Trump tariffs struck down: The US Supreme Court’s 6-3 decision on February 20, striking down President Donald Trump’s sweeping global tariffs is not merely a judicial rebuke. It changes the operating environment for world trade by puncturing the credibility of tariff threats as a durable instrument of US statecraft. The ruling has introduced a layer of uncertainty into global supply chains that had begun pricing in a new US tariff baseline.

The Court held that Trump exceeded his authority by using the International Emergency Economic Powers Act (IEEPA), a statute that does not authorise tariffs, to impose import duties. That legal finding undermines the foundation of several recent deals that were negotiated in the shadow of tariffs. Tariff diplomacy works when counterparties believe the tariff is legally sustainable, and the judgment says it was not.

Trump’s immediate response was to announce a temporary, across-the-board 10% tariff under Section 122 of the Trade Act of 1974, framed as a stopgap for 150 days. Section 122 is both time-limited and historically unused for modern trade bargaining, which is precisely why it fails to restore confidence. It replaces a contested but sweeping instrument with a short fuse and an even larger question: what comes after day 150.

READ I India-US trade framework: The coercion behind concessions

Trade deals under a legal cloud

Many of the administration’s recent understandings with major partners were not traditional trade agreements. They were tariff “ceilings” in exchange for investment pledges, purchase commitments, and selective concessions. Their political logic was clear: convert threat into compliance, then claim wins. The legal fragility of the underlying tariff weapon now forces every counterpart to reassess what, exactly, it agreed to.

Europe offers the clearest illustration. EU business groups have already sought clarity on whether the ruling changes the deal’s practical meaning for firms making investment and sourcing decisions. The point is not whether the tariff rate is 15% or 20%. The point is whether the US can keep it in place without the next court ruling, the next executive workaround, or the next change of administration.

In Asia, the deeper problem is sequencing. Several countries moved manufacturing into Southeast Asia to arbitrage US tariffs on China, only to find that “China-plus-one” itself became a target category. The Court’s ruling provides momentary relief for some producers, but it also increases the risk premium on long-horizon capacity decisions. Firms can handle a bad tariff regime. They struggle with a volatile regime.

READ I India-EU FTA: Carbon rules, value chains, and export strategy

From tariff stacks to tariff roulette

The Trump system relied on stacking. Different legal authorities produced layers of tariffs that could accumulate into a high effective burden for targeted sectors and countries. The Court’s decision peels away an important layer, but the administration’s pivot to other statutes signals that “peeling” may be temporary. The immediate result is not liberalisation. It is tariff roulette.

That matters for global trade because it changes bargaining dynamics. Partners now know the White House may be constrained on one legal track and aggressive on another. They also know that concessions secured under pressure could be reopened, explicitly or implicitly, if the US recalibrates its legal basis for tariffs. That is not a recipe for stable market access. It is a recipe for perpetual renegotiation.

The WTO system was already weakened by unilateralism and retaliation cycles. This episode accelerates a different form of erosion: agreements that are politically binding but legally precarious, backed by threats that can be struck down and replaced in days. For middle powers trying to plan export strategies, the US market begins to resemble a sequence of policy episodes, not a rules-based destination.

READ I India-EU trade deal: CBAM compliance becomes competitiveness

Global economy: Volatility as a tax on investment

The economic cost of Trump tariffs is often debated through price effects and trade diversion. The larger cost here is volatility. Volatility operates like a tax on investment because it raises the option value of waiting. Executives delay plant decisions. Retailers delay long-term sourcing. Financial markets demand a higher risk premium for trade-exposed sectors.

The Supreme Court’s ruling does not eliminate the tariff overhang. It reintroduces it as an institutional contest. Trump has signalled new Section 301 investigations and renewed attention to Section 232-style national security tariffs. These processes can take time, but they also create a pipeline of future tariff shocks.

For emerging markets, the spillovers are straightforward. If the US shifts from broad tariffs to targeted, statute-driven actions, the pattern of winners and losers will change quickly. “Friend-shoring” bets premised on negotiated tariff caps may be revisited. Exporters will demand clearer contractual pass-through clauses. Trade finance will become more conservative. The short-term effect could look like relief in headline rates, while the medium-term effect is tighter conditions for trade-dependent growth.

Trump tariff revenue was never stable revenue

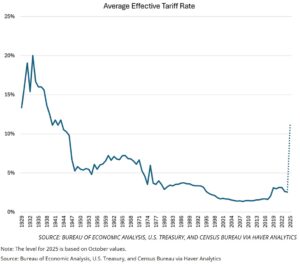

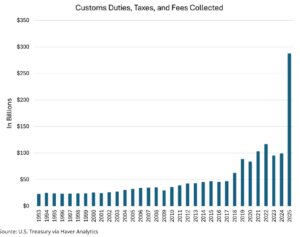

The fiscal implications of Trump tariffs are more concrete than the trade implications, because they involve cash. Analysts estimate that more than $175 billion in tariff collections are at risk of refunds after the ruling, depending on how lower courts and agencies handle claims and procedures.

This is not a technical footnote. Refund exposure of that scale forces the Treasury to plan around cash volatility, even if it believes it can manage balances. It also exposes a deeper problem: the administration treated tariff revenue as a semi-structural offset while pursuing costly tax policy. The Supreme Court has now demonstrated how quickly that offset can evaporate.

Even before the ruling, tariff revenue was a politically reversible stream. It could be reduced by a successor, diluted by exemptions, or bargained away in a deal. Now it is also legally contestable and potentially refundable. A revenue instrument that can be invalidated in one judgment and challenged entry-by-entry is not the foundation on which to build medium-term deficit strategy.

The White House’s answer is to find a replacement for Trump tariffs. Section 122 allows up to 15% for 150 days, with minimal procedural friction, and Trump has presented the new 10% tariff as a fiscal and bargaining bridge. But the bridge is short, and the politics of extending it are unclear. If the administration escalates through other channels, it may recreate revenue at the cost of a larger growth hit. If it does not, the budget hole becomes harder to paper over.

The Congressional Budget Office’s latest outlook already points to large deficits through the coming decade. In that setting, the tariff episode is a warning about fiscal improvisation: executive-driven revenue is easier to announce than to defend, easier to collect than to keep, and easier to model than to rely on.

Institutions now shape tariffs

The Supreme Court decision to strike down Trump tariffs is being read as a constraint on presidential power. In economic terms, it is also a constraint on the credibility of tariff strategy. If tariffs are to be used as long-term instruments, they must sit on statutes that survive judicial scrutiny and political turnover. Otherwise, they will produce a cycle: threat, deal, litigation, refund risk, workaround, and renewed threat.

For global trade, that cycle is corrosive. It turns market access into a contingent outcome of US domestic legal battles. For the global economy, it elevates uncertainty to a first-order macro variable. For the US budget, it exposes the temptation to treat volatile trade taxes as dependable revenue.

The ruling may reduce the effective tariff burden briefly. It does not reduce the central problem. The problem is a US trade regime that is now openly experimental, legally contested, and fiscally entangled.