The Federal Reserve’s decision to cut the federal funds rate by 25 basis points is being hailed by some as a relief from high borrowing costs. But this move may in fact steer the US economy towards deeper troubles. As inflation remains uncomfortably above target, labour markets show cracks, and political pressure mounts, the Fed appears to be taking a gamble. While Fed rate cuts may seem attractive amid slowed job growth, they risk fuelling inflation, undermining credibility, and exacerbating financial instability.

The American economy is in a delicate phase. Growth has slowed, with GDP expected to expand at a modest 1.6% this year — barely above the recession threshold. Job creation has decelerated sharply, averaging just 29,000 positions in recent months, compared with more than 130,000 earlier in the year. Consumer spending remains resilient, but borrowing costs have weighed heavily on housing and autos. Meanwhile, tariffs have rekindled inflationary pressures, keeping core inflation above 3%, far from the Fed’s 2% target. In this uneasy environment, the Fed’s rate cut is less an act of confidence than one of risk management — yet the risks may overwhelm the intended relief.

READ I RBI’s rupee defence could hurt Indian economy

Fed rate cut impact

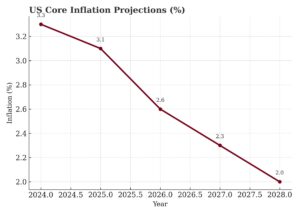

Inflation risks remain sticky: The Fed has lowered the target range for the federal funds rate to 4.00%–4.25%, the first cut since December 2024. Yet inflation has not returned to comfort levels. Core inflation, which strips out volatile components, is expected to end the year at 3.1%, and even the Fed’s own projections suggest that inflation will not reach its 2% target until 2028. By loosening monetary policy when inflation is still elevated, the Fed risks embedding higher price expectations into household and business behaviour. Once expectations rise, breaking the cycle demands far harsher tightening later — a lesson the US painfully learned in the 1970s.

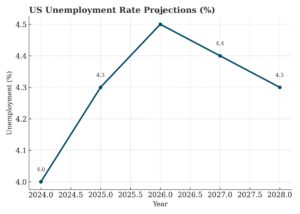

Labour market weakness: The justification for easing lies in the apparent fragility of the labour market. Payroll growth has nearly stalled, revisions to earlier data paint a weaker picture, and the unemployment rate has edged up to 4.3%. Fed Chair Jerome Powell has framed the cut as a “risk management” exercise, meant to pre-empt further job losses. But the weakness is uneven. Many firms are freezing hiring rather than embarking on large layoffs, while wage growth, though moderating, has not collapsed. Cutting rates on the basis of tentative signals risks acting too early. If labour slack does not deepen, monetary easing may only stoke inflationary pressures without delivering meaningful job support.

Stagflation fears and growth-inflation trade-off: The Fed’s move raises the spectre of stagflation — a toxic combination of weak growth and persistent inflation. Tariffs imposed by the Trump administration have already pushed up import costs, while supply-chain frictions continue to raise prices. Housing shortages and sticky shelter inflation remain unresolved. Analysts warn that rate cuts in such an environment may stimulate demand without easing supply constraints, worsening price pressures while growth remains tepid. The Fed’s own dot plot projects growth barely above 1.5% and inflation above 3% in 2026. The danger is that monetary policy may end up trapped between supporting growth and restraining prices, succeeding at neither.

Financial stability and credibility risks: Beyond macroeconomic trade-offs, premature easing carries financial stability risks. Yield curves may invert or flatten, confusing signals for credit markets. Investors have already reacted warily: stock markets offered only modest gains after the cut, while bond markets reflected concern about persistent inflation. The greater threat lies in credibility. Political pressure has been intense, with the Trump administration openly demanding deeper cuts and even attempting to remove a sitting Fed governor. Central bank independence, long considered a bedrock of US financial stability, now faces its most severe test in decades. If markets perceive the Fed as bowing to political interference, inflation expectations will rise, borrowing costs may increase, and the dollar’s reserve status could come under scrutiny.

Global spillovers and inflation risks

The Fed rate cut also reverberates far beyond US shores. A softer dollar can shift global capital flows, destabilising emerging markets. Persistent US inflation raises the costs of imported goods worldwide, and higher American demand for commodities can push up global prices. Tariff-driven cost pressures add another layer of uncertainty. For emerging economies already battling imported inflation, US easing may trigger currency depreciation and higher import bills. In an interconnected world, the risks of premature easing extend well beyond America’s borders.

Going forward, the Fed must adopt a cautious, data-anchored approach. Rate cuts should not be automatic; they must follow clear evidence of sustained deterioration in the labour market, such as rising unemployment over multiple months or a prolonged contraction in payrolls. Acting pre-emptively risks entrenching inflation, while delaying action until weakness is more certain ensures that cuts are both necessary and effective.

Equally important is the need to re-anchor inflation expectations. The Fed must communicate unequivocally that its long-term commitment to 2% inflation remains intact. Clear messaging, coupled with readiness to reverse course if inflation worsens, will reassure markets that easing is not an abandonment of discipline.

Financial stability must remain a central consideration. Regulators should closely monitor credit spreads, non-bank leverage, and vulnerabilities in the housing sector. The Fed’s dual role as monetary authority and stability guardian demands that rate cuts not endanger systemic resilience.

Safeguarding institutional independence is paramount. Political attempts to interfere with Fed governance erode confidence in monetary policy. By defending its autonomy, the Fed preserves the credibility on which all its actions ultimately rest.

Finally, monetary policy must not work in isolation. Fiscal discipline, trade policy, and supply-side reforms must share the burden. Tariffs, in particular, are fuelling price pressures; removing them would ease inflation far more effectively than rate cuts. A coordinated approach is the only durable path to balancing growth, jobs, and price stability.

The Fed rate cut may relieve borrowers today, but the long-term risks outweigh the short-term benefits. Inflation remains sticky, the labour market is not yet in freefall, stagflation looms, and the institution’s credibility is under siege. A steadier hand—anchored in data, disciplined in communication, vigilant about stability, and insulated from politics — is what the US economy requires. The Fed must not confuse the balm of temporary relief with the foundation of lasting stability.