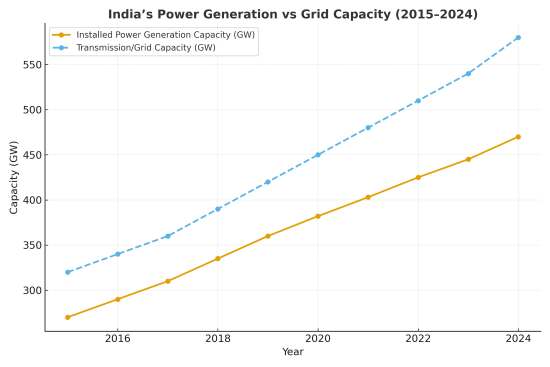

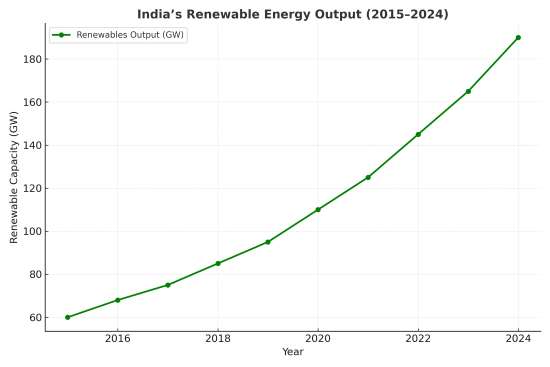

India is surging ahead in renewable-energy capacity, aiming for 500 GW of non-fossil fuel generation by 2030 under the Central Electricity Authority plan. Despite the headline numbers, roughly 50 GW of renewable installations remain stranded as of June 2025, unable to be evacuated reliably into the power grid. At the same time the transmission network build out is lagging: the CEA envisages adding some 191,000 circuit-kilometres of lines by FY2032 at an estimated investment of ₹9.15 trillion. The question for India now is whether policy can shift emphatically from megawatts of capacity to megawatt-hours of delivered clean power.

The technical and institutional mismatch is plain. A utility scale solar or wind plant can often be built in 12-18 months. By contrast, the associated transmission lines — especially inter-state high‐voltage corridors — take 3-5 years to plan, clear land, obtain environmental approvals and commission. The CEA’s “Transmission System for integration of over 500 GW RE” document spells out this challenge and lays the groundwork for 500 GW non-fossil capacity by 2030. Worse still, transmission performance is stalling: in FY2025 only 8,830 circuit-kilometres of new lines were added, versus a target of 15,253 ckm — ie a shortfall of 42 %. And up to 71 % of Inter‐State Transmission System (ISTS) corridors are reportedly operating below 30 % utilisation.

Some states capture the scale of the problem. For example, in Rajasthan, 8 GW of RE capacity remains stranded, with nearly half subject to curtailment because the Associated Transmission System is delayed and ecological mandates—such as underground cabling to protect the Great Indian Bustard—are adding cost and time. Centre–state segmentation exacerbates this: while the CEA and the Central Transmission Utility of India Ltd (CTUIL) lay out broad national plans, state transmission utilities still handle right-of-way (RoW) and land / clearance issues. These split responsibilities slow execution. The result: capacity may be ready, but electrons can’t flow.

READ I India-US mini trade deal: Relief with hidden risks

Market design and regulatory frictions

Despite policy incentives, market design and regulatory frictions hamper delivery. For instance, the Inter-State Transmission System (ISTS) charges waiver—originally extended for solar and wind until 30 June 2025—reduces one cost barrier, and the exemption for battery and pumped storage projects has been extended to 30 June 2028. But a waiver is only useful if transmission capacity and grid access are timely. Banking norms, deviation settlement and curtailment risk feed into tariff bids: developers build a capacity but face commercial risk if they cannot dispatch. The lack of transparent curtailment protocols and the phenomenon of “connectivity hoarding” (where some entities reserve grid access but do not proceed to generate) raise access costs for legitimate projects.

On the storage front, the Solar Energy Corporation of India (SECI) has issued tenders for firm & dispatchable renewable energy (RE) plus storage, signalling the shift from mere capacity to firm megawatt-hour delivery. Without synchronous build-out of lines and storage that can absorb evening/seasonal deficits, auctions can still produce bids that undervalue power grid risk. Until grid visibility is better, tariff compression may reverse.

Financing the power grid

The size of the cheque for transmission is substantial. The CEA’s National Electricity Plan reckons India will need roughly ₹9.15 trillion (~US$110 billion) to build 191,000 ckm of new lines by FY2032. This is over and above generation capex. Execution capacity lies with state utilities, the central public entity Power Grid Corporation of India (POWERGRID), and a growing private T&D sector.

The model of tariff-based competitive bidding (TBCB) for transmission has been brought in, enabling private investment and asset-monetisation. But the risk profile is elevated: states already carry stressed balance-sheets, shifting large power grid capex onto them may affect their credit ratings and increase cost of capital.

Private T&D players are entering, but regulatory certainty, predictable returns and timely RoW remain key. The longer the delay in transmission, the higher the per-unit cost of evacuated RE and the greater the risk of stranded generation assets.

Firming power: Hydro and storage as the hinge

Bridging the gap between installed capacity and delivered power requires firming—both daily and seasonally. Accordingly, the government and the CEA have placed emphasis on pumped hydro storage (PHS) and large hydro-power plus evacuation from the eastern and north-eastern regions. A transmission master-plan flagged 76 GW of hydro and PHS potential in the Brahmaputra basin, with an estimated investment of ₹6.4 trillion.

These assets matter not just for balancing solar/wind variability but for linking renewable-rich states in the west/northwest with demand centres elsewhere via strong corridors. Furthermore, the ISTS waiver extension for co-located battery energy storage systems (BESS) to June 2028 gives a window for integrating storage into transmission planning. But until such storage and hydro assets are paired with timely grid build-out, the risk is that India may inadvertently bottleneck clean power and revert to higher coal reliance during peak or evening times.

The renewables policy imperatives

To shift from MW to MWh delivered, India must focus on three practical moves.

Time-linked joint planning: Mandate coordinated planning between CEA, CTUIL and state utilities with enforceable milestone tracking, so generation and transmission proceed in lockstep rather than sequentially.

De-risking access: Introduce congestion-priced access and transparent curtailment protocols so developers bid with power grid risk priced, not hidden. Banking and deviation settlement must be harmonised nationally.

Grid-first renewable clusters: Prioritise transmission build-out for key RE clusters (eg Rajasthan–Gujarat–Tamil Nadu) with viability-gap support, fast clearances and dedicated corridors for evacuation.

India’s clean-energy story has reached a critical inflection point. The country has proven that it can attract investment, execute projects, and add renewable capacity at scale. What it has not yet proven is the ability to deliver that clean power reliably and affordably across the power grid. The next phase of the transition will therefore be judged less by how many gigawatts are tendered or commissioned, and more by how many megawatt-hours are transmitted and consumed.

Grid synchronisation, firming capacity, and market design will determine whether India stays the course on its 500 GW by 2030 target or slips back into coal dependency to meet evening peaks. The lesson from other large systems—from China’s ultra-high-voltage corridors to Europe’s cross-border balancing markets—is that integration, not generation, defines credibility.

India must now treat transmission as the new frontier of energy reform: a shared national infrastructure that underwrites both growth and climate goals. Only when clean power flows as smoothly as it is built will the promise of a green grid translate into real economic resilience and lower-carbon prosperity.