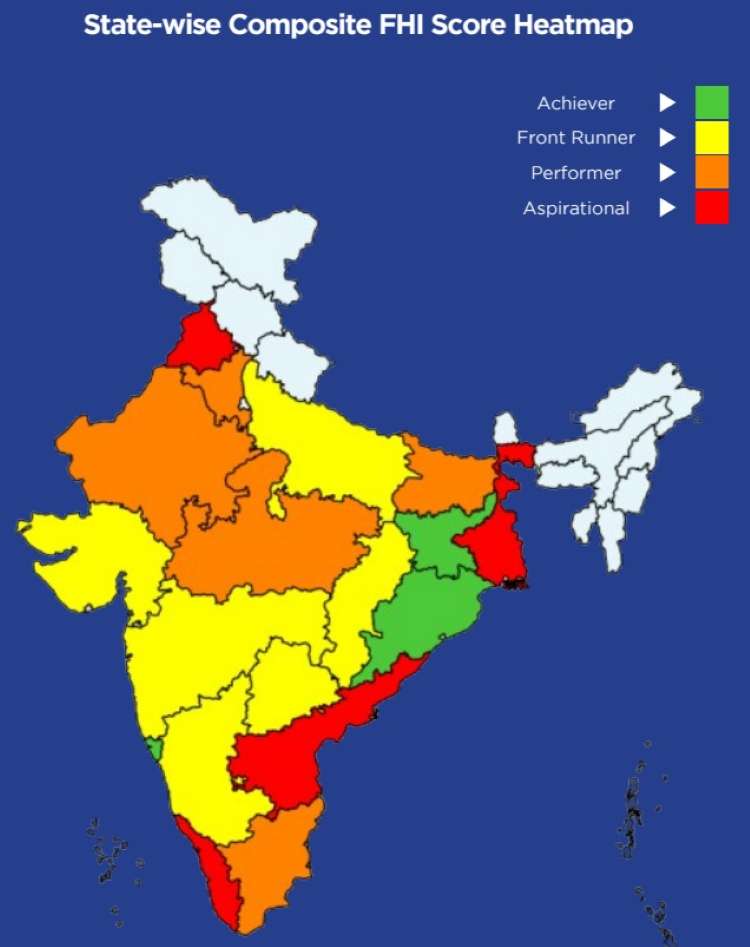

The Fiscal Health Index 2026 released by NITI Aayog, aspires to do what any modern policy instrument should: standardise measurement, enable comparison and guide reform. It is analytically sound in design. It expands coverage, refines indicators, and separates structurally distinct states. Yet, the Fiscal Health Index ranking risks being read in ways that distort reality. When fiscally fragile states in the North and Northeast populate the top tier within their categories, the index begins to say less about fiscal strength and more about the limits of benchmarking itself.

The core difficulty lies in treating fiscal metrics as comparable across states with vastly different economic bases. The inclusion of Northeastern and Himalayan states, even with separate ranking, exposes this asymmetry. These states operate under a distinct fiscal compact. Their revenue dependence on central transfers is high, their own tax bases are narrow, and their expenditure obligations are shaped by geography and security considerations.

A state that runs a modest deficit because its expenditure is largely grant-financed can appear fiscally prudent. Another that borrows more aggressively to fund infrastructure or social spending may rank lower despite stronger underlying capacity. The index measures outcomes. It does not fully capture the fiscal architecture that produces those outcomes.

READ I Economic reforms: Finance ministry flags risks of chasing short-term growth

Fiscal health index anomalies

The Comptroller and Auditor General’s decadal analysis complicates the picture further. State debt has risen sharply—from ₹17.57 lakh crore in 2013-14 to ₹59.60 lakh crore in 2022-23. Debt-to-GSDP ratios have climbed beyond the thresholds recommended by the NK Singh Committee in several states. Eight states now carry debt exceeding 30% of GSDP.

More telling is the composition of borrowing. Eleven states have used debt to finance revenue expenditure rather than capital formation. This violates the basic fiscal principle that borrowing should create assets. A state that keeps deficits in check by compressing capital spending may score well on an index. But it weakens long-term growth.

The Fiscal Health Index captures fiscal balance. It does not sufficiently penalise the erosion of fiscal quality.

READ I Rupee depreciation: Why RBI cannot reverse the fall

When low debt signals low capacity

In several Northeastern states, relatively low debt ratios coexist with weak economic capacity. This is not fiscal strength. It is fiscal constraint. Limited access to markets, narrow tax bases, and heavy reliance on central transfers reduce the scope for borrowing.

By contrast, states like Tamil Nadu or Karnataka carry higher debt but also generate stronger own-tax revenues and sustain higher levels of capital expenditure. They invest in infrastructure, health, and education, which in turn expand their economic base. A snapshot comparison obscures this dynamic.

The risk is that policymakers misread prudence as strength and restraint as discipline.

READ I IIP growth slows despite record factory output

The missing link: Fiscal outcomes

The most serious limitation of the index is its weak linkage to outcomes. Fiscal health is not an end in itself. It is a means to deliver public goods, reduce poverty, and enable growth.

Kerala offers a useful counterpoint. It combines relatively high debt with strong social outcomes. Its multidimensional poverty rate is among the lowest in India. Its investments in health, education, and social protection have produced measurable gains in human development. The state has demonstrated that fiscal stress, when managed, need not preclude welfare outcomes.

Conversely, several northern states with lower fiscal capacity continue to struggle with high poverty rates, weak human development indicators, and limited service delivery. Fiscal metrics alone do not explain this divergence.

Revenue capacity and federal imbalance

The Reserve Bank of India’s data reinforces the structural divide. Southern states dominate per capita income rankings and generate stronger own-tax revenues. Bihar and Uttar Pradesh, despite large economies in absolute terms, lag significantly in per capita income and fiscal capacity.

This divergence has implications for fiscal rankings. States with stronger economic bases can sustain higher deficits and still remain fiscally credible. States with weaker bases appear disciplined because they lack the capacity to spend.

The Fiscal Health Index does not fully integrate this dimension of fiscal federalism. It treats states as comparable units. They are not.

Off-budget liabilities and hidden stress

Another blind spot is off-budget borrowing. The CAG has repeatedly flagged the growing use of public sector entities and special purpose vehicles to raise debt outside state budgets. These liabilities do not always feature in headline fiscal indicators.

A state can appear fiscally sound while accumulating contingent liabilities that will surface later. Without a comprehensive accounting of such exposures, any ranking of fiscal health remains incomplete.

What the index should measure

The value of the Fiscal Health Index lies in its ability to standardise data and highlight fiscal risks. But its interpretation requires caution. A more meaningful assessment would incorporate three additional layers.

First, the quality of expenditure. Capital formation must be distinguished from consumption spending. Second, the sustainability of debt, including off-budget liabilities. Third, the linkage between fiscal choices and development outcomes.

Without these, the index risks becoming a league table of numbers rather than a guide to policy.

A caution against misplaced conclusions

There is a deeper concern. Fiscal Health Index rankings influence policy behaviour. States may seek to improve their position by compressing spending or deferring investment. This would be a misreading of fiscal discipline.

Fiscal health is not about low deficits or low debt alone. It is about the ability to borrow responsibly, invest productively, and deliver outcomes. A state that avoids borrowing to maintain a favourable ranking may be undermining its own growth.

The Fiscal Health Index provides a useful starting point. It is not a definitive measure of fiscal strength. When states with fragile economic foundations appear near the top, it is a reminder that numbers require context. Without it, the index may obscure more than it reveals.