RBI rate cut: The central question before the RBI Monetary Policy Committee ahead of December 5 is whether policy should remain restrictive when inflation has fallen below target and growth impulses show signs of fatigue. The evidence shows that monetary conditions have stayed tight for over a year, even as the inflation outlook has softened. A calibrated 25basis point cut is consistent with both flexible inflation targeting and the need to support demand at a time of slowing momentum.

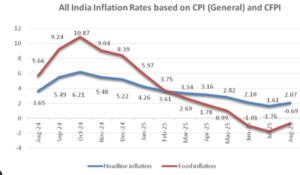

Headline CPI eased to 4.9% in October, well below the upper tolerance band, while core inflation remains subdued at multi-year lows. The RBI has consistently over-forecast inflation since mid-2024, revising projections lower each quarter. On the other hand, ex-post real rates have hovered above 2%, a level historically associated with lower output growth. Research from the BIS confirms that real rates of this magnitude tend to depress demand in emerging markets.

READ | India-Russia tourism pact can balance skewed trade ties

Growth at 8.2% in Q2 FY26 suggests resilience, yet inflation below target implies the economy is operating below potential. Most independent estimates place India’s potential growth well above 6%, including the IMF’s latest World Economic Outlook. The argument, therefore, centres on whether policy should continue in a precautionary “wait-and-see” mode when there is no evidence of overheating, and when monetary policy acts with a lag.

Tight monetary setting risks slowing demand

The policy concern is the emerging signs of softening activity. Core industry growth has eased, and urban unemployment has risen to 7% (CMIE). Exports have slowed, reflecting both weak global demand and the absence of progress on a bilateral trade arrangement with the US. The October boost in GST collections has not been sustained.

Real interest rates have impaired demand for more than a year. Repo at 6.50% alongside inflation below 5% keeps real borrowing costs high for households and firms. Both CPI and WPI inflation remain subdued, with the wholesale index close to zero. With corporate revenue growth slipping into single digits, interest costs will claim a larger share of earnings. High real rates risk pulling back the revival in credit growth visible since Q1.

The evidence also shows that the change to a “neutral” stance with hawkish communication has obstructed financial transmission. Ten-year G-sec yields rose to 6.57% in late October, limiting banks’ incentive to cut lending rates. Recent softening to near 6.51% followed only after the RBI declined auction bids and signalled policy space. A policy cut, communicated clearly, would restore the credibility of data-dependent easing within a neutral stance.

RBI rate cut: Inflation risks have receded

The argument for easing rests on the demonstrated capacity of post-pandemic policy to absorb external shocks. Food inflation management has improved through proactive buffer releases and import actions. The global disinflation cycle is progressing; several major central banks have shifted to easing or signalled imminent cuts. Oil prices remain contained, and the supply of Russian crude continues at discounted rates.

Domestic indicators suggest slack. Spare capacity in several sectors remains visible. Household financial savings have increased, expanding the pool available for credit intermediation. Bank profitability remains healthy despite earlier rate cuts, reducing institutional resistance to pass-through.

Growth of 8.2% in Q2 is encouraging, particularly the momentum in private consumption, which expanded 7.9%, and investment, which grew 7.3% (NSO). Yet nominal GDP growth is subdued at 8.7%, complicating fiscal consolidation. A moderate easing would support demand without jeopardising price stability. The inflation outlook for the next four quarters remains benign according to the RBI’s own household expectations survey and forward projections.

Liquidity needs calibrated easing

Liquidity conditions have tightened due to sustained foreign exchange interventions. System liquidity is slipping into deficit, creating friction for credit offtake. Open Market Operation (OMO) purchases can provide targeted liquidity without amplifying inflation risks. Several analysts argue the RBI should combine a rate cut with incremental liquidity infusion to prevent an abrupt tightening of financial conditions.

The external sector also warrants coordinated fiscal and monetary support. The trade deficit has widened and the rupee has come under pressure from uncertainty around US tariff actions. Maintaining restrictive real rates in this environment may push more burden on fiscal policy, risking higher bond yields.

The evidence supports a 25-basis-point cut in the repo rate. The stance should remain neutral, but communication must underline the possibility of further easing if data confirms a durable low-inflation path. Such an approach balances inflation credibility with the need to protect growth.

A rate cut now would reduce the growth sacrifice ratio, revive transmission by anchoring market expectations, and signal that policy remains data-driven rather than biased toward precautionary tightening. With inflation below target, real rates elevated, and growth facing emerging headwinds, the case for a measured cut is both prudent and responsible.