The liberalisation of India’s economy in the early 1990s—characterised by policies of liberalisation, privatisation, and globalisation—opened the skies to private airlines, ushering in a new era of growth in both domestic and international air travel. Today, India is the world’s third-largest domestic aviation market, behind only the United States and China. The post-pandemic rebound has been robust, with India overtaking Brazil and Indonesia in passenger traffic. However, despite the impressive recovery and rapid expansion, the aviation industry continues to face severe structural, financial, and operational headwinds that threaten its long-term viability.

Indian aviation industry’s ascent began in earnest when private carriers were permitted to compete with the state-owned Air India. The entry of low-cost carriers like IndiGo, SpiceJet, and Go First democratised air travel, bringing it within reach of India’s burgeoning middle class. By the early 2000s, passenger numbers had surged, driven by rising incomes, rapid urbanisation, and airport upgrades. But this expansion came with cracks.

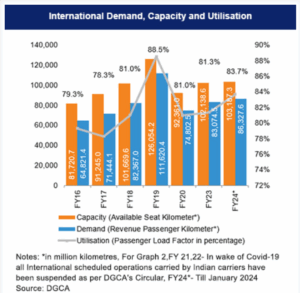

The 2019 collapse of Jet Airways, once India’s largest private airline, was a wake-up call. Strained by mounting debt, high fuel costs, and the global grounding of Boeing 737 Max jets, Jet’s bankruptcy revealed the fragility beneath the sector’s growth story. The COVID-19 pandemic deepened the crisis: capacity was slashed, employees furloughed, and fare caps imposed—upending revenue models across the board. Yet, recovery is now underway. IndiGo is expanding aggressively, while Air India, now under the Tata Group, is staging a long-awaited revival. But the sector’s core problems remain unresolved.

READ I India’s electronics manufacturing push needs policy stability

Bleeding cash in a high-cost industry

Aviation is among the most capital-intensive industries in the world, and Indian carriers face especially acute cost pressures.

Aviation turbine fuel constitutes 40–50% of airline operating costs. With India importing over 80% of its crude oil, global price fluctuations hit hard. To compound matters, ATF is subject to steep state taxes—up to 30%—making it among the most expensive jet fuels globally.

Most airlines operate on wafer-thin margins and rely heavily on debt to finance fleet expansion. The financial implosions of Jet Airways and Go First illustrate the perils of overleveraging. FY2024 saw collective industry losses of Rs 11,600–13,200 crore ($1.4–1.6 billion), despite a duopolistic market dominated by IndiGo and Air India.

India’s inadequate maintenance, repair, and overhaul (MRO) facilities force carriers to send aircraft abroad—to Singapore, the UAE, or Europe—raising costs and grounding aircraft for longer periods. High GST (18%) on MRO services and the lack of incentives discourage domestic investment, despite India’s clear potential as an MRO hub.

Regulatory and infrastructure bottlenecks

Nearly 40% of Indian airspace is under military control, leading to circuitous flight paths that increase fuel burn and operating costs.

Metro airports like Mumbai and Delhi are bursting at the seams. Mumbai, operating with a single runway, handles over 45 flights an hour—well above optimal capacity—causing delays and safety risks.

The Directorate General of Civil Aviation (DGCA) faces criticism for inadequate enforcement and safety lapses. Operational inefficiencies—from baggage mishandling to avoidable delays—diminish consumer confidence.

The shortage of trained pilots, cabin crew, and technicians is another growing concern. With pilot training costs reaching Rs 1 crore, the talent pipeline remains constrained. Meanwhile, intense competition and stressful working conditions fuel attrition and wage inflation.

While aviation accounts for around 2.5% of global CO₂ emissions, India’s rapidly growing passenger numbers threaten to push that share higher. The adoption of Sustainable Aviation Fuel (SAF) is key to decarbonising the sector, but uptake remains sluggish. SAF currently costs 3–5 times more than conventional jet fuel, and India lacks large-scale domestic production. Most supply is imported.

The way ahead

Without targeted subsidies or blending mandates, there is little incentive for airlines to switch. In the absence of clear policy direction, SAF adoption remains aspirational rather than actionable. To secure the sector’s long-term future, India must tackle its challenges head-on through targeted reforms and collaborative policymaking.

Build a domestic MRO ecosystem: Reducing GST on MRO services and offering tax breaks can attract private investment. Public-private partnerships should be leveraged to establish India as a competitive MRO hub.

Rationalise fuel pricing: Bringing ATF under GST would harmonise pricing across states and reduce input costs. Airlines should also adopt fuel hedging strategies to cushion volatility.

Expand infrastructure and airspace: Accelerating the UDAN scheme will decongest metros and improve regional connectivity. Phased release of military airspace to civilian use could streamline routing and lower fuel consumption.

Drive sustainability: Scaling up SAF production—using ethanol, non-edible oils, and waste-derived feedstock—should be a policy priority. Airlines must also invest in fuel-efficient aircraft such as the Airbus A320neo or Boeing 787 to reduce emissions.

Strengthen regulation: The DGCA needs to modernise its oversight regime through data-driven audits and AI-based monitoring systems. Enhanced enforcement will be key to restoring public trust and operational reliability.

India’s aviation industry is at a crossroads—buoyed by rising demand yet constrained by persistent inefficiencies. The resilience shown in the post-pandemic phase offers hope, but hope alone is not a strategy. Without structural reforms, the sector risks being caught in a cycle of boom and bust.

With smart policymaking, infrastructure investments, and environmental responsibility, the aviation industry can become not just a domestic success story, but a global one. The skies are promising, but only decisive action will allow this industry to truly take flight.

Dr Vijyapu Prasanna Kumar is Assistant Professor at Jindal School of Banking & Finance, O.P. Jindal Global University.