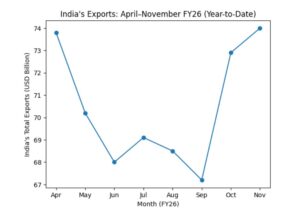

November delivered an uncommon piece of good news for Indian trade. Merchandise exports grew at their fastest pace in 41 months, cutting through weak global demand and persistent geopolitical strain. At a time when the WTO expects global merchandise volumes to remain subdued, India’s performance stood out for its timing as much as its scale. Trade flows, once again, responded more to economic logic than diplomatic comfort.

Merchandise exports expanded by nearly 20% year-on-year, reversing a slowdown that had lingered since mid-2022. The trade deficit narrowed to a five-month low, thanks to contracting imports. According to data released by the Ministry of Commerce and Industry, a sharp fall in gold imports and a softer petroleum bill did much of the immediate work.

READ | Trade deficit widens as India faces global headwinds

The relief mattered because it eased pressure on the external account at a moment when capital flows remain sensitive to global interest rates and risk sentiment.

Exports held up despite US tariffs

Exports to the United States rose by more than 22%, despite tariffs reaching 50% on select product lines. This resilience signals a shift away from pure price competition. Buyers in garments, engineering goods, and gems and jewellery are increasingly prioritising reliability, compliance, and supply-chain diversification.

India benefited from the “China-plus-one” strategy even when it required exporters to absorb tariff pain. That endurance reflects discipline, not comfort.

Exports to China nearly doubled, but the spike deserves caution. The base was low, and shipments remain concentrated in chemicals, iron ore, and select industrial inputs—categories that swing sharply with Chinese domestic cycles. This looks more like restocking than re-alignment. The bilateral trade relationship remains tactical, not structural.

READ | Trade deficit falls, but crude price risk persists

Timing, not policy, did the lifting

Part of November’s strength was circumstantial. Global supply chains normalised after holiday disruptions just as post-festive demand returned. Indian exporters in engineering goods, pharmaceuticals, and chemicals were ready.

Years spent building regulatory familiarity and buyer relationships paid off. When demand flickered back, Indian firms moved faster than competitors still tangled in logistics or cost pressures.

Export mix reveals deeper strength

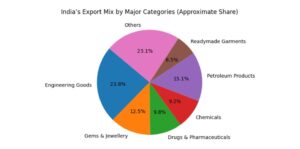

Non-petroleum, non-gems and jewellery exports—often treated as a proxy for manufacturing competitiveness—rose by nearly 20%. These are not impulse purchases. Engineering goods and chemicals reflect integration into global value chains and long-term contracts.

This is where India’s export story becomes less fragile and more earned.

Over the past decade, Indian firms have expanded their footprint in niche segments, supplying components and intermediates rather than finished goods alone. This strategy reduced exposure to short-term demand shocks.

Exports anchored in contracts behave differently from those driven by discretionary consumption. November rewarded that patience.

Logistics costs still cap ambition

What the numbers did not show is India’s persistent logistics handicap. According to the World Bank’s Logistics Performance Index, logistics costs in India remain around 13–14% of GDP, compared with 8–9% in China.

READ | To fix the US trade deficit, fix the fundamentals

Initiatives such as PM Gati Shakti and faster turnaround at ports like Mundra and JNPT are improving efficiency at the margin. But until logistics costs fall decisively, export gains will remain vulnerable to the next shipping or fuel shock.

Imports delivered relief, not reform

The narrowing trade deficit owed much to falling gold imports. That relief is inherently volatile. Gold demand follows prices and household behaviour, not policy design.

Lower petroleum prices also helped. Neither is a durable fix. Export strength matters most when it offsets these structurally sticky imports, not when it merely coincides with them.

Services still stabilise external account

Services exports grew 11.7% in November, once again cushioning the current account. Data from the Reserve Bank of India show IT services, business services, engineering design, and professional offerings absorbing merchandise trade volatility.

Yet technology disruption and rising protectionism argue against complacency. Goods exports must carry more weight.

Diversification is finally paying off

Exporters have deliberately reduced dependence on a few markets. While the US remains the top destination, growing footprints in West Asia, Africa, Latin America, and Southeast Asia softened the drag from Europe.

This strategy was slow and unglamorous. It is now delivering.

Nearly 45% of India’s merchandise exports come from MSMEs, according to SIDBI and RBI estimates. These firms face tighter credit, rising compliance costs, and shrinking margins after tariff absorption.

If MSMEs falter, export growth will narrow to capital-heavy sectors. That would weaken employment outcomes and political durability.

Exports must pass the jobs test

Export success ultimately faces a labour-market test. Capital-intensive gains in engineering and chemicals do not generate jobs at the scale of garments or leather. Data from the Periodic Labour Force Survey underline this imbalance.

In India, export growth without employment traction rarely survives policy scrutiny.

The IMF expects India’s current account deficit to widen again in the third quarter as global growth stays uneven and interest rates remain elevated. Trade uncertainty—from tariffs to the EU’s Carbon Border Adjustment Mechanism (CBAM)—has not receded.

The task now is clear. Turn episodic strength into durable competitiveness. That requires faster logistics reform, predictable export incentives such as RoDTEP, easier MSME credit, and standards compliance at scale. November showed what is possible. Policy must ensure it becomes normal.