STT hike in Budget 2026: The Finance Bill, 2026 proposes higher Securities Transaction Tax (STT) rates on selected derivatives transactions by amending Section 98 of the Finance (No. 2) Act, 2004. The percentage increases appear modest. Their implications are not.

STT is a transaction-based levy collected at source on trades executed on recognised stock exchanges. Introduced in 2004, it was designed as a low-friction instrument to tax capital market activity while minimising evasion. The proposed changes leave equity cash trades untouched and focus squarely on futures and options, a segment that has expanded rapidly in both volumes and retail participation.

READ | Budget 2026 counts gig workers, but stops short of protection

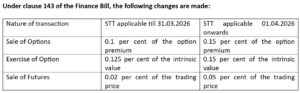

Budget 2026 raises STT on three derivatives

The government has framed the increase as both a revenue measure and a corrective intervention. The latter objective is more significant. Recent regulatory studies have shown that a large majority of retail participants in the derivatives market, particularly in options, incur net losses over time. Trading gains are heavily concentrated among a small minority, while frequent, small-ticket traders bear disproportionate losses. The design of the STT hike reflects this diagnosis.

The government has framed the increase as both a revenue measure and a corrective intervention. The latter objective is more significant. Recent regulatory studies have shown that a large majority of retail participants in the derivatives market, particularly in options, incur net losses over time. Trading gains are heavily concentrated among a small minority, while frequent, small-ticket traders bear disproportionate losses. The design of the STT hike reflects this diagnosis.

READ | Budget 2026: Export facilitation and MSME liquidity take centre stage

Options trading now dominates India’s derivatives market, accounting for the bulk of turnover and retail participation. Futures trading, by contrast, remains relatively more institutional and hedging-oriented. By raising STT more sharply on option premiums and exercises, the policy targets the segment where speculative retail activity is most intense, rather than treating the futures-and-options market as a single undifferentiated block.

The STT increase also needs to be read alongside a series of earlier measures introduced over the past two years. Contract lot sizes in derivatives have been raised. Option buyers are required to pay premiums upfront. Margin requirements on expiry-day short positions have been tightened. Market intermediaries and regulators have stepped up action against unregistered trading advisers and social media influencers offering stock tips. Investor grievance redressal systems have been strengthened, supported by sustained awareness campaigns.

Individually, none of these steps would materially alter trading behaviour. Taken together, they signal a deliberate attempt to introduce friction into a segment that had become unusually accessible to inexperienced participants.

Markets responded nervously on Budget Day. The Sensex and Nifty fell, and India VIX rose by 10.7 per cent, indicating a sharp increase in perceived risk. Such reactions are not uncommon on Budget days and often reflect rapid unwinding of leveraged or derivatives-heavy positions rather than a considered verdict on policy. There is little evidence so far of a persistent impact on broader equity sentiment.

For long-term equity investors, the STT revision is largely neutral. The incidence falls most heavily on frequent traders, particularly in options strategies that rely on high turnover and thin margins. High-frequency traders, institutional arbitrageurs, and funds exploiting price differentials between cash and derivatives markets will see transaction costs rise, potentially compressing returns.

READ | Budget 2026 treats MSMEs as infrastructure, not beneficiaries

This raises a legitimate concern. Derivatives markets are not merely speculative arenas; they also facilitate hedging, risk transfer, and price discovery. Higher transaction taxes can reduce liquidity, widen bid–ask spreads, and impair market efficiency, especially during periods of stress. These trade-offs are real, even if they are not the primary focus of the current policy stance.

The revenue dimension of the STT hike, while secondary, is not trivial. Derivatives account for a significant share of capital market turnover, and even small increases in transaction taxes can yield meaningful collections. At the same time, STT remains a relatively small component of overall tax revenues, reinforcing the view that behavioural correction, rather than fiscal consolidation, is the dominant objective.

There is also the risk of activity migrating to offshore or less regulated venues if onshore costs rise too sharply. The government appears willing to accept this risk in the near term, prioritising retail investor protection over marginal gains in market volumes.

The broader message is unambiguous; the government no longer views rapid growth in derivatives trading as an unqualified positive. Expansion will be tolerated only alongside higher friction and tighter guardrails. Once again, STT has been deployed as a blunt but administratively efficient instrument to deliver that signal.

Leena Chhabra is Assistant Professor of Finance at University of Delhi.