India looks attractive on paper. It remains the fastest-growing major economy, has a large domestic market, offers political stability, and is being watched by global companies that want to reduce their dependence on China. Yet foreign investors are not committing capital at the scale New Delhi would like. Foreign capital is scarcer than before, and the government is now trying to draw more of it in.

Finance Minister Nirmala Sitharaman has said more measures are being prepared to encourage foreign investment. The statement recognises a simple fact: India can no longer assume that foreign capital will arrive merely because growth is strong.

READ | China FDI policy shifts from blanket curbs to safeguards

Foreign capital sees India’s gains and gaps

India’s problem is not absence of opportunity. Investors see opportunity and obstacles together. The government has eased rules for foreign participation in government securities and offered tax exemptions on income and capital gains from sovereign debt. More changes are expected as the Finance Ministry seeks to protect the external account against geopolitical shocks, volatile commodity prices and uncertainty in financial markets.

The harder issue lies beyond tax concessions and regulatory fine-tuning. Investors welcome incentives, but they commit long-term capital when they trust the business environment. Chief Economic Adviser V Anantha Nageswaran has described the present moment as a live balance-of-payments stress test. The conflict in West Asia has raised energy prices, shipping costs and insurance costs. It has weakened the rupee and added to inflation risks. In such a setting, the government wants larger and steadier capital inflows. Periodic relaxations will not be enough.

The distinction between portfolio flows and long-term investment matters. Foreign portfolio investors respond to yield differentials, liquidity and short-term market openings. Their money can enter quickly and leave as quickly. Foreign direct investment signals confidence in a country’s long-term growth, institutions and policy stability. India has found it difficult to sustain such inflows.

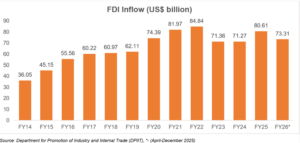

Net FDI inflows have stayed weak despite strong growth. One reason is higher repatriation of profits and disinvestment by existing foreign investors. Foreign companies are taking more money out of India than before. New investments are being offset by withdrawals, limiting the net gain.

READ | FDI inflows rebound, but capital quality issues persist

Foreign investment depends on states

India has improved its business climate, but governance remains uneven across states. Investment decisions turn on land acquisition, power supply, logistics, local permissions and administrative response. Some states have built a working investment apparatus. Others still impose delays after the investment announcement has been made.

This is where national reform meets its limit. Projects are executed in states. A central notification does not acquire land, connect power, clear local approvals or move goods to port. Investors price this gap into their decisions.

The global setting has also changed. Capital is no longer as cheap or as mobile as it was during the years of ultra-low interest rates. Advanced economies now direct investment towards national security, technology and supply-chain resilience. Investment choices are shaped by geopolitics as much as returns. Countries now compete for capital tied to semiconductors, critical minerals, clean energy and advanced manufacturing.

India has strengths in this contest. Global capability centres and data centres show that multinationals still find value in India. The domestic market remains a major draw. But these advantages cannot offset weak institutions indefinitely. The recent volatility caused by the West Asia conflict has exposed India’s external vulnerabilities. Crude oil prices, a weaker rupee and subsidy pressures can disturb macroeconomic stability quickly. Financial incentives may help at the margin. They cannot provide a durable answer.

READ | Why India’s FDI numbers are flashing a warning

India’s foreign capital agenda

Countries that attract long-term foreign investment do so through reliable institutions. Investors value predictable policy, efficient courts, clear regulation, dependable infrastructure and macroeconomic stability. Incentives can influence timing. They rarely decide the final destination.

This is where India’s approach needs correction. More tinkering with tax rules or investment norms will produce limited gains. Much of the easier liberalisation has already been done. India has opened many sectors, eased ownership restrictions and made space for foreign investors in bond markets. Additional concessions may bring some incremental capital, especially into debt. They will not transform investment behaviour.

The next reforms are harder. India needs faster contract enforcement, better bankruptcy resolution, more predictable regulators, stronger state-level governance, lower logistics costs and implementation of labour reforms. These cannot be delivered by a Finance Ministry circular. They require courts, regulators, state governments and local administrations to work better.

Until that happens, fresh measures to attract foreign capital will produce announcements rather than an investment surge. India’s growth story is still strong. The question is whether investors can trust the operating conditions enough to put long-term money behind it.