The recent disruption across India’s aviation network has shown how concentrated infrastructure markets can magnify operational shocks. IndiGo, which accounts for more than 60% of domestic air traffic, saw its on-time performance collapse to 8.5%. More than a thousand daily cancellations left passengers stranded, fares spiked, and government intervention became necessary. What began as a firm-level setback quickly became a nationwide mobility challenge.

The Indigo crisis matters for a broader reason. India’s key infrastructure sectors — aviation, telecom, ports and mining — have steadily moved towards monopolies, duopolies or tight oligopolies. Policy has encouraged consolidation to build globally competitive firms. The question now is whether the country has created markets that function smoothly during stress. The IndiGo meltdown shows that efficiency in calm periods is not the same as resilience in turbulent ones.

READ I GDP deflator warning: How did the nominal growth weaken

India’s preference of national champions

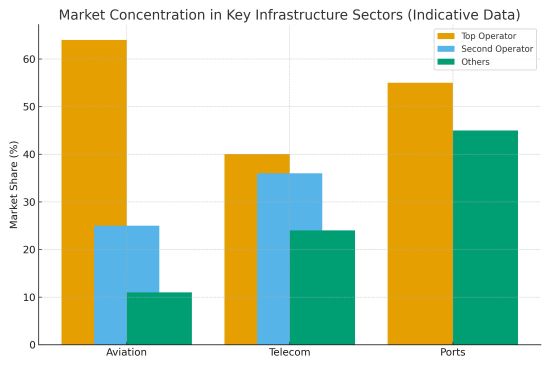

A central feature of the NDA government’s industrial strategy over the past decade has been consolidation. Its key decision makers believe that fragmented sectors cannot attract capital or compete internationally. The result is clear across infrastructure. Two airlines carry more than 90% of domestic passengers. Three telecom operators serve almost the entire market. A small number of conglomerates dominate ports and logistics. Mining blocks increasingly go to large balance-sheet firms.

This strategy has delivered some benefits—higher investment, faster execution, and improved asset quality in several sectors. However, consolidation has also narrowed the competitive field. When a single firm handles a disproportionate share of national capacity, operational risk becomes systemic risk. The IndiGo crisis demonstrates how quickly such concentration can affect the wider economy.

Indigo crisis reveals system fragility

India’s aviation market is now one of the most concentrated among major economies. IndiGo controls a large majority of traffic. The Air India group accounts for most of the rest. Smaller carriers have limited fleets and thin networks. With little spare capacity elsewhere, a disruption at one dominant airline has widespread consequences.

The Indigo crisis, triggered by flight cancellations, illustrates this point. The causes—stricter pilot duty norms, scheduled software upgrades on A320 aircraft and winter fog—were not unexpected. But the market had limited redundancy to absorb the shock. Fares surged six- to seven-fold on some routes, according to travel agents. Long queues, multi-hour delays and last-minute cancellations had knock-on effects across business schedules, logistics chains and household decisions.

The regulatory system struggled to keep pace. DGCA’s technical and supervisory capacity has not expanded proportionately with rising passenger volumes. India now handles more than 150 million domestic flyers every year, yet oversight remains thin. The absence of differentiated rules for systemically important airlines is a critical gap. Infrastructure markets require buffers that go beyond standard commercial norms.

Telecom shows similar patterns. After a period of intense price competition and subsequent consolidation, three operators now control almost the entire subscriber base. One of them continues to face financial uncertainty. Consumers may benefit from lower tariffs, but the sector also exhibits new vulnerabilities—network outages affecting millions simultaneously or limited pressure for service quality improvements in rural areas. India’s ports are a starker example where two conglomerates run a large share of port capacity. Mining and energy sectors also display similar trends.

In each of these sectors, concentration has improved scale economics but also increased dependence on a few operators. A shock at the firm level can easily turn into a macroeconomic disturbance.

Indigo crisis exposes information gaps

The IndiGo crisis exposed another institutional weakness: information asymmetry. Airline apps continued to show flights as “on time” even as airport displays showed lengthy delays. Passengers made decisions based on inaccurate data, incurring costs that could not be recovered through compensation. In infrastructure sectors, information is not merely a consumer-service feature. It is a production input that affects labour mobility, business schedules and supply chains.

Other sectors have similar problems. Telecom users often report unpredictable data speeds. Port users face opaque scheduling information. Electricity consumers encounter sudden tariff changes when distribution companies disclose costs with long delays. These are symptoms of regulatory frameworks that emphasise redress after failure rather than prevention through improved transparency.

India’s regulators need to move from reactive compensation-based models to proactive information-governance frameworks, especially in markets where concentration limits consumer choice.

Regulatory capacity and systemic importance

The broader policy question is whether the Indian state has built regulatory capacity at the same pace as market consolidation. In advanced economies, sectors dominated by a few players typically come with strong antitrust enforcement, detailed continuity plans, clear disclosure norms and robust digital monitoring systems. India’s institutional structure is not yet comparable.

Consider the aviation episode. The ministry intervened only after several days of disruption. The absence of early warnings, readiness audits and system-wide contingency planning highlighted the limits of current oversight. Similar gaps exist in other infrastructure regulators—whether in staffing, data analytics capabilities or enforcement autonomy.

One way forward is to classify large operators as systemically important infrastructure institutions, similar to the financial sector’s treatment of large banks. Such entities would face stricter requirements for operational continuity, transparency, staffing thresholds and real-time information disclosure.

The IndiGo crisis is more than an operational accident. It shines a light on a structural issue across Indian infrastructure: high concentration without matching regulatory depth. Consolidation has created strong national champions, but it has also increased the fragility of essential networks. Efficiency during stable periods is only one measure of success. The test of any market design is how it handles stress.

Policy now needs to address this imbalance. Regulators must be strengthened. Transparency requirements should be modernised. Systemically important operators should face higher resilience obligations. As India expands its infrastructure capacity and builds global-scale firms, the institutional framework governing them must evolve as well. Without such reforms, operational failures will continue to impose large economic and social costs.