Importance of retirement planning: Everybody needs a good life after retirement, but not many people actually end up planning for it. The third age, also called the golden years of adulthood, is generally defined as the span of time between retirement and the beginning of age-imposed physical, emotional and cognitive limitations. That would roughly fall between the ages of 65 and 80. All of us need to do retirement planning to be financially independent during that time.

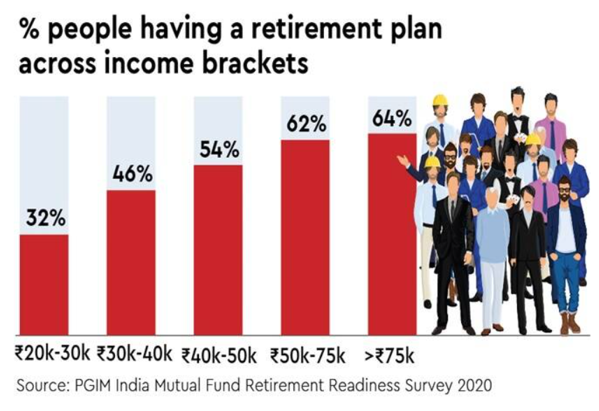

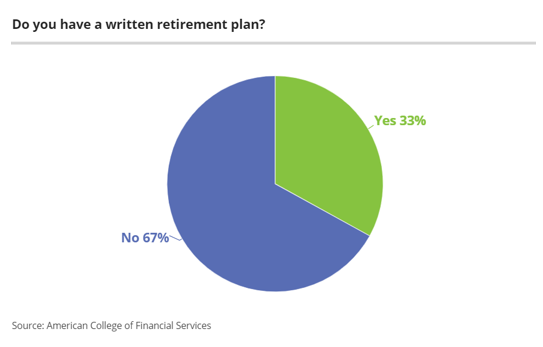

According to research conducted by PGIM India Mutual fund in 2020, 51% of Indians do no retirement planning and are worried about the cost of living, healthcare issues and lack of family support in future. Surprisingly, the proportion of American population who do not do retirement planning is similar. Nearly 50% of American citizens have less than $100,000 saved in their retirement fund. The amount may look big, but it is much smaller than what it should be.

READ I Towards a robust public health system based on universal healthcare

The retirement scenario might look similar in percentage terms. However, if certain factors are taken into account such as living expenses, lifestyle, goals etc., much clearer conclusions can be drawn. For instance, a corpus of Rs 50 lakh is considered to be a safe bet for retirement in India, but, $100,000 which is roughly Rs 72 lakh is considered below the mark in the US. The reasons are high living cost and high expenses.

The only reason why people fail to do retirement planning is what we call ‘investor ignorance’. People often think it’s either too early or it’s too late to save money. This may not always be true. What people don’t realize is that all the investments they do today (for the future), will happen concurrently while managing their present expenses. So, the later one begins planning his/her retirement, the more the burden of investing a higher amount for retirement. Similarly, if one is already near or past his/her retirement, it is natural to assume that it’s too late and there’s nothing that you can do about it. But starting somewhere is much better than not starting at all.

READ I Can Tamil Nadu government create a South Indian Miracle?

There are a number of retirement plans available in both the countries, and the most common plans which are accessible to majority of the citizens are listed along with their benefits.

Retirement options for Indians

Senior citizens saving scheme: SCSS is available only to senior citizens or to people who retire early. SCSS can be availed from a post office or a bank by anyone above 60.

New Pension Scheme: NPS is open to all individuals across the country. The National Pension System is a voluntary defined contribution pension system. It is the instrument in which the entire corpus escapes tax at maturity and entire pension withdrawal amount is also tax-free.

Employee’s Provident Fund: EPF is the most common saving instrument in India. It was introduced as a retirement product. The current rate of return from EPF is fixed at 8.5% per annum. EPF is tax free and withdrawal is also tax free if there is continuous service of 5 years.

READ I The Model Tenancy Act 2020: Towards a maintainable, inclusive rental market

Retirement planning options for Americans

401(K): This is an employer-sponsored retirement plan to which certain eligible employees based on pre-set criteria can make tax-deferred contributions from their salary or wages.

403(b): This is a retirement account for certain employees of public schools and tax-exempt organisations. Participants mainly include people from the public sector such teachers, school administrators, professors, government employees, nurses, doctors, and librarians.

IRA: This is an account set up at a financial institution that allows an individual to save for retirement with tax-free growth or on a tax-deferred basis. The 3 main types of IRAs each have different advantages:

In traditional IRA, you make contributions with money you may be able to deduct on your tax return, and any earnings can potentially grow tax-deferred until you withdraw them in retirement.

In Roth IRA, you make contributions with money you’ve already paid taxes on (after-tax), and your money may potentially grow tax-free, with tax-free withdrawals in retirement, provided that certain conditions are met.

In Rollover IRA, you contribute money “rolled over” from a qualified retirement plan into this traditional IRA. Rollovers involve moving eligible assets from an employer-sponsored plan, such as a 401(k) or 403(b), into an IRA.

READ I Opportunity beckons India’s higher education sector

Benefits of retirement planning

Tax benefits: Retirement planning helps in tax saving. For example, investments in PPF and 401(K) qualify for tax exemption. These are long-term investments suitable for retirement. There are variety of instruments available for retirement planning at the same time to qualify for tax saving.

Cost saving: Planning for retirement at a young age helps in reducing the cost. For example, in an insurance policy the premium to be paid will be lesser when the policyholder is young, whereas getting insurance during retirement becomes costly.

Helps tackle inflation: Investing in retirement helps beat inflation. Putting money in savings account will not generate high returns to beat the inflation. In other words, the returns generated will not be sufficient enough to live an uncompromised life.

Presently, a major proportion of people, in both India and the US, don’t pay much attention to their retirement and this in turn, leads to compromising on their comfort in the later stage of life. Having a strong financial standing not only makes you better off, but it also reduces your dependency on others for money. Being financially independent is, in itself, a great achievement in life. It shows how great a planner one is. Here are 5 points one can follow to start with their retirement planning.

- Start early.

- Keep aside minimum 20-30% of your income for retirement.

- Don’t save what is left after spending, rather spend what is left after saving.

- Do proper research before selecting any retirement plan.

- Always diversify your portfolio with a balanced combination of insurance, retirement schemes, mutual funds, equity etc.

(Dr Badri Narayanan Gopalakrishnan is founder and director at Infinite Sum Modelling. Anish Uppal is a researcher at Infinite Sum Modelling and founder, The Trader’s Journal.)

Dr Badri Narayanan Gopalakrishnan is Fellow, NITI Aayog. Views expressed are personal.