The Union Budget 2026–27 is being presented as a reaffirmation of fiscal discipline. The headline numbers support that claim. The fiscal deficit is budgeted at 4.3 per cent of GDP, a marginal improvement over the 4.4 per cent targeted for 2025–26. The debt-to-GDP ratio is projected to decline to 55.6 per cent from 56.1 per cent. After years of pandemic-induced expansion, the finance ministry is signalling a return to a narrower fiscal corridor. The question is not intent, but credibility under tightening constraints.

Finance minister Nirmala Sitharaman has chosen continuity over surprise. This is her ninth consecutive budget and it shows. The consolidation path remains incremental, not abrupt. The glide path set out earlier—bringing the deficit below 4.5 per cent by 2025-26—has been broadly respected. What the budget attempts now is to hold that line while sustaining public investment and managing a heavy borrowing programme. That balancing act defines the budget more than any sectoral announcement.

READ I Budget 2026: The hidden costs of India’s fiscal consolidation

A narrow consolidation window

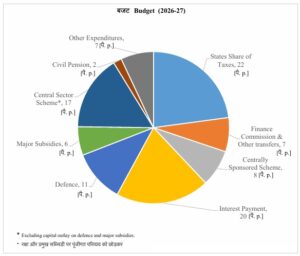

The room for fiscal manoeuvre is limited by arithmetic. Nominal GDP growth assumptions remain robust, supported by the Economic Survey’s projection of 6.8–7.2 per cent real growth for 2026–27. But expenditure rigidities have hardened. Interest payments claims a large share of the revenues. Subsidies, though lower than pandemic peaks, have not reverted to pre-2020 norms. Defence outlays remain sticky amid geopolitical uncertainty. Consolidation, therefore, is being pursued through restraint rather than retrenchment.

This explains the modest reduction in the deficit number. A 10 basis point improvement may appear cosmetic, but it reflects the political economy of adjustment. Sharp expenditure cuts would have undermined growth momentum ahead of a fragile global cycle. Large tax increases would have conflicted with the government’s effort to keep consumption buoyant. The budget chooses the path of least resistance, accepting slower consolidation in exchange for stability.

READ I Why Budget 2026 is a harder test than GDP numbers suggest

Capex as fiscal signalling

Public capital expenditure remains the centrepiece of the budget’s growth narrative. The allocation of ₹12.2 lakh crore for infrastructure in 2026–27 represents an 8.8 per cent increase over the current year and extends the post-pandemic strategy of state-led investment. This is not merely a growth lever; it is also a signalling device. By protecting capex while compressing the deficit, the finance ministry is attempting to reassure markets that consolidation will not come at the cost of medium-term growth potential.

Market reaction point to mixed success. Equity indices fell after the budget speech and bond markets remain uneasy. While the capex number back manufacturing and private investment, it does little to reduce the near-term fiscal stress. The strategy relies more on crowding in private capital than delivering instant fiscal relief.

READ I Record trade surplus masks weakness of China’s economy

Debt targets and borrowing reality

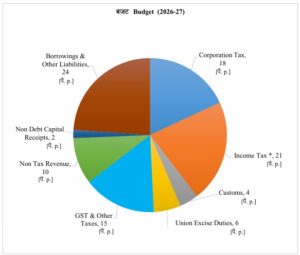

The government’s formal shift to a debt-to-GDP anchor is significant. Targeting a ratio of 55.6 per cent next year gives consolidation a medium-term reference point rather than a single-year deficit obsession. Yet this framework is under strain from the scale of gross borrowing. The budget takes gross market borrowings to a record ₹17.2 lakh crore in 2026–27. Net borrowing is comparatively low, but the sentiment is affected by the headline number.

This tension exposes the core vulnerability of the consolidation effort. Debt ratios may fall on paper, helped by nominal growth, but financing requirements remain large. Central and state borrowing combined continues to test market absorption capacity. Bond yields have already hardened despite significant policy rate cuts and liquidity support from the Reserve Bank of India. The budget offers no clear roadmap for easing this pressure beyond faith in growth and institutional support.

Manufacturing push without fiscal expansion

One way the budget attempts to square the circle is by linking consolidation with industrial policy. The focus on seven manufacturing sectors—semiconductors, pharmaceuticals, rare-earth magnets, chemicals, capital goods, textiles and sports goods—is meant to signal a shift towards higher domestic value addition. Initiatives such as the second phase of the semiconductor mission and the Bio Pharma Shakti programme are structured as medium-term commitments rather than large upfront fiscal shocks.

This approach reflects caution. The government has announced targeted schemes instead of broad-based incentives, often co-funded with industry or states. The intent is to limit immediate budgetary impact while claiming strategic ambition. Whether these programmes deliver sufficient private investment to justify their fiscal footprint remains uncertain. What is clear is that they are designed to fit within consolidation, not challenge it.

Growth dependence and external risk

The sustainability of fiscal consolidation rests heavily on growth outcomes. The budget assumes that India will continue to outperform most major economies, even as global trade remains unsettled and protectionist pressures persist. The recent resilience in the face of US tariff threat has reinforced confidence in domestic demand and public investment. But this dependence cuts both ways. Any growth disappointment would quickly reopen the fiscal gap.

There is also limited acknowledgement of state-level fiscal stress. While central consolidation is emphasised, combined public sector borrowing remains elevated. Without coordinated adjustment, central restraint risks being offset elsewhere. The budget does not directly confront this risk, preferring to rely on overall macro stability and shared growth dividends.

Consolidation as political economy

The deeper story of Budget 2026–27 is not austerity but sequencing. The finance ministry is attempting to normalise fiscal policy without provoking political or market backlash. That requires patience and favourable macro conditions. It also requires credibility—something the government believes it has earned through steady, if unspectacular, deficit reduction since the pandemic.

Prime Minister Narendra Modi’s government frames this as proof of reform over rhetoric. Critics will argue that consolidation remains too slow and too dependent on optimistic growth assumptions. Both views have merit. What cannot be ignored is that the budget reflects the limits of fiscal policy in the current cycle. Ambition is present, but it is tightly bounded.

The attempt at consolidation in 2026–27 is therefore best seen as defensive competence rather than transformative reform. It holds the line, reassures creditors, and avoids destabilising shocks. Whether that will be enough if global or domestic conditions turn adverse is a question the budget leaves unanswered.