India’s economy is walking a fine line. Headline inflation has eased to multi-year lows, giving relief to households and policymakers. Yet, uneven demand recovery and sectoral deflation raise doubts about whether stability is coming at the expense of growth. With the Consumer Price Index (CPI) now close to the lower bound of the Reserve Bank of India’s (RBI) 2–6% target band, the task is no longer just containing inflation but balancing stability with momentum.

A premature policy loosening could rekindle price pressures, while prolonged caution risks stifling investment and consumption at a time of global headwinds. The situation demands not only monetary fine-tuning but also coordinated fiscal support to sustain growth without undermining the credibility of India’s inflation-targeting regime.

READ I GST reforms and FDI surge power recovery

Retail and wholesale inflation

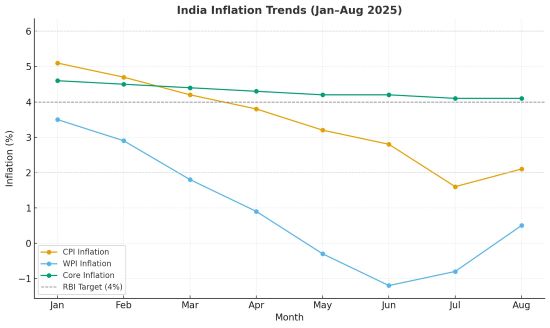

Annual retail inflation in August 2025 stood at 2.07%, up from a revised 1.61% in July. Food inflation remained in negative territory at –0.69%, though less steep than July’s –1.76%. Core inflation, which excludes food and fuel, was steady at 4.1%. On the wholesale side, the Wholesale Price Index (WPI) edged back into positive territory with a 0.52% year-on-year increase after months of deflation, driven by food and manufactured goods. Urban inflation (2.47%) was higher than rural inflation (1.69%), reflecting stronger non-agricultural demand. Provisional data show that food inflation, while still negative across both rural and urban areas, is inching towards convergence.

Food inflation is the most volatile component. The current negative readings are driven by base effects, falling prices of cereals and vegetables, and favourable supply conditions. But erratic rainfall in Punjab, Telangana, and Haryana threatens yields of kharif crops such as pulses, rice, and coarse cereals. This could reverse the trend, pushing food prices up later in the year. Fuel and energy inflation remain muted for now, but global oil market volatility leaves room for upside risk.

Global inflation trends

Globally, inflation has eased from the highs of 2022, when supply chain disruptions and energy shocks pushed consumer prices to record levels across advanced and emerging economies. The US Federal Reserve’s aggressive tightening cycle has helped bring American inflation closer to its 2% target, though housing and services costs remain elevated. In the eurozone, disinflation has been faster, with falling energy prices and weak demand pulling headline inflation below 2.5%, but core inflation remains sticky. China, by contrast, is flirting with deflation, reflecting weak domestic demand and property market distress.

Across emerging markets, food and fuel prices remain the biggest swing factors, as climate shocks and geopolitical disruptions to shipping lanes have kept commodity markets volatile. For India, these global crosscurrents—softening demand in the West, potential supply shocks in energy, and China’s slowdown—frame the external backdrop against which domestic price management must be calibrated.

Core inflation near 4.1% underscores that underlying demand is intact. Services, housing, utilities, and healthcare costs remain sticky. Urban housing inflation has stayed above 3%, while health and education indices show little sign of easing. These pockets of persistence matter because inflation expectations can shift. If households and firms come to expect higher prices, it could influence wages and business pricing, complicating RBI’s efforts to keep inflation anchored.

Policy response: Balancing risks

The RBI targets CPI inflation at 4% with a 2–6% tolerance band. With headline inflation near the floor, the central bank has cut the repo rate by 100 basis points since February 2025. But further easing has to be cautious. Over-aggressive cuts could reignite price pressures, particularly in essentials.

Fiscal policy must complement monetary moves by strengthening food supply chains, managing subsidies, calibrating minimum support prices (MSPs), and improving procurement and storage to soften shocks. Urban demand pressures suggest targeted interventions in housing, utilities, and services could also be warranted.

India’s inflation picture today is one of cautious optimism. Headline inflation is well below the peaks of 2022–23, food prices are subdued, and wholesale inflation is positive again—though modestly. Yet vulnerabilities remain: weather-linked supply risks, sticky core inflation, and fragile expectations. A durable framework requires dual-track policy: preserving monetary credibility while deploying fiscal and supply-side tools to buffer shocks. Investments in agriculture logistics, forecasting systems, storage infrastructure, and rationalisation of input costs are essential.

The challenge is not just keeping inflation low but keeping it anchored. India’s policymakers must ensure that stability is durable and compatible with growth. For an emerging economy that seeks both robust expansion and price discipline, that remains the sweet spot.

Naman Mishra is a doctoral student at Bennett University, Greater Noida. Aneesh KA is Assistant Professor of Economics at the Delhi NCR Campus of CHRIST University.