India’s textile exports: The proposed India-US trade arrangement remains important for India’s textile and clothing industry even as the tariff landscape has changed. For Indian exporters, the issue is no longer only whether headline tariffs come down. It is whether the eventual agreement preserves competitiveness against Bangladesh, Vietnam, Indonesia and other Asian suppliers in the American market.

On February 6, India and the United States outlined the framework for an interim trade agreement. That raised hopes in India’s textile and clothing sector, the country’s second-largest employer after agriculture. A reduction in U.S. import tariffs could improve India’s relative position against competing exporters. Yet tariff correction alone cannot settle the matter. Final export competitiveness depends on logistics, scale, productivity, delivery performance and compliance capability as much as on customs duties.

READ | India textile industry remains exposed to global shocks

Bangladesh tariff deal changes the equation

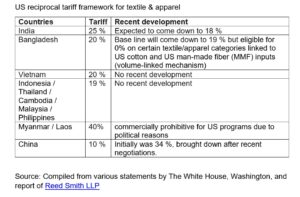

The regional equation changed when Bangladesh and the United States announced a reciprocal trade arrangement. Under that framework, Bangladeshi exports would face a general tariff of 19%, while a specified volume of textile and apparel exports could enter the United States at zero reciprocal duty if linked to the use of U.S.-origin textile inputs. That is not a simple tariff cut. It is a conditional, volume-linked sourcing incentive that can alter regional trade patterns.

For India’s garment exporters, the Bangladesh arrangement creates fresh pressure in the U.S. market. It can also affect Indian suppliers of yarn, fabric and fibre to Bangladesh if Dhaka shifts part of its sourcing toward U.S. inputs to qualify for preferential access. The stock market’s immediate reaction reflected that concern, with textile counters falling as investors priced in the possibility of short-term disruption.

Soon after, commerce minister Piyush Goyal said India could receive a similar facility once the bilateral arrangement is concluded. That assurance matters. But until terms are formalised, Indian exporters must operate in a market where a key competitor already has a more defined pathway to preferential access.

Tariffs matter, but they do not decide competitiveness alone

The debate in India has centred too narrowly on tariff differentials. That is understandable, but incomplete. Textile and apparel sourcing is no longer determined by customs duties alone. Buyers evaluate labour cost, productivity, power tariffs, shipping time, order flexibility, testing standards, compliance systems and the ability to scale without quality slippage.

US reciprocal tariff framework for textile & apparel

That is why even a modest tariff advantage does not automatically shift orders. A buyer sourcing basic garments may still favour Bangladesh because of lower wage costs and large-scale garmenting capacity. A buyer looking for diversified sourcing, shorter lead times, technical capability or a broader product mix may still find India attractive despite a smaller tariff edge.

India’s own export profile underlines this complexity. Its shipments to the United States are concentrated in knitted apparel, woven apparel and made-ups. In some of these segments, tariff competition with Bangladesh is close enough that operational capability becomes decisive. The real contest, therefore, is not between tariff lines alone. It is between production systems.

READ | US-Bangladesh deal narrows India’s US textile advantage

India’s value chain remains a structural advantage

India retains one enduring strength that Bangladesh cannot easily replicate: a deeper and broader domestic textile value chain. India has a more integrated ecosystem from fibre and spinning to fabric and garments. That gives manufacturers better control over cost, quality and delivery. It also reduces exposure to disruptions in imported raw material supply.

Bangladesh’s garment industry is formidable, but its backward linkage remains uneven. It has stronger capability in cotton spinning and knit fabric production, but woven and man-made fibre segments still depend more heavily on imported inputs. India has long been an important supplier to that system.

The new U.S.-Bangladesh framework attempts to reshape those sourcing patterns by linking zero-duty access to the use of U.S. cotton and man-made fibre inputs. But that shift has limits. U.S. cotton may offer efficiency gains, as industry participants often argue, yet it also brings longer shipping routes, higher freight bills, greater inventory costs and longer lead times. Those are not marginal considerations in a business where delivery schedules and working capital matter as much as raw material quality.

Non-tariff factors will shape the next phase

India’s challenge is not merely to secure equivalent tariff treatment. It is to convert tariff relief into commercial advantage. That requires improvement in areas where trade policy cannot substitute for industrial capability.

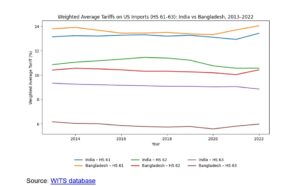

Tariff Comparison of India-Bangladesh in USA During 2013-22 for the product code 61, 62, 63

Bangladesh retains an advantage in labour-intensive, high-volume basic garments. India compensates in part through productivity in organised units, stronger technical supervision and greater product diversification. It also has policy support through production-linked incentives and integrated textile park development. But these advantages will matter only if they translate into faster execution, reliable quality and competitive cost structures.

For U.S. buyers, the attraction of South and Southeast Asian sourcing will remain intact because Washington cannot allow apparel inflation to rise sharply while also trying to reduce dependence on China. That gives India an opening. But it is an opening that must be earned through factory-level competitiveness, not assumed from tariff diplomacy alone.

READ | Textile industry’s problem is not labour, it’s policy and scale

India-US trade deal must protect market position

The eventual India-US agreement matters because it can prevent Indian exporters from slipping into a tariff disadvantage against regional competitors. It can also reduce uncertainty at a time when sourcing decisions are being recalibrated across Asia. But it should not be mistaken for a complete solution.

The textile and clothing sector does not need a narrative of relief. It needs a framework for competitiveness. Tariff parity with Bangladesh and other Asian exporters is necessary. It is not sufficient. India’s long-term position in the U.S. market will depend on whether it can combine trade access with lower logistics costs, faster turnaround, stronger compliance and a more responsive manufacturing base.

That is the real test before India’s textile industry. The bilateral trade arrangement can help preserve the level playing field. Only industrial performance can determine who wins on it.

Dr Amlan Ray is an economist with experience in T&C product development and exports. He is currently academic head at Sunstone Education Technology and advisor to Infinite Sum Modeling Inc, an economic modelling firm. Supratim Bandyopadhyay is an IIT Delhi alumnus with three decades of experience in textile production, quality assurance, and global sourcing across South and Southeast Asia. He is associated with US-headquartered Cintas in global apparel supply chains and based in Bangkok.