The New CPI series: India’s most consequential inflation statistic has been reset. The government has shifted the Consumer Price Index to Base 2024, drawing the revised weights from the Household Consumption Expenditure Survey 2023-24. CPI is not just a monthly print. It frames RBI policy choices, budget assumptions, dearness allowance and pension indexation, wage negotiations, and—inevitably—public belief about whether life is getting costlier faster than incomes.

The case for rebasing is straightforward. A basket built off older consumption patterns cannot remain the economy’s primary price gauge indefinitely. But the success of this revision will not be decided by the methodological note. It will be decided by whether the new index is seen as both more representative and more believable.

READ I CPI overhaul could deepen gap between inflation data and reality

CPI basket update and consumption shifts

Household spending has moved since the earlier survey base. Urbanisation has accelerated, services have expanded faster than overall GDP, and a significant slice of consumption has migrated to digital channels. The new CPI series acknowledges this structurally: the weighted item basket rises to 358 from 299, with a larger services footprint, and the classification is mapped to COICOP 2018 to improve international comparability.

This is also a revision to how prices are collected. MoSPI’s new series expands the price-collection frame across rural and urban markets and adds designated online markets in large cities, with online prices collected at higher frequency for selected items. This matters because “new items” without credible collection design is cosmetic modernisation. The stated aim is to reduce the lag between how Indians spend and how India’s CPI measures.

READ I Indian economy: Inflation cools but investment lags

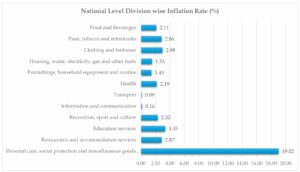

Food weight reduction and headline inflation volatility

The most visible shift in the new CPI series is the reduced weight for food and beverages—from 45.86% in the earlier series to 36.75% in CPI 2024. This reflects a declining food share in the consumption expenditure profile captured in HCES 2023-24, while food remains the single largest component.

A lower food weight will also change the short-term behaviour of headline inflation. India’s food prices are volatile. Vegetable spikes, cereal swings, and policy moves on exports and buffer stocks can push the monthly number around. A CPI less dominated by food will be less sensitive to transient spikes, giving policymakers a steadier signal when they need to distinguish episodic supply shocks from broader price pressure.

One point needs to be explicit because it will recur in public debate. CPI is designed to track out-of-pocket household expenditure; MoSPI’s documentation notes that free social transfers in kind are excluded by definition, following standard guidance. The food-weight change should therefore be read as a shift in cash expenditure patterns, not an imputed valuation of what households consume.

READ I India must move workers out of low-productivity work

Services inflation and digital prices

The new CPI series leans into what has changed in India’s inflation dynamics. In a more service-led economy, price pressure is shaped not only by agricultural cycles but also by rising costs in health, education, transport, communication, and financial services. The updated basket expands services coverage and incorporates prices from digital channels for selected segments.

Housing is a second, quieter, but important change. The CPI 2024 series expands rent measurement and explicitly extends coverage to rural housing, with 19,039 dwellings identified for rent collection (15,715 urban; 3,324 rural). This is a methodological upgrade with real-world consequence: housing inflation is a large and persistent driver of cost-of-living perceptions, and weak measurement here corrodes trust even when the rest of the index is sound.

RBI inflation targeting and fiscal indexation

Budget projections, inflation-linked expenditures, and welfare adjustments depend heavily on CPI prints. If the index is overly hostage to short-lived food spikes, fiscal planning can become noisy—especially where payouts are indexed mechanically. A more representative basket should reduce that volatility at the headline level, without removing food from view.

For the RBI, the advantage is more subtle. The new series should, over time, support clearer separation between temporary food shocks and structural inflation drivers—useful for communication as much as for decision-making. But this benefit is contingent on credibility. If the public concludes the index is smoothing inflation away, the RBI’s job becomes harder, not easier.

Lived inflation gap and credibility risk

Statistical accuracy does not automatically translate into perceived credibility. The sharp reduction in food weight raises a predictable concern: the gap between measured inflation and felt inflation may widen for rural and lower-income households that remain heavily food-centric. Even if the national consumption average shows a declining food share, the psychological and economic impact of rising vegetable, milk, or pulse prices remains far stronger for households operating on tight budgets.

This is not a technical footnote. CPI is also a political signal. It shapes arguments around cost of living, welfare adequacy, and income adjustments. If food prices are elevated while headline inflation appears subdued because weights have shifted, the statistical approach—and the policy response that follows—will face greater scrutiny.

New CPI series and revision cycle discipline

For researchers, investors, and policymakers to interpret trends, continuity is essential. A new CPI series without a properly constructed historical back-series forces users into ad-hoc linking, complicating long-run comparisons and weakening transparency. The burden should not be shifted to analysts who rely on official statistics precisely because they need standardisation.

The second trust lever is frequency. MoSPI’s own position is that base-year revisions for key indicators should move to a three-to-five-year cycle, aligning with survey availability and structural change. That commitment matters because it reduces the likelihood that CPI again drifts far from contemporary consumption.

None of this should distract policymakers from the underlying inflation problem. India’s inflation is experienced unevenly across regions and income groups. Better measurement helps diagnosis. It does not replace supply-side reforms in agriculture, storage, logistics, and food distribution—the recurring sources of India’s most visible inflation episodes.