The rupee’s slide past 91 to the dollar is not a market aberration. It reflects a policy equilibrium in which the Reserve Bank of India has chosen to smooth volatility rather than defend levels, even as foreign portfolio outflows, importer demand for dollars, and geopolitical risk converge. The question for markets is not whether the rupee weakens further, but how that weakness is managed across time horizons.

In the near term, pressure is structural rather than speculative. Foreign investors have sold more than $3 billion of Indian equities in January alone, making the currency unusually sensitive to incremental dollar demand. Importers are covering exposures without corresponding exporter sales, while exporters are holding back receipts in expectation of further depreciation. The result is a one-sided market that intermittent state-run bank selling can temper but not reverse.

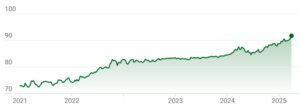

Indian rupee vs UD dollar

What is striking is that this has occurred without a broad-based dollar rally. The dollar index has remained range-bound, yet the rupee has been the weakest performer among major Asian currencies on several trading days. That divergence points inward. India’s widening current account deficit, equity-linked capital outflows, and uncertainty over trade relations with the United States are doing more damage than global financial conditions.

READ I Budget 2026: Fiscal policy debate ignores deepest structural flaws

RBI’s calibrated response

The RBI’s response has been deliberately calibrated. Intervention has been visible but modest, largely through forwards and buy–sell swaps rather than outright spot defence. The recent $10-billion swap that lifted headline reserves validates this approach. Reserves are being preserved, liquidity is being managed, but no attempt is being made to draw a hard line in the sand.

This restraint is not driven by incapacity. With reserves above $700 billion—covering more than eleven months of imports and the bulk of external debt—the central bank has ample firepower. The choice is strategic. A weaker rupee cushions growth at a time when external demand is uncertain and domestic investment sentiment remains sensitive to global risk cycles. It also aligns with a real effective exchange rate that has moved below 100, easing competitiveness pressures without triggering inflationary stress.

Over the medium term, the rupee’s path will be shaped less by flows and more by policy signals. The Union Budget will matter not for its headline numbers but for its credibility on fiscal consolidation and growth support. A budget that reassures bond markets and limits borrowing surprises will reduce pressure on the currency by anchoring rate expectations and curbing imported inflation risks.

READ I Budget 2026: Macro factors limits policy space for FM

Geopolitics and the rupee value

Equally important is the trajectory of India–US trade relations. Markets have discounted repeated timelines for a deal. Trump’s tariff threats, whether rhetorical or real, have raised the risk premium on Indian assets. Until clarity emerges, foreign investors are unlikely to rebuild positions at scale. This keeps the rupee vulnerable to episodic risk-off moves, even if intervention caps disorderly depreciation.

The central bank’s forward book adds another layer of complexity. Net short dollar positions exceeding $60 billion imply that future maturities will periodically test spot markets. These rollovers can be managed, but they constrain how aggressively the central bank can lean against depreciation without tightening domestic liquidity. That trade-off explains the preference for swaps and OMOs over large spot sales.

READ I Budget 2026: The fiscal arithmetic is getting harder

In the long run, the rupee’s outlook is less about exchange-rate management and more about macro fundamentals. Sustained currency stability requires a narrower current account deficit, deeper non-debt capital inflows, and a manufacturing and services export base that is less sensitive to global financial cycles. Trade agreements with Europe may help at the margin, but they are not substitutes for domestic productivity gains.

There is also an implicit acceptance within policy circles that gradual depreciation is not inherently harmful. What is being avoided is not weakness, but volatility. As long as inflation remains contained and external liabilities are manageable, a softer rupee is seen as an adjustment mechanism rather than a failure of policy.

In the short term, the rupee remains biased weaker with intermittent intervention to prevent overshooting. In the medium term, fiscal signals and trade clarity will determine whether depreciation stabilises or continues. Over the long term, the currency will track India’s ability to convert growth into durable external competitiveness. The central bank’s actions indicate that it is prepared to live with the answer.