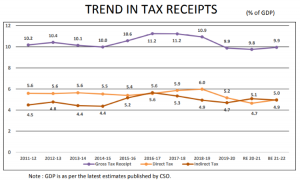

Union Budget 2022: The last financial year was one of the most challenging ones for the Indian economy. However, the first two quarters of the current fiscal year have given indications of a strong rebound. The gross tax revenue collections in the April to October period have risen by 55.79% compared with the same period of the previous year. The annual gross tax revenue collections are likely to surpass the Budget 2021 estimates.

Finance minister Nirmala Sitharaman will present her fourth Union Budget on February 1, 2022 amid these encouraging trends and a hope that the third wave of the Covid-19 pandemic would be less lethal than the first two. This article focuses on the key macro indicators relating to non-resident taxation that are expected to be addressed in the upcoming Budget.

READ I Will global minimum tax disrupt India’s tax regime?

Budget 2022 and OECD two-pillar solution

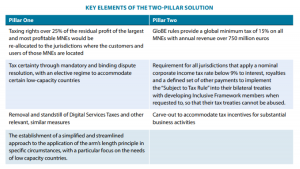

Being a market jurisdiction and a victim of the challenges arising from the digitalisation of the economy, India has been on the forefront of the OECD’s BEPS project. Earlier this year, the inclusive framework of which India is a member reached a definitive milestone with 136 of 141 OECD members agreed on the two-pillar solution that involves a global minimum tax rate of 15%. The solution may require certain amendments in the domestic tax law as well. The key ones are as follows:

- A domestic taxing right consistent with the design of Amount A, or the share of residual profit allocated to market jurisdictions using a formulaic approach, under Pillar I.

- Provisions relating to Income Inclusion Rule (IIR) and Undertaxed Payment Rule (UTPR) under Pillar II aimed at ensuring a global minimum effective tax rate of 15% for large multinational businesses.

Given that the model rules covering IIR and UTPR are yet to be released and the model rules for domestic legislation to implement Amount A are expected to be developed by early 2022, it is less likely that Budget 2022 may have proposals in this regard. However, if there is any development regarding the model rules before the Budget is approved by Parliament, the government may consider incorporating suitable proposals through amendments to the Finance Bill.

READ I The global minimum tax: A great beginning despite inbuilt biases

Equalisation levy

The equalisation levy is proposed to be withdrawn once Pillar I is effective. India has already reached an agreement with the United States in this regard. However, in the interim, clarity is required on some of the following key issues:

- Various terms used in the EQL provisions which are not defined (e.g., digital facility, electronic facility, platform);

- There is no specific exclusion for intra-group transactions although the legislative intent may not be to include such transactions under the purview of EQL;

- The terms “online sale of goods” and “online provision of services” have been defined to include any one or more of the five specified online activities which may bring almost all the cross-border transactions under EQL; and

- Interplay between FTS / Royalty and EQL, especially in a scenario where the position taken by the taxpayer is not accepted by the tax authorities.

Taxpayers expect that the Union Budget 2022 will settle the dust on these issues. Moreover, there are many transaction specific issues which should also be clarified through FAQs.

READ I Global minimum tax: No clarity on revenue impact

Significant economic presence

SEP provisions were introduced in 2018 to address thrown up by the digitalisation of the economy. The definition of SEP was amended in 2020. The second limb of the amended definition, covering systematic and continuous soliciting of business activities or engaging in interaction with users in India, does not include the words “through digital means” unlike the erstwhile definition. This could cover all the modes, i.e., physical as well as digital, within the purview of SEP provisions which does not seem to be the intent of the legislature.

Secondly, considering the broad coverage of the concepts of SEP and EQL, there is an evident overlap of the services covered under both regimes. A plain reading of the provisions under both the regimes may likely give rise to double taxation, wherein on one hand EQL will be charged on the entire consideration received by the foreign entity, on the other tax will be levied under the Income-tax Act, 1961 in case such entity constitutes SEP. There could also be withholding of tax impact by way of treating the sums received by non-residents as royalty, FTS, etc.

The above are only macro level issues relating to non-resident taxation and there are many other expectations from Budget 2022. Let us see whether the upcoming Budget meets the expectations of the taxpayers.

(Lakshit Desai is director with Deloitte Haskins & Sells LLP.)