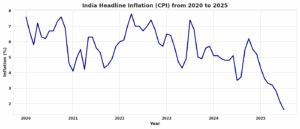

India’s retail inflation fell to 1.55% in July 2025 — the lowest since June 2017. The slide was driven largely by a sharp drop in food prices, especially vegetables and pulses, alongside the Reserve Bank of India’s decision to hold interest rates at 5.5%. On the surface, this is a victory for economic management. But the lived experience of many Indians tells a more complicated story: are prices really falling for consumers, or does the official number hide more than it reveals?

The RBI attributes the benign inflation outlook to healthy crop sowing and comfortable food grain stocks, hinting that monetary policy could turn more accommodative. Food inflation in July was -1.76%, helped by a 20.69% year-on-year drop in vegetable prices and a 13.76% fall in pulses. Given that food accounts for about 40% of the Consumer Price Index (CPI) basket, such declines should, in theory, ease household budgets — particularly for low-income families where food is a dominant expense.

Lower food prices, while welcome for consumers, hurt farmers’ incomes and risk dampening rural demand. This could ripple through the wider economy, especially in sectors dependent on agricultural spending. As Kotak Mahindra Bank’s Upasna Bhardwaj notes, higher real rural wages and expected crop arrivals may soften the blow, but the immediate impact on farm earnings is severe.

READ I US tariffs force India to accelerate diversification plan

Core inflation tells another story

The headline number also conceals important variation. Core inflation — stripping out volatile food and energy — remains steady at around 4%–4.12%, signalling that underlying domestic demand pressures persist. Urban consumers, who spend proportionally less on food, are feeling sharper increases in non-food essentials.

Housing rents (9.5% CPI weight) rose 3.1% in June, with actual increases in metros often higher. Hospital and nursing charges, though only 0.44% of the CPI basket, climbed 6.6%, while education fees (2.9% weight) rose 5.4%. For households with school-going children or elderly dependents, these costs overshadow any gains from cheaper vegetables.

A CPI inflation basket stuck in time

Part of the disconnect lies in how inflation is measured. The CPI basket is still based on 2011–12 consumption patterns, with outdated items like cassettes and CDs and inadequate representation of mobile phones, internet charges, or other modern essentials. This outdated structure means the official rate may understate cost-of-living increases.

The distortions can be stark. Gold prices, up 36% year-on-year in June 2025, are a major expense for households planning weddings, but carry minimal weight in CPI. Similarly, the high perceived cost of big-ticket items like smartphones or leisure spending (multiplex tickets, snacks) barely registers in official inflation.

Another unrecorded factor is “shrinkflation,” where companies keep prices unchanged but reduce product sizes, effectively raising per-unit costs without affecting the inflation print. Despite the fall from 6.2% inflation in October 2024 to 2.1% in June 2025, prices still rose 0.6% month-on-month in June, and over the past decade, retail prices are up roughly 58%. For most consumers, this long-term climb overshadows short-term relief.

External headwinds and policy dilemmas

The inflation picture is further complicated by external shocks. Fresh US tariffs on Indian exports could shave 30–40 basis points off GDP growth, increasing the case for RBI rate cuts. But the central bank remains cautious, wary of a short-term rebound in inflation — especially as vegetable prices have already begun rising month-on-month.

For households heavily reliant on food purchases, recent price falls bring modest relief. For urban middle-class families facing rising rents, school fees, and healthcare costs, the headline figure feels disconnected from daily reality. “Personal inflation” depends on spending patterns, location, and lifestyle — often far exceeding the national average.

Until the CPI basket is updated to reflect current consumption, and policymakers address the rural distress caused by low food prices, the feel-good factor from a sub-2% inflation rate will remain unevenly shared. The RBI’s challenge is to support growth without underestimating the real cost pressures confronting Indian households.