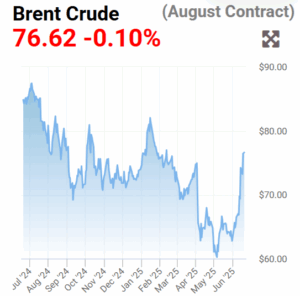

For years, economists have worried about sluggish demand, not scarce supply. That complacency ended the moment Israel and Iran exchanged missiles. In a flash, Brent crude climbed past $75 a barrel and traders braced for a sprint to three-digit territory if a single rocket shuts the Strait of Hormuz—the world’s narrow, nerve-fraying oil artery. Ships are already hugging safer waters, and marine insurers have quietly doubled their war-risk premia. Suddenly the ghost of the 1973 embargo is striding across trading floors from Singapore to Chicago.

Oil is the first casualty, not the last. About a third of global container traffic relies on Red Sea and Gulf routes; diverting around the Cape of Good Hope adds two weeks and a mountain of extra fuel costs. In the skies, matters are no better. Airspace over Iran, Iraq and Jordan—the aerial bridge between Asia and Europe—shut within hours of the first Israeli strike, forcing carriers such as Emirates, Etihad and Qatar Airways onto circuitous detours. Every fresh nautical mile and every extra tonne of jet fuel push up freight bills and, soon enough, retail prices.

READ I Liberating urban governance from middlemen networks

Israel-Iran war and the stagflation threat

Supply shocks breed the cruellest dilemma: inflation climbs even as output sinks. Britain’s headline inflation had eased to 3.4 per cent in May, but fresh energy jolts threaten to undo two painful years of monetary tightening. The European Central Bank and the US Federal Reserve face the same trap: cut rates and risk validating higher prices, raise them and crush economies already limping under tariffs and weak investment.

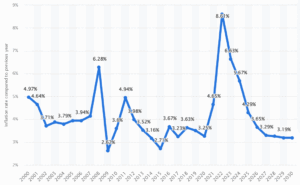

Global annual inflation rate and projections (%)

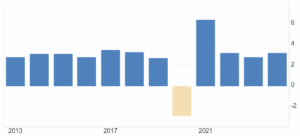

Global annual GDP growth rate (%)

Fiscal numbers are bleaker still. Israel’s war outlay—an estimated $725 million a day—could balloon its 2025 deficit beyond six per cent of GDP. Iran’s revenues wobble on pipelines that might themselves become targets. Eventually, the bill lands on households as higher taxes or costlier credit.

Equity indices have not collapsed—yet. The S&P 500 sits scarcely one per cent below its pre-war level, a tribute to algorithmic optimism and the hope that geopolitics blows over quickly. But the 1973 experience cautions otherwise: Wall Street needed six years to recoup its losses after that energy shock. Investors have noticed. Options linked to geopolitical risk are getting pricier, gold flirts with its April record near $3,500 an ounce, and money is stampeding into low-yield sovereign bonds.

India’s double vulnerability

No economy illustrates the bind better than India. We import 85 per cent of our crude, most of it through Hormuz. Every ten-dollar rise in oil adds roughly $15 billion to our import bill and widens the current-account deficit by 0.3 percentage points. The Reserve Bank’s hard-won inflation glide path—CPI at 4.5 per cent for 2025-26—cannot survive a sustained oil spike. Nor can rural households that depend on subsidised LPG cylinders or truckers who haul produce on diesel.

The irony deepens. India also exports about $1.4 billion worth of basmati rice to Iran; any payments freeze or shipping blockade will hurt farmers in Haryana and Punjab. A war thousands of kilometres away can scorch our fields and kitchen stoves alike.

Meeting in Bari, G7 leaders issued the usual communiqués praising Israel’s “right to self-defence” and calling Iran a “source of instability.” Fine words—but investors noticed what was missing: an energy plan. There was no emergency reserve release, no pledge to police sea-lanes, no hint of reviving the moribund Iran nuclear deal. Without a diplomatic off-ramp, markets are left with prayer, and prayer is no hedge.

What ought to be done

The United States, European Union and Gulf states should broker a narrow maritime accord—call it “Hormuz Safe Passage”—guaranteeing civilian shipping under neutral escort. China, the largest buyer of Iranian crude, and India, one of the largest consumers, have every incentive to join. If the combatants know that choking commerce will trigger multilateral naval patrols, they may think twice.

The IMF and World Bank must ready a rapid-disbursement window for oil-importing developing countries. The pandemic-era Rapid Financing Instrument saved cash-starved economies; a similar facility can soften the blow of an oil spike on budgets from Colombo to Cairo.

Central banks should signal that any rate rises will be surgical and temporary, aimed squarely at anchoring expectations. Meanwhile, governments can cushion the poor with time-bound fuel subsidies funded by windfall levies on defence stocks and energy majors now minting extraordinary profits.

Iran’s nuclear programme is the molten core of this crisis. The 2015 accord was imperfect, but while it lasted, Tehran shipped out 97 per cent of its enriched uranium. A fresh pact—this time with buy-in from China, Russia and the Gulf—could exchange rigorous inspections for phased sanctions relief. Diplomacy costs less than blockade; verification less than bombardment.

Energy is the world’s ultimate general-purpose input; disturb it and every ledger, every livelihood, quivers. The Israel-Iran war raises costs, reroutes trade, rattles markets and corners central banks. It spares neither creditor nor debtor, importer nor exporter. History warns that supply shocks burn longer than demand shocks and leave deeper scars. Unless statesmanship intervenes, we risk repeating an unforgiving arithmetic: stagflation plus strategic paralysis equals lost years of growth.

Peace may demand patience and painful compromise. War is already charging us at the petrol pump. The longer the cannons roar, the louder the cash registers will scream.