The months ahead of Budget 2026 will invite familiar claims of resilience. Growth remains firm, but the RBI’s reading of the cycle suggests a less comfortable truth: the economy is being carried by a narrow set of drivers, while the investment engine is still hesitant and inflation risks remain concentrated in food. The policy test for the Budget is therefore not to “support growth” in the abstract, but to change the composition of demand toward durable capital formation, and to do so without widening fiscal vulnerabilities or forcing the central bank back into a defensive stance.

The NSO’s first advance estimate for 2025-26 has projected 7.4% growth. The IMF has also lifted its FY26 forecast, citing stronger late-year momentum. Yet the RBI’s State of the Economy assessment points to a less comfortable reading of the cycle. Growth is holding, but its composition is doing the heavy lifting. The second-half pick-up that the RBI flags is real, but it is also a reminder that the first half was soft enough to pull the full-year number down. The policy question for Budget 2026 is not whether India is growing. It is whether the growth mix is shifting towards durable investment and productivity, or getting trapped in a narrow set of drivers.

READ | Budget 2026: The fiscal arithmetic is getting harder

Growth is moderating, and the drag is telling

The RBI’s diagnosis matters more than the deceleration itself. The drags were not incidental. Private capex did not show a “visible” pick-up, and general government capital expenditure growth also moderated, pulling down gross fixed investment and manufacturing’s contribution to GVA. This is not a statistical quirk. It is a signal that the investment cycle is still being carried by selective balance sheets and public infrastructure outlays, not by broad-based capacity creation.

If Budget 2026 is framed as an exercise in “supporting growth”, it will miss the point. The economy does not need another generic growth push. It needs a rebalancing of the growth engine away from consumption-led spurts and towards investment that raises output potential.

Consumption is improving, but it is not a strategy

The RBI describes private final consumption as the brightening spot, helped by e-commerce and quick commerce, and notes early signs of better corporate earnings in Q3 relative to H1. The consumption impulse is visible in staples, housing demand in mid-income and premium segments, and a rural recovery supported by a better agricultural season.

READ | The big question for Budget 2026

But consumption cannot substitute for investment. It can, at best, buy time. A consumption push that is not matched by an investment response risks importing inflation through supply bottlenecks and widening the trade deficit through higher import demand. The RBI’s own trade numbers show how quickly the external account can respond when domestic demand firms.

Budget 2026 should therefore treat consumption relief, if any, as targeted and time-bound. It cannot become the organising principle of fiscal policy.

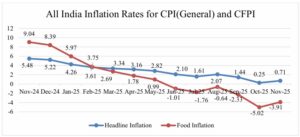

Food inflation is a macro risk

The food inflation has fallen sharply in November 2025 to -3.91% on the back of decreasing prices for vegetables, eggs, meat, fish, spices, and fuel. But, there is no respite on the overall cost of living. Prices, continues to rise in edible oils, fruits, and prepared meals. The RBI’s warning is precise: sticky food inflation, alongside firmer rural wages and corporate salary outgoes, can generate second-round effects.

This matters for Budget 2026 because food inflation is not only a welfare problem. It shapes monetary space. When food inflation stays elevated, the central bank’s ability to support growth through easing becomes constrained, even if core inflation is steady. It also distorts household budgets in a way that looks like a tax, especially on urban middle-income consumers that are “pinning hopes” on relief through higher disposable incomes.

A credible Budget response is not to announce another broad subsidy layer. It is to show administrative capacity on food supply. Buffer management, release policy, and logistics are not glamorous, but they are decisive. The RBI’s own data on procurement and buffer norms underline that India often has stocks, but price behaviour still turns volatile when distribution and market supply fail to respond smoothly. Budget 2026 should reward execution in storage, transport, and market integration, not only new scheme architecture.

READ | Budget 2026: Rural incomes are India’s weak spot

Trade deficit is widening

India’s merchandise trade deficit widened to $21.9 billion in December 2024, and the cumulative deficit for April-December widened to $210.8 billion. Petroleum products and electronic goods dominate the deficit profile. The oil share of the monthly deficit rose as oil and non-oil deficits widened. This is the external mirror of the growth mix.

Services exports are doing what they have done for a decade: stabilising the macroeconomy. Services exports grew strongly, and net services earnings remained healthy. Remittances and services cushioned the current account deficit, which the RBI notes at 1.2% of GDP in Q2:2024-25, with reserves accreting as capital inflows exceeded the CAD.

But this cushion should not be treated as a licence to be casual about manufacturing competitiveness. A widening merchandise deficit driven by electronics and capital goods is a structural competitiveness problem. Budget 2026 should not claim success by pointing to a manageable CAD. It should focus on reducing the economy’s import intensity in the sectors where domestic capability is plausible, and where policy already claims intent.

Fiscal arithmetic is tightening

The RBI notes that central government revenue expenditure growth picked up, interest payments kept rising, subsidy outgo increased, and capital expenditure moderated during April-November 2024, even though November itself showed a strong capex print. It also records the importance of the RBI’s surplus transfer in lifting non-tax revenue.

This combination is a warning about fiscal comfort. A one-off boost from central bank transfers cannot be the foundation for recurring commitments. Nor can Budget 2026 treat capex as a slogan. The real test will be capex quality and crowding-in. Where does public capex create investable demand for private firms, and where does it remain a government-only pipeline?

There is also a federal dimension. The RBI’s state-level snapshot shows states’ revenue receipts rising, but capital expenditure lower than last year’s levels. If the Union wants capex-led growth, Budget 2026 will need to structure incentives that make state capex predictable and less hostage to within-year cash management.

Financial conditions are sending mixed signals

The RBI’s liquidity narrative is unusually instructive. System liquidity turned into deficit from mid-December, the central bank injected large sums via variable rate repos, and yet banks still placed funds in the standing deposit facility. The RBI reads this correctly as skewed liquidity distribution and a degree of reluctance to on-lend in money markets.

At the same time, the rate corridor was tested, term money market rates stayed elevated, and credit growth moderated from the previous year. These are not crisis signals. They are friction indicators. They suggest that monetary transmission is not only about policy rates. It is also about liquidity plumbing, risk appetite, and the price of term funding for NBFCs and lower-rated borrowers.

Budget 2026 cannot directly fix market plumbing, but it can avoid making it worse. Large, poorly timed borrowings, or fiscal surprises late in the year, can tighten financial conditions when the economy needs smoother credit intermediation.

READ | Budget 2026: Fiscal consolidation versus welfare spending

What Budget 2026 should signal

The RBI points to genuine momentum in renewables, green bonds, and capacity milestones in solar and wind, alongside progress in ethanol blending. These are important, and they offer a sector where private investment can be mobilised at scale.

But the green transition is not only a climate chapter. It is an industrial opportunity. Budget 2026 should treat it as such, with a focus on domestic value chains, grid readiness, storage, and the financing architecture that can fund long-duration assets without loading risk onto banks alone.

Budget 2026 should be judged on whether it acknowledges three realities embedded in the RBI’s assessment.

First, growth is resilient, but investment is the weak link that keeps reappearing.

Second, food inflation is the constraint that can quickly tighten monetary space and compress real incomes.

Third, the external account is stable mainly because services exports and capital inflows keep cushioning the merchandise deficit, not because the deficit has been structurally tamed.

A Budget that is honest about these constraints, and disciplined in how it allocates fiscal room, will do more for credibility than any headline-grabbing announcement.