategic counsel with 25 years experience with leading corporates across diverse sectors including automobiles, e-commerce, advertising and financial services. He understands and ideates on intersection of finance, digital, contextual-finance, consumer, mobility, Urban transformation, and ESG. Actively engaged across growth policy conversations and public policy issues.