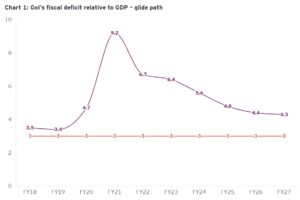

For 2026-27, fiscal consolidation remains central to the government’s macroeconomic strategy. Yet, the path is beginning to show visible strain. Current estimates suggest the fiscal deficit may exceed the glide path target of 4.3% of GDP, with some projections closer to 4.5%. These variations reflect different assumptions, but the underlying drivers are similar: external shocks, policy responses to those shocks, and rising expenditure commitments.

The consolidation effort since the pandemic has been deliberate. Fiscal deficit was brought down from elevated levels through a combination of revenue recovery and expenditure restraint. The Union Budget reaffirmed this direction, with a medium-term objective of reducing fiscal deficit below 4.5% of GDP by 2025–26 and then to 4.3% in 2026–27. This trajectory assumed steady nominal GDP growth, buoyant tax revenues, and a gradual easing of subsidy pressures.

READ I India’s FTAs need competitiveness, not just access

Subsidy pressures return

That last assumption is no longer holding. Subsidies—food, fertiliser and fuel—continue to dominate discretionary spending space, and recent developments have reversed earlier gains.

Over the past two years, subsidy outgoes had moderated as global commodity prices stabilised and administrative measures improved targeting. That phase now appears to be ending. Geopolitical tensions in West Asia have unsettled energy markets, and the effects are visible in domestic price pressures, including the recent LPG stress. Given India’s dependence on imported crude, such volatility quickly translates into fiscal pressure, as the government is often compelled to intervene to stabilise prices.

Fertiliser subsidies are under similar strain. Nitrogen fertilisers are closely linked to natural gas prices, which have risen amid supply disruptions. Recent trends indicate urea prices rising by about $100 per tonne to around $600, while DAP prices have moved from roughly $650–670 to $750–770 per tonne. Since farm-gate prices are largely insulated, the fiscal burden absorbs the increase.

Food subsidies, though more predictable, remain structurally large. The continuation of free or subsidised grain distribution under welfare programmes leaves limited room for compression. Taken together, these components risk undoing part of the fiscal adjustment achieved in recent years.

READ I India growth story faces deeper structural gaps

Debt burden and interest payments

Beyond the annual deficit, the underlying constraint is the stock of public debt and the cost of servicing it. Interest payments already absorb a substantial share of the Union government’s revenue receipts, limiting flexibility in expenditure decisions. This reduces the room for counter-cyclical policy and makes even modest slippages in the fiscal deficit more consequential.

The issue is not just the size of the fiscal deficit in a given year, but the persistence of deficits that add to debt and lock in future interest obligations. Without a sustained reduction in the primary deficit, fiscal consolidation risks becoming a moving target.

READ I Industrial policy revival: What India must get right

Policy buffers and revenue trade-offs

The government has sought to retain flexibility. In March, the Ministry of Finance announced an Economic Stabilisation Fund of about ₹1 trillion to respond to external shocks. The intent is to enable targeted interventions—whether through subsidies or temporary tax relief—without immediate disruption to budgeted allocations.

However, such buffers come with trade-offs. Temporary tax measures, including customs duty reductions on key inputs, can support industry by lowering costs, but they also imply revenue foregone at a time when fiscal space is already constrained. These decisions, while necessary in the short term, complicate the consolidation arithmetic.

Revenue assumptions themselves face limits. Budget projections rely on continued gains from formalisation, improved compliance, and economic expansion. But buoyancy has its bounds. A slowdown in growth would directly affect tax collections, and corporate tax revenues may moderate if profitability is squeezed by higher input costs.

At the same time, non-tax revenue avenues such as disinvestment and asset monetisation have delivered uneven outcomes. While there has been progress in specific transactions, aggregate receipts have often fallen short of targets. This reduces the ability to offset rising expenditure pressures.

Managing fiscal deficit slippage

The government is therefore managing multiple constraints: external volatility, domestic welfare commitments, and limited revenue headroom. In this context, the question is not whether the fiscal deficit will deviate marginally from the target, but whether such deviation is contained and purposeful.

A slippage towards 4.5% of GDP, if driven by targeted and temporary measures, is unlikely to undermine macroeconomic stability. The risk lies in persistent expansion of revenue expenditure without corresponding gains in growth or efficiency.

Improving subsidy delivery remains the most immediate lever. Direct benefit transfers, tighter targeting, and periodic price adjustments can contain costs without diluting support. In fertilisers, a shift towards nutrient-based pricing and incentives for balanced usage can reduce distortions over time.

Rationalisation of centrally sponsored schemes and elimination of duplication can yield savings. At the same time, public capital expenditure should be protected, given its role in sustaining medium-term growth. The composition of spending will matter as much as its aggregate level.

Fiscal consolidation, therefore, is entering a more difficult phase. The easier gains from post-pandemic normalisation have been realised. What remains is a tighter balancing act between growth, welfare, and macroeconomic stability.