For nearly 30 years, global value chains defined the operating logic of globalisation. Production fragmented across borders. Firms optimised costs. Trade expanded through tightly interlinked supply networks. Consumers benefited from scale and price competition. The Global Value Chain Development Report 2025 confirms that this model is under strain—but not in retreat. Instead of deglobalisation, the world is witnessing a recalibration. Cost efficiency is no longer the sole organising principle. Resilience, sustainability, regional proximity, and strategic competition now shape how value chains function.

The report is clear on one point: repeated shocks—from the Covid-19 pandemic and geopolitical conflict to climate mandates and industrial policy activism—have disrupted GVCs. Yet these pressures have forced reorganisation rather than collapse. The result is a more complex form of global integration, where firms trade speed for security and cost for control.

READ I Global economy’s 2026 optimism masks deep fault lines

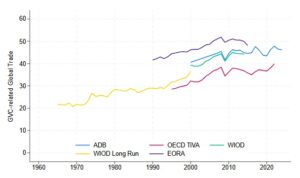

GVC trade remains dominant

GVC-linked trade continues to account for the bulk of global commerce, even as its share has declined. According to the report, GVC-related trade fell from 76% of global trade in 2010 to 63.6% in 2025, reflecting slower cross-border fragmentation rather than disengagement. Economies with deep historical integration- Europe, East Asia, and North America—continue to dominate production networks.

Firms have adapted to successive shocks by diversifying suppliers, adding production stages, and rerouting trade flows. Since the early 2020s, production processes have lengthened rather than shortened in many regions. Geopolitical risks and logistics disruptions have encouraged firms to add buffers, particularly across Europe and Central & West Asia, and to rely on alternative corridors rather than single routes.

This adaptive behaviour underlines a central argument of the report: GVCs are becoming more redundant by design, not less global by default.

READ I GDP growth: India tops global charts, but faces tariff risks

Services anchor global production networks

One of the report’s most consequential findings is the rising centrality of services in global manufacturing. Services now account for nearly one-third of the value added in manufacturing exports, reflecting deeper integration of logistics, finance, IT, design, and business services into production.

Since 2019, services have overtaken goods in GVC participation.

Digital services—telecommunications, software, finance, and professional services—proved far more resilient than goods trade during the pandemic and its aftermath. This shift marks a structural transformation: competitiveness increasingly depends on data flows, regulatory alignment, and digital infrastructure rather than physical scale alone.

For developing economies, this trend lowers some traditional entry barriers but raises new ones. Digital connectivity, regulatory certainty, and service-sector capabilities now matter as much as industrial capacity.

READ I India-US ties: Partnership under pressure

SMEs, intangibles, and the productivity divide

The report flags a persistent weakness in global value chains: small and medium enterprises remain trapped in low-productivity equilibria. Limited access to finance, weak broadband infrastructure, and inadequate digital skills prevent SMEs from upgrading within GVCs.

Productivity gains, the report argues, hinge on three enablers: reliable digital infrastructure, affordable finance, and targeted skill development. Intangible capital—data, software, organisational know-how, and intellectual property—has become a decisive source of comparative advantage. Firms with higher ratios of intangible to tangible assets demonstrate greater resilience and faster reconfiguration when shocks occur.

This “servicification” of GVCs has also reinforced regionalisation. Governments and firms increasingly favour intraregional trade to reduce exposure to geopolitical disruptions. Europe, North America, and parts of Asia have all seen faster growth in regional trade than in cross-regional flows.

Readiness matters more than location

To assess which countries are positioned to benefit from the GVC reset, the report introduces a Global Value Chain Readiness Index, covering six pillars: trade and investment regimes, technology and connectivity, sustainability and energy systems, financial and business readiness, institutional quality, and geopolitical alignment.

The results are sobering for many developing economies. Even countries with favourable demographics, renewable energy potential, or critical mineral reserves fall short on logistics reliability, digital infrastructure, financial depth, and institutional capacity. Nearshoring and friend-shoring strategies deliver gains only when backed by domestic reforms.

Future GVC participation will demand higher standards—on sustainability, reliability, traceability, and coordination—raising the cost of entry for laggards.

Technology, EVs, and the green constraint

The global electric vehicle (EV) industry illustrates how technological and environmental transitions are reshaping value chains. China now accounts for around 77% of global EV production, overtaking traditional automotive leaders such as Germany, the United States, and Japan. The report notes that technological discontinuities can still create latecomer advantages—if countries align industrial policy with technology adoption.

Environmental sustainability is no longer peripheral. Carbon pricing, emissions trading, and trade-related climate measures are becoming embedded in GVC governance. Expanding carbon pricing to cover smaller firms can improve emissions efficiency, but only if accompanied by access to green technology and finance.

The The Global Value Chain Development Report 2025 calls for policies that support green R&D, accelerate low-emission technologies, and reform intellectual property regimes to widen diffusion. Without international coordination, climate-linked trade measures risk deepening global divides.

Industrial policy, finance, and integration

Another defining feature of the current phase is the resurgence of industrial policy. Unlike earlier eras, today’s interventions are embedded in fiscal, financial, and climate frameworks. Tax credits, targeted lending, subsidies, green finance, and public procurement are increasingly coordinated at the macro level.

These policies promote resilience but also intensify geoeconomic fragmentation. Firms navigate tariffs, sanctions, and subsidies by routing investment through connector economies such as Mexico, Vietnam, Turkey, and ASEAN members. While WTO subsidy rules remain in force, weak enforcement and notification gaps limit their disciplining role.

Finance emerges as a binding constraint. Foreign direct investment remains critical for technology transfer and organisational learning. Trade and supply-chain finance determines whether firms can operate within complex networks. High costs and limited coverage of trade finance disproportionately exclude SMEs and emerging markets from GVC participation.

A more demanding phase of globalisation

The Global Value Chain Development Report’s central conclusion is unambiguous: globalisation is not disintegrating, but it is becoming more demanding. Integration today requires capabilities rather than cost arbitrage. Firms and countries must invest in digital infrastructure, financial systems, skills, and regulatory credibility.

For policymakers, the task is to ensure that this new phase remains inclusive, resilient, and sustainable. That means widening access to finance and technology for smaller firms, improving logistics and digital trade frameworks, and aligning industrial and climate policies. Without such coordination, rewired value chains risk reinforcing existing divides rather than generating shared growth.

The era of hyper-globalisation may be over. What replaces it will reward preparedness, not proximity alone.

Dr Rajeev Verma is Assistant professor (Economics), University of Delhi.