RBI monetary policy: The monetary policy committee will announce its first resolution of FY27 on April 8, 2026. Over the past year, monetary policy has been expansionary, with the repo rate cut by 125 basis points from 6.50% to 5.25% between December 2024 and February 2026 to support growth. But the earlier tailwind of benign inflation has faded. This resolution comes amid the war in the Middle East and its spillovers: rising crude prices, capital outflows, and volatility in global financial markets.

Policy rate decisions also shape other macroeconomic variables, especially the rupee’s exchange rate against the US dollar. That makes the April resolution more consequential than a routine rate call.

READ | RBI MPC meeting faces growth-inflation trade-off

Rupee depreciation and exchange rate pressure

A bilateral exchange rate is the price of one currency in terms of another. It is determined in the foreign exchange market by demand and supply, and shaped by interest rates, inflation, trade balances, and market sentiment.

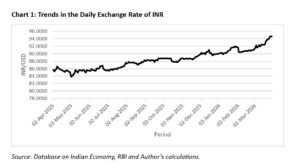

In nominal terms, the rupee has been on a persistent weakening trend against the US dollar. It breached the 95 mark on March 30, 2026, before recovering to 94.65 after RBI intervention in the forex market. It has been among the worst-performing Asian currencies, sliding by more than 10% in FY26.

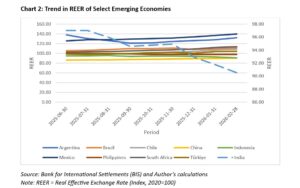

The weakness is not only nominal. It is visible in real terms as well. According to the RBI Bulletin of March 2026, the rupee’s real effective exchange rate for a 40-currency basket fell from 102.34 in February 2025 to 94.05 in February 2026. That points to undervaluation. A comparison with the REERs of other emerging economies shows the same pattern: the rupee has been steadily depreciating in real terms.

Exchange rate risks for imports, inflation and growth

A weaker rupee makes Indian goods and services cheaper relative to those of peer economies and can improve export competitiveness. But that advantage is limited in a world marked by wars, tariff threats, policy uncertainty, and weak trade demand. In such a setting, the gains from currency depreciation taper quickly.

READ | RBI misselling rules may reshape retail finance conduct

The costs are clearer. A weaker rupee makes imports more expensive. That is a serious risk for India, which imports more than 85% of its energy needs and remains heavily dependent on the Gulf. In the present context, a persistently undervalued currency is a burden, not a cushion. Estimates suggest that a 10-dollar rise in crude prices could shave 0.5 percentage points off India’s GDP growth.

The inflation risk is equally serious. Higher import costs raise fuel and transport prices and then spread across sectors. Imported inflation can also worsen the trade balance and current account.

Capital outflows and RBI policy constraints

External pressures are already visible in financial flows. In March 2026, investors pulled nearly $12 billion out of Indian equity markets, signalling a shift in sentiment. Such outflows put further pressure on the rupee and add to inflation risks.

BIS REER data also show that the rupee has remained undervalued, with volatility that is moderate but still higher than in several other emerging and developing economies. That matters because the exchange rate is a key channel of monetary transmission.

If the RBI continues with an expansionary stance in pursuit of growth, it risks further currency undervaluation. That can trigger beggar-thy-neighbour effects, where one country seeks export gains through currency weakness and its trading partners respond in kind. Such pressures are already visible among India’s competitors, including China, Indonesia, and the Philippines. In a fragile global trade environment, that would further erode India’s external position.

READ | RBI dividend windfall cannot replace fiscal reform

Easy money also weakens India’s ability to attract capital inflows by widening interest rate differentials with economies that are holding rates steady instead of cutting them further. An accommodative stance could also accelerate the drawdown of foreign exchange reserves, reducing the RBI’s room to intervene in the currency market when needed.

RBI monetary policy must put price stability first

The RBI and the MPC must now navigate a sharper trade-off between growth and stability. Accommodative policy may support demand, but it also carries clear risks: higher inflation, deeper external vulnerability, further rupee depreciation, volatile capital flows, and added pressure on debt sustainability.

In the current external environment, price stability must take precedence. Growth support, for now, should be treated as a secondary objective and left largely to the government.

Chinmay Joshi is a Research Associate at the Economics and Policy Area at Bhavan’s SP Jain Institute of Management and Research (SPJIMR), Mumbai and a Research Scholar at Gokhale Institute of Politics and Economics, Pune.