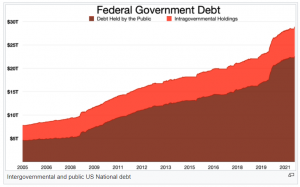

Public debt has risen to unprecedented levels because of the Covid-19 pandemic. Public debt is criticised for its impact on economic growth and the burden it puts on future generations. The view of public debt has been changing in response to events. In the 1980s and 1990s, there was a growing concern about governments. The general view was that public debt in the US was on a dangerously unsustainable path. The Committee for Responsible Federal Budget was established in 1981 in response to this concern. Then came the global financial crisis, and there was a temporary rethink on the role of public debt in the US.

The American Recovery and Reinvestment Act of 2009 piloted by the Obama administration rolled out a $787 billion stimulus package that pushed US public debt from 64% of the GDP to 84%. Similarly, large deficits and the rising debt-to-GDP ratio forced European countries to recapitalise their banking systems. Some countries like Ireland saw even larger increases in debt-to-GDP ratio, but that deviation from the normal was temporary. Once recovery set in, the governments turned back to austerity and the events of 2008 and 2009 were dismissed as temporary.

READ I Timely action on inflation needed to avert hard landing, says Maurice Obstfeld

Covid forces deviation from fiscal orthodoxy

The next deviation from fiscal orthodoxy happened during the Covid-19 pandemic. We saw governments around the world running large deficits and accumulating unprecedented levels of debt. The US federal deficit was 15% of the GDP in 2020, and 12.4% in 2021. The public debt was more than 100% of the US GDP, as in the case of most of the developed world. Germany abandoned its balanced budget rule and ran up a deficit higher than 4% of the GDP. Instead of chastising national governments for excessive debt and deficits, the European Commission was warning them not to prematurely cut public spending.

Is this change in attitude and practices justified? And how long will it persist? I would argue that the change is justified in extraordinary circumstances like a global pandemic. A government that does not respond to this kind of emergency by mobilising all available resources will lose its legitimacy. Under normal circumstances, the government should live within its means in the same way a responsible household would balance its budget. But these are not normal circumstances. A government that doesn’t borrow to provide essential services during a pandemic would be accused of dereliction.

History reminds us that states and rulers have long borrowed to meet emergencies. Governments borrow heavily to mount a national defence which is seen as legitimate by the public. If you follow the recent literature on public debt, you know about ‘r-g’ where ‘r’ is the real interest rate and ‘g’ is the real growth rate of the economy. It is important to understand the behaviour of r minus g from the 19th century into the 20th century.

The point is that modern public finance and modern levels of public debt are in a sense corollaries of modern economic growth. There has to be a market for public debt and an adequate population of individuals with savings to invest. So it’s not a coincidence that the political jurisdictions that pioneered the issuance of public debt are the commercial centres of early modern and modern Europe.

READ I Philosophy of economics, policy science and ideology

History of public debt

Venice, Genoa, the Netherlands and Britain were all naval and commercial powers. Same is the case of the French towns that pioneered the placement of municipal and sovereign debt. There were financial preconditions for being able to issue public debt. Successful debt issuers have to create secondary markets where the securities can be bought and sold so that the investors could limit their risks and meet their liquidity needs.

So, government debt came to be seen as increasingly safe and became increasingly liquid. Public debt securities are accepted as collateral for other borrowing and lending transactions. The growth of the sovereign debt market eventually resulted in the creation of a private debt market. Over time, the uses of public debt have evolved, but financing wars remains of premier importance. One can see that public debt issuance in the US is punctuated by wars.

In the 19th century, governments started borrowing to invest in infrastructure. Investing in roads, railways, ports and urban lighting are associated with modern economic growth. In the late 19th century and early 20th century, governments began borrowing to finance social programmes and transfer payments. It makes sense to borrow toemergency invest in productive infrastructure which takes time to build and accrues returns over time. As the returns accrue, they can be used to finance the debt. It makes less sense to borrow for financing social programmes and transfer payments which are not always productive.

In a fragmented polity, political groups will have just enough power to defend their preferred social programmes, but not enough to force spending cuts on the preferred programmes of others. When political polarisation is combined with electoral uncertainty, politicians will advocate for higher spending on their favourite programmes. Revenue constraints will not deter them as they know that they will be in a weaker position to push for such spending when out of office. As a result, public debt will shoot up. That’s how public debt became a bad thing in the US from the 1980s. Leaders did what they did and public debt in the US remained uncomfortably high.

Covid created war-like emergency

Then came the Covid-19 pandemic. Everyone realised that this public health emergency was a crisis is a war-like situation. And it elicited a war-like fiscal response. Will this see a change in attitudes and actions that will persist in the fiscal landscape? The change in fiscal behaviour in the US, India, and elsewhere is simply the product of Covid-19. The nations will return to a more austere fiscal policy and attempt to reduce higher debt levels after the pandemic. But in advanced countries, the change in attitudes predates Covid-19 in some sense. Many of us were worried about turning back prematurely toward austerity after the global financial crisis and dooming ourselves to a slow recovery.

Thomas Piketty argued that a more expansive state is needed to address the rising inequality across the world. This predates Covid-19. Raghuram Rajan also talked about the fault lines and the need to address them before the pandemic. There was growing recognition of the need for the government to provide public goods such as education, healthcare, transportation, infrastructure and climate action, as markets don’t adequately provide these if left to their own devices. There was a recognition among American historians of the need to do that more expansively. Are we now swinging back to a new deal? In addition, low interest rates make heavier public debt sustainable.

The United States federal government spent just 2% of the GDP to service debt in 2020. This share remained almost unchanged since 2001. Public debt has gone up enormously since the 1990s, but interest payments have come down drastically. The same is true for Europe. So, one can argue that the Maastricht treaty, which limits the debt-to-GDP ratio to 60%, is outdated. The question now is whether these low interest rates will persist. The answer will depend on what you think is the reason why current interest rates are low.

Are they low because of a global savings glut and high savings rates in Germany, Saudi Arabia and emerging markets like China? Or is it because life expectancy in advanced economies has risen? When people live more and look forward to more years of retirement, they tend to save more. Is this because of the shift from manufacturing to services and from factories to digital platforms as Mr Summers believes? Or is it because of the growing inequality and the disproportionately high savings rates of the wealthy?

If interest rates go up, the debt arithmetic will become problematic. The change in the debt to GDP ratio over time depends on the government’s budget surpluses, especially the primary surplus that excludes interest payments. In such a scenario, governments will face some hard choices. Historically they have made the hard choice of running primary budget surpluses while bringing down public debt. There are three historical cases before World War I.

he United Kingdom brought down its Napoleonic war debt from nearly 200% of GDP to only 28% over the course of a century, the United States brought down its civil war debt of 30% of the GDP to essentially nothing on the eve of World War I and France reduced Franco-Prussian war debt of 100% of the GDP to barely half that level by the time of WWI.

How did they achieve these feats? In the case of the UK, there was a Victorian belief in sound finance so that the government could borrow again in future conflicts and a working class that preferred inflation over deflation. In the US, there was strong creditor influence in the Congress and the Southern states were opposed to expansive federal spending. France preferred fiscal restraint for building up the capacity to borrow again in future wars.

Look at some less happy cases like Germany after WWI where the public debt as a share of GDP was liquidated through hyperinflation. This is clearly not something anyone would want to repeat. After World War II, advanced economies brought down debt-GDP ratios of around 100% to barely a quarter of that by 1975. So, those who say that these heavy debts were brought down through financial repression, keeping interest rates low, regulation and a relatively rapid economic growth in the 30 years after WWII.

There was, again, a lot of fiscal effort involved. Primary budget surpluses were run by many advanced economies for extended periods to bring down these heavy debts. That brings us to the question of whether the nations can deal with the debt load by running persistent primary surpluses.

Since 1970, there have only been only three cases of countries that managed to run primary budget surpluses as large as 5% of the GDP for 10 consecutive years. The three cases are Norway after 1999, Belgium after 1995 and Singapore after 1990. What do these countries have in common? Norway discovered massive amounts of oil and natural gas in the North Sea and was able to sock away much of that in its sovereign wealth fund for future generations, but had the highest debt to GDP ratio in Europe and wanted to qualify for monetary union to adopt the Euro in 1999, so it had to convince its partners that it was a reliable Euro-area country.

Singapore had a strong technocratic government worried about its geopolitical exposure. The government could mandate primary surpluses and move revenues again into sovereign wealth funds. All countries can’t do this. Investors may shift to short maturity debt if they see inflation coming. There would have to be a series of inflationary surprises for this to happen. However, I doubt that our central banks will be prepared to sacrifice their hard-earned credibility by doing so. I think stability culture is now deeply ingrained in the central banking community. Hence, we will get 2-4% inflation for a period of time, but not the kind that would be needed in order to inflate away the inherited debt burden.

Can it be done through faster economic growth? That’s what Europe is trying to do through its recovery fund. There are people who hope that the coming digital revolution will translate into faster economic growth in the US and worldwide. However, history suggests that it will take time for faster economic and productivity growth to happen. This was the impetus for developing the interstate highway system in the United States.

The productivity benefits of this materialised only in the 1960s and 1970s after the highway system was completed in the 1950s. The point is that it takes time for general-purpose technologies to translate into faster economic growth. All this suggests that there are no simple solutions to ease the debt burden without major economic, financial and political dislocations.

(Barry Eichengreen is an American economist. Currently, he is George C. Pardee and Helen N. Pardee Professor of Economics and Political Science at the University of California, Berkeley.)