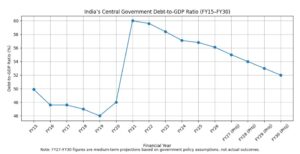

Fiscal consolidation vs welfare spending: The government has set itself an ambitious fiscal task. In the forthcoming Union Budget, it aims to reduce the debt-to-GDP ratio to about 54.5–55% by FY27, down from the 56.1% budgeted for FY26. Beyond that lies a larger target- bringing debt closer to 50% by FY31. The arithmetic matters, but the real question is political. Can India consolidate its finances without cutting back on social sector and welfare spending that has become integral to household security?

Debt, not the annual deficit, is the binding constraint on fiscal policy. By anchoring consolidation to debt rather than headline deficit numbers, the government gains room to respond to economic shocks. Yet India’s fiscal history offers a cautionary lesson. Consolidation has often been achieved by trimming what is easiest to cut rather than what is least damaging to growth or social outcomes.

READ | Fiscal consolidation: Can India have high growth and low deficit?

Welfare spending is hard to cut

Over the past decade, welfare schemes have moved from being temporary support measures to becoming part of the social contract. Food security under the National Food Security Act, employment guarantees through MGNREGA, health insurance via Ayushman Bharat, and a wide range of direct benefit transfers now shape household expectations. They also act as automatic stabilisers when growth falters.

Cutting these outlays sharply would carry economic and political costs. Private consumption remains uneven, and job creation has not kept pace with headline GDP growth. Any visible rollback of welfare spending risks weakening demand at a time when the recovery is still fragile. This significantly narrows the government’s room for manoeuvre.

Revenue reform: Limited room, hard choices

One route to consolidation lies on the revenue side. India’s tax-to-GDP ratio has improved in recent years, helped by Goods and Services Tax stabilisation and stronger income-tax compliance. Even so, it remains modest for an economy with India’s development needs.

The scope for easy gains is now limited. Broadening the tax base without raising rates has long been the preferred approach, but much of the low-hanging fruit has already been harvested. Further progress will require politically harder steps—deeper GST rate rationalisation, pruning exemptions, and addressing the persistent under-taxation of certain asset classes. These reforms are administratively feasible but politically costly.

READ | Fiscal consolidation: Can Indian economy survive a deficit squeeze

Growth-led consolidation and its limits

The government has increasingly focused on the quality of expenditure. Capital spending has been prioritised over revenue expenditure, reflecting its higher multiplier effects and contribution to medium-term growth. If nominal GDP growth stays near the upper end of the assumed 10.5–11% range, the debt ratio can fall even with a relatively moderate fiscal deficit.

This growth-led path is embedded in the government’s medium-term fiscal framework, which models alternative debt trajectories based on different growth assumptions. The weakness is evident. Growth depends on global demand, domestic investment, and private consumption—factors largely outside the finance ministry’s direct control. A slowdown would quickly upset the consolidation calculus.

Interest burdens and the hidden squeeze

A less visible constraint complicates this strategy: interest payments. At the Centre, interest costs now absorb more than two-fifths of net revenue receipts, making them the single largest claim on the exchequer. Unlike capital spending or subsidies, interest outgo is non-discretionary. It cannot be postponed without risking market confidence, and it rises automatically as debt accumulates or borrowing costs increase.

This has direct implications for welfare protection. Even when social sector allocations are maintained in nominal terms, rising interest payments can quietly erode their real value. As a larger share of revenue is pre-empted by debt servicing, the adjustment burden shifts to areas that are easier to compress administratively—scheme expansion, maintenance spending, and timely fund releases. Welfare is rarely cut outright; it is often thinned out.

The structure of public debt adds to this pressure. Greater reliance on small savings, shorter maturities, and episodic spikes in bond yields can push up servicing costs even without fresh fiscal slippage. Consolidation driven solely by deficit targets may therefore prove illusory—numerically tidy, but fiscally rigid.

READ | Indian economy: Focus on fiscal consolidation will hurt fragile recovery

Subsidy reform without rolling back entitlements

Another option lies in improving efficiency rather than cutting benefits. India’s experience with direct benefit transfers shows that better targeting and reduced leakage can create fiscal space. Food and fertiliser subsidies, in particular, have seen improvements in delivery efficiency, even though their absolute size remains large.

The political challenge is perception. Efficiency gains are largely invisible, while any perceived reduction in entitlements is immediately felt. This makes sequencing critical. Gradual reform that protects beneficiary coverage while improving delivery offers a more credible route to consolidation than blunt expenditure cuts.

The IMF’s warning and the federal risk

CareEdge Ratings estimates that the fiscal deficit could fall to around 4.2–4.3% of GDP by FY27 if nominal growth averages about 10.7%. On these assumptions, public debt could still approach 50% of GDP by FY31.

In its latest Article IV consultation, the International Monetary Fund has urged India to adopt a more ambitious medium-term debt target and to include state government liabilities within the debt anchor. From a sustainability perspective, the advice is sound. Combined public sector debt is what ultimately determines fiscal risk.

But the recommendation raises a federal concern. States account for a large share of social sector spending—health, education, nutrition, and welfare delivery. A tighter combined debt target could force adjustment at the state level, even if the Centre protects its own programmes. Consolidation at the top may thus translate into austerity at the front lines of social policy.

The political economy of consolidation

Reducing the deficit without cutting welfare is ultimately a political choice. Fiscal consolidation is often framed as a technical necessity, but in India it is inseparable from distributional outcomes. Protecting social expenditure implies that adjustment must come from elsewhere—higher and more efficient revenue mobilisation, better targeting of subsidies, and a sustained push for growth-enhancing public investment.

None of these choices is easy. Yet a mechanical pursuit of debt targets, without regard to social consequences, risks producing a fiscally neat but socially brittle outcome. India’s demographic profile ensures that demands on the state will only rise. Debt discipline can anchor fiscal policy, but it cannot substitute for a broader debate on the size and role of government in a developing economy.