India is preparing a sweeping overhaul of its income tax framework, aimed at simplifying compliance for millions of taxpayers. The Lok Sabha has passed two key legislations — the Income Tax Bill, 2025 and the Taxation Laws (Amendment) Bill, 2025 — which together replace the six-decade-old Income Tax Act, 1961, and amend related provisions in the Finance Act, 2025. The new regime will take effect from April 1, 2026.

Finance minister Nirmala Sitharaman, introducing the Bill in the Rajya Sabha, called it a landmark reform to make the law easier to read, interpret, and implement. Without altering tax rates, the income tax bill strips away redundant provisions and outdated terminology. The number of sections is cut from 819 to 536, chapters from 47 to 23, and word count from 5.12 lakh to 2.6 lakh. Clarity is aided by 39 new tables and 40 formulas. A notable change is the adoption of a uniform “tax year” — a 12-month period starting April 1 — aligning India’s system with global best practices.

READ I Student suicides reveal a broken education system

Income tax bill offers relief for Individuals

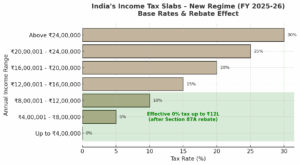

The new regime retains a basic exemption of ₹12 lakh, with a standard deduction of ₹75,000, effectively lifting the zero-tax threshold to ₹12.75 lakh. The slab structure starts with nil tax up to ₹4 lakh, rising to 30% for income above ₹24 lakh. Financial planners expect these changes to benefit middle-income earners, especially those in the ₹8–15 lakh bracket.

The income tax bill removes a restrictive clause from an earlier draft that denied refunds on returns filed after the due date. Now, even belated filers can claim refunds, reducing hardship. In a further easing measure, no Tax Collection at Source (TCS) will apply to education-related overseas remittances under the Liberalised Remittance Scheme when financed through approved institutions.

Corporate and compliance changes

For companies, the income tax bill corrects anomalies in inter-corporate dividend deductions for those under concessional tax rates. It also aligns the Alternate Minimum Tax for Limited Liability Partnerships with the existing law, lowering the rate from 18.5% to 12.5%. Taxpayers with no liability can obtain nil-TDS certificates, reducing procedural delays.

Ambiguities in transfer pricing rules and carry-forward of losses have been addressed. The Bill also clarifies that house property income will carry a standard 30% deduction after municipal taxes. For non-profits, exemptions can now cover up to 5% of total donations, not just anonymous contributions.

The income tax bill retains a contentious clause defining “virtual digital space,” allowing tax authorities to access digital data, including email servers and social media accounts, during surveys and searches. To address privacy concerns, the government will issue a standard operating procedure to safeguard personal data.

Complementary amendments

The Taxation Laws (Amendment) Bill introduces targeted changes to the existing Act and the Finance Act, 2025. It exempts income from dividends, interest, and long-term capital gains for Saudi Arabia’s Public Investment Fund and its subsidiaries — a move to resolve constraints arising from a 2022 notification.

It also extends National Pension System tax benefits to the Unified Pension Scheme, allowing tax-free withdrawals of up to 60% of the corpus at retirement. Amendments to the block assessment scheme in search cases aim to bring greater clarity and efficiency to investigations.

Impact on taxpayers

For salaried individuals and small business owners, the simpler structure should reduce reliance on tax consultants. Refund eligibility for late filers and the nil-TCS provision on education remittances will ease financial strain. Retirees will benefit from higher tax-free pension withdrawals, offering better post-retirement security.

The absence of new tax rates signals the government’s intent to avoid additional burdens at a time when households are still recovering from pandemic-era disruptions.

The twin bills mark the most significant modernisation of India’s tax laws in decades. While welcomed for clarity and relief measures, concerns linger over expanded enforcement powers and potential misuse of digital access provisions. With Presidential assent pending, the government expects phased implementation from the next financial year — ushering in what it terms a “clearer, simpler, and fairer” era in tax administration.