Affordable housing: Roti, kapda, makan may define the Indian dream, but even this basic triad has slipped out of reach for millions of households. Urban home ownership is becoming harder, not easier, despite rising incomes and multiple government schemes. The mismatch between policy intent and market outcomes has become sharper as the Delhi Development Authority’s latest offerings stand out against a nationwide collapse in low-cost housing.

The new Jan Sadharan Awaas Yojana 2025 shows what public-sector intervention can achieve in a market skewed toward mid and high-end projects. The scheme offers legal, serviced and transparent access to homes at prices far below market rates. The broader question is whether this model can be replicated across India’s major cities, or whether Delhi will remain an exception in a market that is moving rapidly out of the reach of lower and middle-income buyers.

READ | Why states miss their capital expenditure targets

DDA’s low-cost push highlights a vanishing market

DDA’s latest release of 1,537 flats across Narela, Rohini, Ramgarh Colony and Moti Nagar provides a rare supply of formal low-cost housing. Narela alone offers 1,120 EWS units priced between ₹11.8–11.9 lakh, with booking amounts of ₹50,000 for EWS and ₹1 lakh for LIG applicants. The eligibility norms widen access, and the allotment process remains transparent.

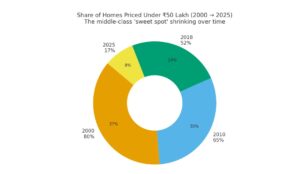

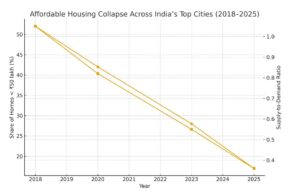

But Delhi is the outlier. Across India’s top eight cities, the supply-to-demand ratio for affordable housing fell to 0.36 in 2025, down from 1.05 in 2019, according to Knight Frank India. The share of homes priced below ₹50 lakh has collapsed from 52% in 2018 to 17% in 2025. This erosion has shut out first-time buyers, even as urbanisation accelerates.

Why developers are exiting affordable housing

Costs have risen across the housing value chain. Land prices are elevated. Construction costs have increased between 8–12% annually, as shown in the RBI’s construction cost index. Developers prefer mid and premium projects where margins are higher and sales cycles shorter. Affordable buyers have limited repayment capacity, which slows project cash flows.

Financing gaps deepen the problem. NBFCs and housing finance companies hesitate to lend for low-ticket homes. Banks meet their priority-sector targets faster through large-ticket mortgages. Smaller developers who once built affordable units find credit hard to secure. The result is a structural imbalance—surging demand at the bottom of the pyramid and shrinking supply.

Rental housing: India’s missing pressure valve

India’s rental housing market should have acted as a buffer for lower-income households, but it remains underdeveloped. The Model Tenancy Act (MTA), designed to formalise rentals and protect both landlords and tenants, has seen limited adoption. Most states have not implemented it, leaving rental contracts informal and poorly regulated.

Formal rental stock remains scarce. With weak rental supply and high insecurity around tenure, more households feel pressure to buy even when ownership is unaffordable. This adds stress to the very segment of the market where supply is collapsing. Without a functioning rental ecosystem, affordable home ownership becomes the only viable option for millions—tightening the squeeze on demand.

Land-use and zoning: The core policy constraint

Weak land management and restrictive zoning limit the ability of Indian cities to scale affordable housing. Floor Area Ratio (FAR/FSI) remains low in most metropolitan regions. Height restrictions, fragmented approvals, and inconsistent zoning rules create friction in adding low-cost stock. Much of urban land remains locked in low-density uses, including institutional and single-family zones.

DDA’s advantage stems from decades of planning that retained large, contiguous public land parcels. Most cities do not have this luxury. Without higher FAR, predictable zoning, and digitised land records, no city can replicate Delhi’s scale in EWS and LIG units. The constraint is not only money. It is land, and how cities choose to use it.

The impact of CLSS withdrawal on demand

The end of the Credit Linked Subsidy Scheme (CLSS) under PMAY–Urban in 2022 removed a critical incentive for first-time homebuyers. CLSS lowered effective interest rates for EWS, LIG and MIG buyers. With its withdrawal, monthly mortgage outflows increased sharply, reducing affordability and weakening demand precisely at the lower end where the market needed support.

This change matters. Fewer households now qualify for credit, and EMIs have risen in a period of higher interest rates. Combined with rising prices, the end of CLSS has pushed many aspiring buyers back into overcrowded rentals or informal settlements.

Demographic and migration pressures intensify demand

Urbanisation continues to push millions into cities each year. NSSO and UN-Habitat projections show that India will add 400 million new urban residents by 2050. Much of this growth will be driven by younger workers entering the labour force and migrating from rural areas in search of jobs. This demographic bulge fuels demand for housing at the lower end of the market.

When affordable units shrink and rental options remain weak, migrants turn to informal settlements. The strain is visible in expanding peri-urban slums, overcrowded transport corridors, and rising pressure on public services. The housing shortage is therefore not just an economic issue. It is a demographic one.

Growing role of informal and slum housing

As formal supply tightens, informal housing expands. Mumbai’s slum population continues to hover near 40% of its residents. Delhi, Bengaluru and Kolkata show similar patterns. Low-income households turn to informal colonies for proximity to jobs, flexible rents and low upfront costs. Regularisation drives temporarily improve tenure security but do not add new formal stock.

This growth of informal housing underlines the affordability deficit. Without serviced plots, regulated rentals and affordable ownership at scale, slums fill the gap. They are a symptom of structural scarcity, not a cause.

Replicating the DDA model needs land, planning

The DDA model rests on four foundations: public land, below-market pricing, legal clarity, and transparent allotment. These elements keep prices low without burdening the state exchequer. For many families, a ₹12–13 lakh EWS flat remains the only viable path into Delhi’s formal housing market.

But scaling this model requires land pooling, stronger planning institutions and empowered urban development authorities. States such as Gujarat, Tamil Nadu and Maharashtra have tried variations, but supply remains far below demand. PMAY–Urban, despite sanctioning over one crore homes, has not created enough formal urban apartments because most units were self-built in peri-urban plots.

India needs a national public-land strategy

India’s housing shortage will deepen unless cities rethink how land is planned, zoned and utilised. The fall in homes priced under ₹50 lakh is a structural market failure. Private incentives cannot close this gap. Public-sector housing will have to expand, especially in large metros where land markets favour high-end projects.

Cities need clear land pooling frameworks, integrated transport planning and higher FAR to support multi-storey affordable housing. Credit guarantees for low-ticket loans, viability-gap funding and incentives for small developers can rebuild supply. A national public-land strategy is now essential.

DDA’s 2025 initiative shows what is possible when land access, transparent governance and public purpose converge. Without similar interventions across India’s major cities, urban home ownership risks becoming an elite privilege—closing the ladder of upward mobility that shaped India’s middle class.