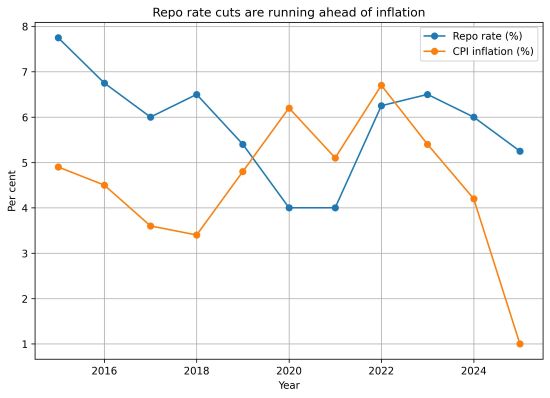

India’s monetary policy has entered a phase where comfort risks breeding complacency. Inflation has collapsed to levels rarely seen in a large developing economy. Core inflation is muted and growth remains well above potential. Since February 2025, the Monetary Policy Committee has cut the repo rate by 125 basis points to 5.25 per cent. Governor Sanjay Malhotra has argued that real interest rates must fall further to support demand as growth momentum softens. The argument is coherent. It is also incomplete.

In an economy with strong credit growth, stretched market valuations and uneven real investment, aggressive easing carries risks that do not appear in inflation prints. Monetary policy must confront those risks before they harden.

READ I Will RBI’s repo rate cuts bring relief to homebuyers?

Disinflation expands space—but it also blurs signals

India’s inflation numbers are striking. CPI inflation fell to 0.25 per cent in October and rose marginally to 0.71 per cent in November. Core inflation excluding precious metals is lower still. These readings place inflation far below the 4 per cent target and outside the lower tolerance band. Under the inflation-targeting framework, the MPC is entitled—indeed obliged—to respond.

Yet very low inflation also weakens price discipline. When nominal rates fall sharply, risk is mispriced before demand revives. Asset prices react faster than investment decisions. The IMF has warned repeatedly that prolonged periods of low inflation combined with accommodative policy tend to inflate financial assets first. India’s growth story does not repeal that arithmetic.

READ I RBI must let the rupee settle closer to its real value

Credit is easing faster than activity is slowing

Bank credit continues to grow at double-digit rates, led by retail loans, unsecured credit, and housing. RBI data show that credit to manufacturing lags well behind personal lending. Transmission is largely complete. Lending rates are falling. Liquidity conditions are easy.

By contrast, the slowdown that worries the MPC remains prospective rather than realised. GDP grew 8.2 per cent in the second quarter. The RBI expects full-year growth to exceed 7 per cent, moderating to around 6.7–6.8 per cent only in the coming quarters. This is not a demand shock. It is a return towards trend. Cutting rates aggressively in this setting risks amplifying leverage where it is already rising, rather than catalysing new investment where it is absent.

READ I IMF flags rupee flexibility shift as RBI reduces intervention

Asset markets are flashing warnings

Equity markets have delivered outsized returns, particularly in mid- and small-cap segments where valuations have detached from earnings growth. Residential real estate prices in major cities have risen sharply, supported by cheaper credit and improved sentiment. These moves have occurred alongside uneven wage growth and fragile external demand.

The RBI has flagged these risks before, notably in its Financial Stability Reports, which point to rising household leverage and stress in unsecured lending. The lesson from other economies is unambiguous. Extended monetary accommodation after the global financial crisis inflated asset prices well beyond fundamentals. When adjustment came, it was abrupt and costly. India’s cycle is smaller, but the mechanics are identical.

Low inflation does not suspend financial stability

Several MPC members have described inflation as “too low” for a developing economy and indicative of a demand deficit. The diagnosis is defensible. The inference is not automatic. Monetary policy cannot treat financial stability as a downstream concern to be addressed later through regulation alone.

The RBI’s mandate is not confined to inflation and growth in isolation. It includes systemic stability. When rate cuts become the dominant response to a mild cyclical deceleration, macroprudential tools must do more of the work. Higher risk weights, tighter loan-to-value norms, and closer scrutiny of unsecured lending are not optional add-ons. They are the price of aggressive easing.

External risks argue for restraint, not reassurance

External conditions remain unsettled. Merchandise exports have contracted. Manufacturing indicators have softened. Trade disruptions linked to US tariff actions and geopolitical uncertainty weigh disproportionately on MSMEs and labour-intensive sectors. These risks justify support.

They do not justify indifference to capital flows or currency pressures. Rate cuts narrow interest differentials at a time when global monetary conditions remain volatile. Liquidity-driven asset booms unwind faster when external sentiment shifts. Strong reserves reduce vulnerability. They do not eliminate it.

What calibrated easing should look like

The MPC’s decision to retain a neutral stance despite cumulative easing is therefore prudent. It preserves room to respond. That room must be used judiciously. Further cuts should be explicitly contingent on evidence that lower rates are translating into productive investment rather than speculative leverage.

Communication matters. When the central bank emphasises only low inflation and growth support, markets price a one-way liquidity trade. When it speaks clearly about financial stability, expectations adjust. Central banks that learned this lesson late paid for it with sharper tightening later.

India’s macroeconomic position is strong. That strength demands discipline, not haste. Rate cuts may be necessary, but they are not costless. When monetary easing fuels asset inflation faster than real investment, policy has already lost its way. The RBI should continue to cut rates if conditions warrant—but with vigilance that is visible, firm, and unsentimental. Growth sustained by bubbles is not stability. It is deferred risk.