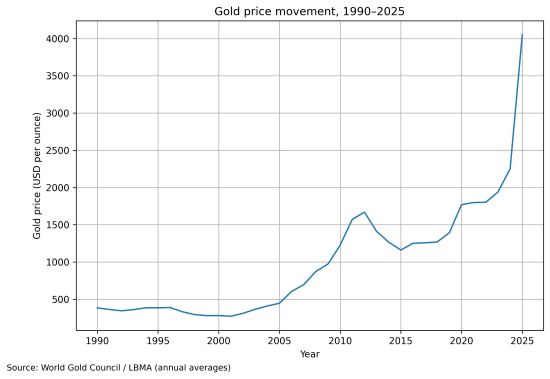

Gold price outlook: Gold has delivered an extraordinary run over the past two years. Prices crossed $4,000 an ounce in 2025 after rising more than 60% in a single calendar year, defying repeated calls of exhaustion. The rally matters because it reflects deeper shifts in global finance rather than a transient risk-off trade. Central banks are reworking reserve strategies. Investors are reassessing currency risk.

Political pressure on monetary authorities has returned to the centre of the global narrative. For countries like India, where the yellow metal is both a household asset and a macro variable affecting imports and the current account, the outlook for bullion is not a market curiosity. It is a policy signal.

The immediate question is whether gold has run too far, too fast. The more important question is what has changed beneath the surface.

READ I Cut interest rate or stall: Viksit Bharat hinges on RBI

Momentum meets monetary easing

In the near term, gold prices are supported by a familiar but powerful combination. US interest rates are falling. The dollar has weakened and geopolitical risk remains elevated.

The US Federal Reserve began its easing cycle in late 2025 as growth slowed and financial conditions tightened. Historically, the first phase of rate cuts tends to produce volatility in gold prices, followed by renewed upside once markets internalise a lower real-rate regime. That pattern has largely held. Inflation in the US remains above the Fed’s 2% target, while political pressure on the central bank has increased. The result is negative real yields across parts of the Treasury curve.

Gold thrives in that environment because it competes directly with cash and government bonds. A weaker dollar amplifies the effect, since bullion is priced in dollars and attracts non-US buyers when the currency falls.

Investor flows reflect this logic. According to J.P. Morgan Global Research, combined investor and central bank demand reached roughly 980 tonnes in the third quarter of 2025, more than 50% above the average of the previous four quarters. At prevailing gold prices, that translated into quarterly inflows of over $100 billion. These are not marginal reallocations.

The near-term risk is policy surprise. A sharp reacceleration of US growth, or a disorderly rise in bond yields, would cap gold prices. Barring that, gold is unlikely to correct meaningfully in the next 6–12 months.

READ I Interest rate cuts alone won’t fix India’s spending slump

Structural buyers will not disappear

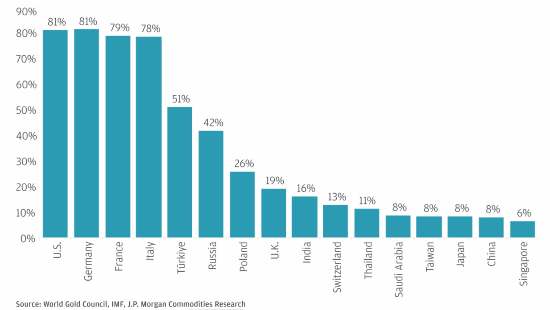

The strongest support for gold prices now comes from official reserves. Central banks have bought more than 1,000 tonnes of gold annually for three consecutive years, a break from past cycles. This is not speculative behaviour. It is strategic diversification.

Data from the International Monetary Fund shows that gold now accounts for nearly 20% of global official reserves, up from about 15% in 2023. Total central bank gold holdings are close to 36,200 tonnes. The shift accelerated after Russia’s foreign exchange reserves were frozen in 2022, but it has broadened since then.

Gold as a percentage of reserve holdings

Many emerging market central banks still hold less than 10% of their reserves in gold. If those institutions were to raise gold’s share to even 10%, the notional demand would run into hundreds of billions of dollars, even at current gold prices. J.P. Morgan estimates that such a rebalancing could require purchases of 1,200–2,600 tonnes, depending on price levels.

Importantly, high prices do not end this demand. They reduce the number of tonnes needed to achieve target reserve shares. That is a mechanical adjustment, not a reversal. Studies by the Bank for International Settlements have shown that emerging market central banks benefit from holding more than 20% of reserves in gold to hedge foreign exchange risk.

This is why central bank buying is best seen as a floor prices, not a speculative accelerator.

READ I Gold prices signal India’s shift to digital wealth

From hedge to portfolio anchor

Private investors have returned to gold in force, but the allocation remains modest by historical standards.

By the end of September 2025, gold accounted for about 2.8% of total global investor assets under management across equities, bonds, and alternatives. Two decades ago, that share was often higher during periods of stress. Analysts at J.P. Morgan and Goldman Sachs argue that a rise toward 4–5% over the next few years would not be extreme.

Exchange-traded funds have played a decisive role. ETF holdings rose by more than 100 tonnes in a single month in late 2025, the fastest pace in over three years. Lower interest rates make non-yielding assets more attractive, but something else is at work.

Gold is now serving two roles simultaneously. It is a hedge against monetary debasement in a world of expanding public debt. It is also an insurance asset against market drawdowns and geopolitical shocks. That dual function explains why gold has risen alongside equities at times, rather than merely offsetting them.

Goldman Sachs has estimated that if just 1% of privately held US Treasuries were reallocated to gold, prices could approach $5,000 an ounce. That is not a forecast. It is a measure of sensitivity.

Why gold prices signal work slowly

On the supply side, gold remains stubbornly inelastic. New mine supply responds slowly to price increases because of long project timelines, regulatory hurdles, and declining ore grades. Recycling does rise when gold prices surge, but not enough to offset demand shocks of the scale now being observed. According to the World Gold Council, annual mine production growth has been modest even during periods of sustained high prices.

This matters for the medium-term outlook. When demand rises quickly but supply adjusts slowly, prices tend to rebase higher rather than mean-revert. That is what appears to have happened since 2024.

For India, higher global gold prices translate into a larger import bill. Gold imports have historically widened the current account deficit during price spikes. The Reserve Bank of India has repeatedly flagged gold demand as a macro vulnerability, even as households treat the metal as a store of value. Managing this tension remains a challenge.

Gold price in an unstable monetary order

Over the long term, gold’s trajectory depends less on cyclical rate moves and more on the credibility of institutions. The post-1990 monetary order rested on central bank independence, fiscal restraint, and a dominant reserve currency. All three pillars are under strain. Public debt ratios have risen sharply. Political pressure on central banks has intensified. Sanctions and financial fragmentation have weakened trust in neutral reserve assets.

Gold benefits from each of these shifts without requiring a crisis to justify its role. That is why major banks now speak of “rebasing” rather than a bubble. J.P. Morgan expects average gold prices above $5,000 an ounce by late 2026, with further upside possible if diversification accelerates. Goldman Sachs sees $4,900 as a base case by December 2026, with upside risks.

These projections should not be read as precise targets. They reflect a broader judgment: gold is being repriced for a world with higher uncertainty and weaker monetary anchors.

Policy Circle has previously examined how gold’s resurgence fits into debates on de-dollarisation and reserve diversification. The current phase suggests that the trend is durable rather than episodic.

A higher floor, sharper risks

Gold is unlikely to move in a straight line from here. Near-term corrections are inevitable. But the drivers that lifted prices over the past two years remain intact.

Central banks are unlikely to reverse diversification. Investors remain under-allocated relative to history. Supply cannot respond quickly. Together, these forces imply that the floor for gold prices is higher than in past cycles.

The risk lies in complacency. For policymakers, especially in gold-importing economies, a world of structurally higher prices demands better management of external balances and household savings behaviour. For investors, gold should be treated neither as a speculative bet nor as a relic, but as a strategic asset in an increasingly unstable financial market.