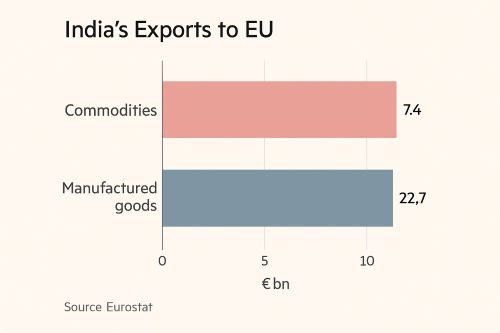

The India-EU FTA has entered a decisive phase as negotiators confront the European Union’s tightening Carbon Border Adjustment Mechanism, which moves into full effect from 2026. The EU is already India’s second-largest export destination, accounting for nearly 15% of total merchandise shipments. The CBAM regime will impose a carbon-based levy on imports of steel, aluminium, cement, fertilisers, hydrogen, and electricity, based on verified embedded emissions.

The issue matters now because the EU is integrating CBAM into its wider industrial decarbonisation plan under the European Green Deal, signalling that trade partners must align or risk losing competitiveness. The argument centres on a structural challenge: India’s export sectors face rising compliance costs unless domestic decarbonisation, carbon accounting systems, and energy-transition investments advance at a faster pace.

READ I Rupee depreciation: The real drivers of India’s currency fall

CBAM will reshape India’s cost competitiveness

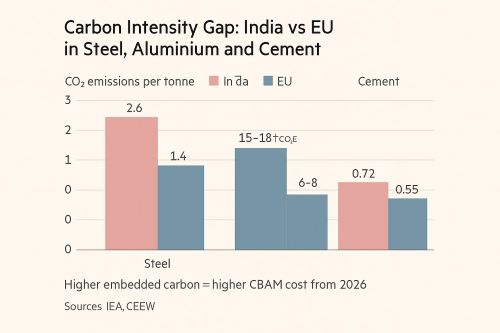

The evidence shows that CBAM will directly affect India’s steel, aluminium, and cement exports, which have some of the highest emissions intensities among major producers. According to the IEA, India’s blast-furnace steel emits around 2.6 tonnes of CO₂ per tonne of crude steel, compared with 1.4 tonnes in the EU. This gap is central to the cost burden CBAM will impose. Once the transitional phase ends in 2026, exporters will need to purchase CBAM certificates aligned with the EU Emissions Trading System (ETS) price, which has ranged between €60–€90 per tonne in recent years. A steel consignment with high embedded carbon will therefore face a steep tax burden.

Aluminium shows a similar vulnerability. The CEEW estimates that EU-bound Indian aluminium could face an effective carbon cost equal to 12–22% of its export value, driven by coal-based power used in smelting. Cement producers also face exposure because India’s clinker emissions intensity (0.72 tonnes of CO₂ per tonne) exceeds the EU’s benchmark.

The policy concern is that these cost differentials could erase India’s freight-adjusted price advantage. The central question is whether firms can adopt low-carbon pathways fast enough to stay competitive under CBAM’s pricing logic, which treats carbon intensity as a tariff in all but name.

An India-EU FTA may not shield exporters

The argument centres on an uncomfortable reality: a trade agreement cannot neutralise a climate-linked border tax that is explicitly non-negotiable under EU law. The EU has stated that CBAM is a non-tariff, non-preferential measure, meaning FTA concessions do not dilute its impact. India’s hope of securing exemptions through diplomacy therefore has limited scope.

A credible domestic response requires carbon pricing reforms, measurement-reporting-verification (MRV) systems, and accelerated renewable-energy uptake. The Commerce Ministry has emphasised that India will contest discriminatory aspects of CBAM at the WTO. Yet legal action cannot substitute for domestic readiness. Without plant-level MRV systems aligned with EU methodologies, exporters risk being assigned default carbon values, which are significantly higher than actual emissions.

Domestic carbon pricing will also become unavoidable. Whether through an emissions-trading scheme or a shadow carbon price applied via regulatory mandates, exporters need a price signal to plan investments. The current Perform, Achieve and Trade (PAT) scheme has delivered energy savings but does not align with CBAM’s granular emissions accounting.

India’s ongoing renewable-capacity expansion—reaching 190 GW of non-fossil capacity—is a strategic advantage. But energy-intensive sectors require deeper reforms, such as green-hydrogen pathways for steel and low-carbon process heat for cement. Without these, the India-EU FTA cannot compensate for the structural disadvantage created by CBAM.

Implications for MSMEs and carbon-intensive states

The evidence shows that the CBAM impact will not be uniform across India. States such as Odisha, Chhattisgarh, and Jharkhand—core steel and aluminium clusters—will bear disproportionate costs. Odisha alone accounts for over half of India’s aluminium output, much of it powered by captive coal plants. CBAM-linked cost escalations will therefore hit state-level revenues, employment, and investment pipelines.

MSMEs integrated into large-sector supply chains face a sharper challenge. Most cannot independently finance emissions-monitoring infrastructure or procure renewable power at scale. A CEEW analysis indicates that close to 30% of India’s metal-sector MSMEs lack digital systems needed for emissions tracking. Without support, they risk exclusion from export-oriented value chains as large producers tighten sustainability requirements.

Gujarat and Maharashtra, with stronger renewable-energy integration and better port connectivity, may weather the transition more effectively. But even in these states, clusters supplying steel tubes, aluminium extrusions, and metal components will face tighter scrutiny under CBAM’s verification rules. The policy concern is that regional disparities could widen unless national-level mitigation measures accompany the India-EU FTA.

A realistic roadmap post India-EU FTA

The central question is whether the India-EU FTA can align decarbonisation with export competitiveness within the CBAM timeline. A realistic roadmap requires four elements.

First, India needs a unified carbon-accounting framework. Harmonised MRV protocols across steel, cement, aluminium, fertilisers, and hydrogen will allow exporters to present verified emissions data rather than default values. Agencies such as the Bureau of Energy Efficiency and the MoEFCC

should co-develop sectoral methodologies.

Second, India must accelerate access to low-carbon energy. Green hydrogen for primary steelmaking, renewable-energy purchase obligations for smelters, and waste-heat recovery in cement can lower embedded carbon. The evidence shows that green hydrogen costs in India have already fallen to USD 4–5/kg, with potential for further reduction.

Third, targeted cluster-level support is essential for MSMEs. Common emissions-monitoring facilities, renewable-energy procurement pools, and concessional financing through SIDBI can prevent value-chain exclusion.

Fourth, India’s FTA strategy must integrate climate-adjustment financing. The EU’s Global Gateway fund, blended-finance platforms, and technology-transfer frameworks can support decarbonisation of India’s hard-to-abate sectors. The argument centres on aligning trade commitments with industrial-transition requirements so that CBAM becomes a catalyst rather than a barrier.

India’s export prospects in the EU market depend on a clear alignment between FTA negotiations and domestic decarbonisation. The policy concern is not the presence of CBAM but the preparedness of Indian industry to operate under a carbon-priced trade regime. A coordinated roadmap that strengthens MRV systems, accelerates low-carbon energy adoption, and supports MSMEs can minimise disruption.

Harmonising trade strategy with climate-transition investments will allow India to preserve market share while building a more competitive industrial base. The evidence shows that the challenge is significant, but the opportunity is equally so if policies are sequenced with discipline.