The Union Budget 2026-27 has brought a familiar ghost back to North Block: the fiscal deficit. The headline number, 4.3% of GDP for the coming year against a revised 4.4% the year before, suggests steady consolidation. But that tells only part of the story. The more important question is not how much the government borrows, but what it borrows for.

For years, India’s fiscal record was defined by borrowing for consumption. The government borrowed to pay interest on past debt and to finance subsidies and routine expenditure. The revenue deficit captured that weakness. It reflected borrowing for day-to-day spending rather than for creating assets.

READ I Indian economy needs a hard oil shield

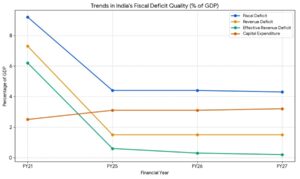

India’s fiscal deficit quality

That pattern is now changing. Budget 2026-27 projects the revenue deficit at 1.5% of GDP, the lowest in nearly two decades. Effective revenue deficit, after adjusting for grants that create capital assets, is projected at 0.3%. That is close to a fiscal golden rule: borrow mainly to build, not to consume.

This is the real shift in India’s public finances. A fiscal deficit used to create infrastructure is not the same as one used to fund current expenditure. The distinction matters for growth, debt sustainability and investor confidence.

READ I Rupee depreciation is India’s oil warning

Capital expenditure drives fiscal multiplier

The clearest expression of that shift is capital expenditure. The Budget sets capex at ₹12.22 lakh crore in FY27, or about 4.4% of GDP. That is a sharp rise from 1.7% in FY19. Public spending has moved decisively towards roads, railways, logistics and energy infrastructure.

This is not an accounting detail. Capital spending has a higher multiplier than routine revenue spending. A highway, rail corridor or transmission line raises productivity long after the budget year ends. A subsidy may ease immediate distress, but it rarely expands the economy’s productive capacity. The government is therefore betting that public investment will crowd in private investment, which has remained weak for too long. The logic is straightforward: if the state improves power, transport and logistics, private firms may finally invest with greater confidence.

That improvement in expenditure quality has also helped India’s macro standing. A 4.3% deficit used to build productive assets is more defensible than a lower deficit used to finance giveaways. Markets and ratings agencies understand that distinction.

READ I RBI dividend windfall cannot replace fiscal reform

Interest payments still squeeze fiscal space

But past excesses still cast a long shadow. Interest payments in FY27 are expected to exceed ₹14 lakh crore. That absorbs nearly 26% of total expenditure and around 40% of revenue receipts. This is the cost of old borrowing, and it sharply limits current choices.

When four out of every ten rupees of revenue go to servicing debt, fiscal space narrows. That leaves less room for health, education and social protection. Public expenditure on health still remains below the National Health Policy target of 2.5% of GDP. This is why the shift in fiscal focus from annual deficit numbers to the debt-to-GDP ratio makes sense.

Debt-to-GDP target and nominal growth risk

The Centre now aims to bring debt down to 50% of GDP by FY31 from around 56% now. That signals a more serious concern with long-term solvency rather than annual optics. But debt ratios do not fall by intent alone. They need growth.

That is where the arithmetic becomes less comfortable. Reaching the 50% target requires nominal GDP growth of around 10.5-11%. With nominal growth cooling to about 8-9% in early 2026 as inflation eases, the denominator effect is weaker. In such a setting, debt reduction becomes harder even if fiscal discipline holds.

State finances and federal fiscal deficit

The Centre’s numbers are only part of the picture. State finances are becoming more uneven. The 16th Finance Commission enters this debate at a time of sharper federal friction. Some states continue to invest in infrastructure. Others lean more heavily on cash transfers and subsidies.

The Centre’s Special Assistance to States for Capital Investment has helped keep state capex near 2.4% of GDP. But the larger issue remains unresolved. The FRBM framework imposes a uniform 3% fiscal deficit ceiling on states. Critics are right to ask whether that is too blunt an instrument. Borrowing to build a university, hospital network or transport system is not the same as borrowing to pay for a free power scheme. The quality of the deficit matters as much in Chennai or Lucknow as it does in Delhi.

Bond markets may eventually enforce that distinction. States that choose consumption over asset creation may find themselves paying more to borrow. That would be a healthier form of fiscal discipline than a mechanical one-size-fits-all ceiling.

Capex momentum and the growth cliff risk

India is no longer seen through the old lens of fragility. The economy has moved beyond the twin balance sheet crisis and gained a degree of macro credibility. But credibility is never permanent. It has to be renewed.

The risk is clear enough. If public capex keeps rising but private investment does not respond, the government could end up carrying too much of the growth burden for too long. That would weaken the balance sheet without delivering the hoped-for handover to private enterprise.

The test, then, is not whether the fiscal deficit falls from 4.4% to 4.3%. It is whether each borrowed rupee creates future income, productivity and taxable growth. India needs a fiscal culture that judges borrowing by its use, not just by its volume. An independent fiscal council, as proposed earlier by the N.K. Singh committee, would help bring more transparency and discipline to that exercise.

As India looks towards becoming a $7 trillion economy, the fiscal debate must also grow up. Debt can support growth. But only when it finances assets that outlast the borrowing. Steel and concrete can justify debt. Consumption dressed up as policy cannot.

Dr PK Santhosh Kumar is Director, Centre for Budget Studies, Cochin University of Science and Technology.