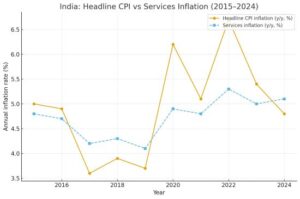

India’s retail inflation appears unusually benign. Headline CPI inflation fell to 0.25% in October 2025, pulled down by a sharp 5 per cent contraction in food prices and a broad cooling across goods categories. Rural inflation dipped into negative territory, while urban inflation remained moderate at about 2 per cent. On the surface, the data signals the strongest disinflation Indian households have seen in years.

Yet the broader inflation trend looks less benign once the spotlight moves beyond cereals and vegetables. India is witnessing a clear shift: services inflation is rising even as goods deflate. Housing inflation remains close to 3 per cent and health inflation is approaching 4 per cent. Education, personal care, logistics, domestic services and digital services all show persistent price increases. The headline number has never been less representative of the economy beneath it.

READ I India’s critical minerals push needs a midstream reset

Services inflation is rising

The divergence between goods and services is widening because these two parts of the economy respond differently to supply conditions. Goods prices are adjusting quickly to improved harvests, lower commodity prices and better global availability. Services prices are not. Sectors such as healthcare, education, transport, hospitality, beauty services, repair services and household support continue to record steady increases.

This reflects a deeper transition in India’s price structure. Services now account for a majority of India’s GDP and a rising share of consumption in urban households. When food prices fall, the impact is immediate and visible. But when rents inch up, or when childcare, diagnostics or commute costs rise, the pressure feels continuous. The October CPI print therefore captures only one half of India’s inflation reality.

What is driving the rise in services inflation

The firmness of services inflation stems from both structural and cyclical factors. Wage costs in the services economy have been rising, especially in hospitality, logistics, retail and personal care. These sectors rely heavily on physical labour, making efficient substitution or automation difficult. A rise in wages slips quickly into final prices.

Higher compliance costs are another source of inflationary pressure. The rollout of GST 2.0, wider e-invoicing norms, state-level fees and local reporting requirements have increased the administrative load on small service firms. Unlike manufacturing, these firms seldom have the scale to absorb compliance expenses, so those costs end up embedded in final prices.

Urban rentals remain firm as well. Clinics, coaching centres, small restaurants, salons, warehouses and logistics hubs face steadily rising rents in most cities. These fixed costs make service prices sticky even when input costs fall elsewhere. Transport and energy costs reinforce these pressures. Fuel prices may move within narrow bands, but electricity, refrigeration and local transport remain cost-heavy for service providers. A restaurant, pharmacy, early-childhood centre or small logistics player cannot easily compress such costs.

The shift in household consumption patterns adds to this structural firmness. Indian families today spend more on services—digital subscriptions, app-based delivery, after-school learning, diagnostics, preventive healthcare, fitness, financial services and travel. These categories are not only expanding; their prices tend to adjust slowly and almost never move downward. A family that sees relief at the vegetable market may still find its monthly bills unchanged or higher because the essential services it uses have become costlier.

Why services inflation matters for policy choices

The rising prominence of services inflation complicates India’s monetary policy environment. For decades, the CPI index was driven largely by food and fuel, and headline inflation was a reliable signal for interest-rate decisions. That assumption is breaking down. A headline inflation print of 0.25% might suggest room for policy easing, but underlying services inflation paints a different picture. If policymakers respond only to the headline number, they risk stimulating demand at a moment when service-sector prices are still rising.

The implications for households are even more direct. Urban middle-class families feel the weight of services inflation more acutely than food inflation. Falling onion or cereal prices offer relief, but rising school fees, medical bills, rent, transport charges and childcare costs can swallow those gains quickly. Service-heavy inflation erodes purchasing power in quieter ways, and this erosion does not always show up in headline CPI.

MSMEs face similar stress. Small service firms—restaurants, retail outlets, coaches, salons, clinics, delivery fleets and business-support services—gain little from falling goods prices. Their biggest costs are wages, rentals, compliance expenses and electricity. As these costs rise, margins tighten, even when headline inflation suggests a mild environment.

The challenge is made harder by India’s data gaps. The country still lacks a full Services Producer Price Index, leaving policy institutions without a clear view of how service costs are evolving. Several recommendations to create such an index remain unimplemented. Meanwhile, India’s inflation-measurement overhaul may soon incorporate real-time e-commerce price feeds. This will improve coverage but could blur historical comparability and introduce new complexities for data interpretation.

Managing services inflation in India

India needs to realign its inflation management strategy with the economy it now has—not the one it had a decade ago. A clearer and more detailed indicator of services inflation must be published regularly, enabling the Reserve Bank of India to calibrate policy more accurately. MoSPI needs to accelerate work on a Services Producer Price Index that captures changes in health, education, logistics, communication and professional services. Better measurement will lead to better judgment.

Policy responses also need rebalancing. Rationalising compliance costs, municipal fees, digital reporting burdens and other para-tariffs would ease cost pressure on service-sector MSMEs. Incentives that support digitisation, energy efficiency and easier credit for service firms can reduce operational costs without adding to fiscal strain. Urban rental markets may need local-level regulatory attention to avoid cost escalations that feed directly into consumer inflation.

India’s inflation profile is undergoing a quiet, significant transformation. Goods and food are pulling headline inflation down, but services inflation is becoming the dominant force shaping everyday life. This divergence is not a temporary quirk; it signals a structural shift in consumption, wages, costs and compliance.

If India continues to rely on a CPI basket designed for a goods-dominated economy, it will misread both inflation risks and growth prospects. The next phase of inflation management must look beyond falling food prices and engage with the rising cost of services. Without this shift, India risks entering a period of silent, persistent services inflation—low in official statistics but high in the lived experience of households and businesses.